AE Wealth Management: Weekly Market Insights | 1/1/23 – 1/7/23

Weekly Market Commentary

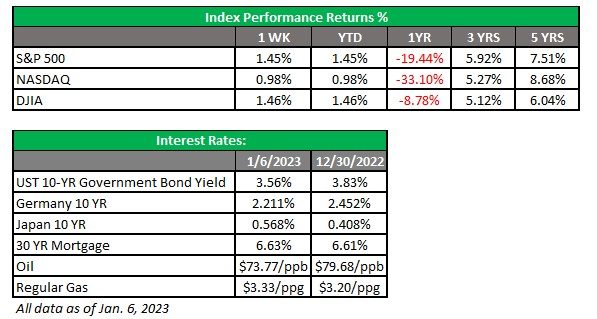

THE WEEK IN REVIEW: Jan. 1 – 7

Could Fed’s work be working?

We rounded the corner into a new year, and stocks ended the first full week of 2023 on a high note, with each of the three major markets up more than 2% on Friday. The markets were buoyed by signs that inflation may indeed be slowing, including lower-than-expected wage growth. Friday was the best day for the Dow and the S&P since Nov. 30. The services sector also showed contraction in December, after months of steady growth, another sign that the economy may be slowing.

Jobs reports give mixed signals

On Wednesday, the U.S. Bureau of Labor Statistics shared its latest job openings figures — showing openings were essentially unchanged at 10.5 million in November. This translates to 1.7 job openings for every unemployed worker, a ratio that the Fed would like to see continue to decline. Pre-pandemic, the U.S. was at 1.2 job openings for every unemployed worker.

Meanwhile, the unemployment rate fell further than expected, to 3.5%, and nonfarm payrolls were higher than estimated, at 223,000 jobs added for the month. While these numbers arrived better than expected, wage growth missed expectations in a sign that inflation pressures could be weakening — a positive sign for markets. Average hourly earnings were up 0.3% for December and 4.6% for the year while expectations had been for 0.4% and 5% increases.

Another positive sign for markets: Service industry activity slowed for the first time in more than 2 ½ years as demand weakened in December. The Institute for Supply Management (ISM) non-manufacturing PMI benchmark has remained surprisingly solid month after month, beating expectations in November with a score of 56.5. Economists’ expectations had been for another month of expansion in December, at 55.0. But Friday’s numbers showed lower activity — at 49.6 for December. It was the first time since May 2020 that this indicator has fallen below 50. The services sector accounts for more than two-thirds of U.S. economic activity, so this level is a noteworthy sign. Indeed, the ISM says a level that sustains under 50 can be consistent with a recession.

So, what’s the Fed to do?

After raising the federal funds rate seven times in 2022 for a total of 4.25 percentage points, it appears more increases could be on the way. Expectations are for another 0.25 percentage point increase at the Fed’s next meeting, Feb. 1. Federal Open Market Committee members indicated in their last meeting in December that they’ve seen progress in tamping down inflation but that they need more evidence inflation is on a sustained downward path. We’ll keep watching and listening.

Leadership tussle settled — after dozens of rounds

Although we say that divided government can be good for markets — when one party controls the White House and the other the Congress — because it is less likely that big spending initiatives or big changes will pass, we didn’t expect so much intra-party division. But this past week we saw infighting that led to four days of negotiations to seat a new speaker of the House. It wasn’t until a 15th round of voting late in the night Friday that Speaker Kevin McCarthy was installed. The last time it took this many votes to seat a speaker was before the Civil War.

It remains to be seen how the House will function with some deep divisions remaining among its factions and what concessions McCarthy has had to make to hold onto power. What we do know is that this is likely a further sign that we won’t see significant new government spending initiatives emerging this year, which is another good sign for continued inflation cooldown.

Coming this week

- Several Federal Reserve policymakers have speaking engagements this week, including the Atlanta Fed president on Monday and the Philadelphia and St. Louis Fed presidents on Thursday. Federal Reserve Chairman Jerome Powell will speak in Sweden on Tuesday at a symposium hosted by Sweden’s central bank. We’ll see if any notable insights are shared about the Fed’s plans going forward.

- The Consumer Price Index (CPI) for December will be released Thursday. Expectations for core CPI are that it will drop to 5.7% from its previous 6%.

- On Thursday, we’ll also get a look at initial jobless claims for the first week in January, and those are expected to rise slightly, to 210,000 from the prior 204,000.

- This week we’ll also get an early look at the University of Michigan consumer sentiment survey, a leading indicator of consumer attitudes, when its preliminary report is released Friday. How consumers are feeling can tell us a lot about where the economy is headed this year.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

01/23-2659492-2