AE Wealth Management: Weekly Market Insights | 1/28/24 – 2/3/24

Weekly Market Commentary

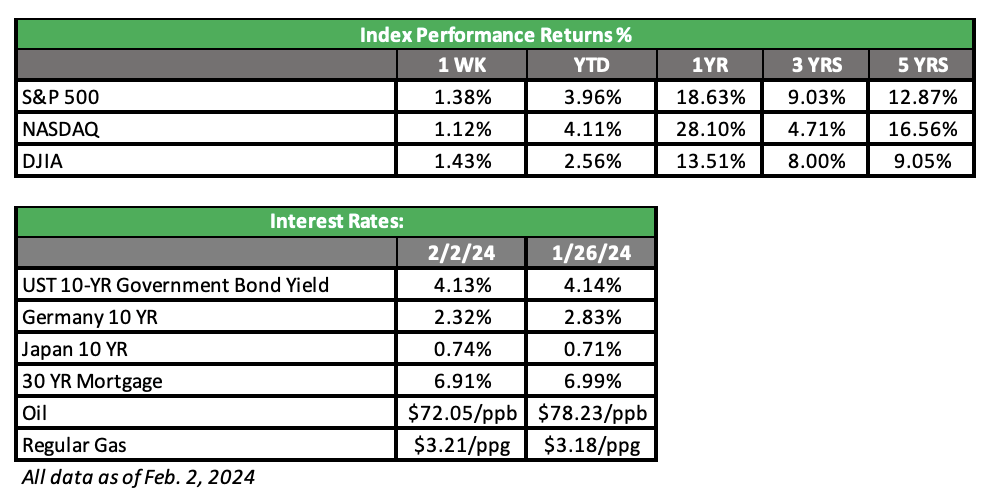

THE WEEK IN REVIEW: January 28 – February 3, 2024

Powell pushes back — and markets get a dose of reality

Remember the “Soup Nazi” from Seinfeld? Well, Federal Reserve Chairman Jerome Powell channeled his inner “Soup Nazi” with an emphatic “No rate cuts for you” last Wednesday. He essentially poured cold water (or soup) all over the market’s expectations that rate cuts would start as early as the March meeting. In response, markets had a tantrum and handed us the worst day since last September.

Markets have once more convinced themselves to expect a very narrow result and were shocked when reality intervened. Fortunately, the shock didn’t last long; markets quickly made the best of it, rallying on Thursday and Friday in the hopes that even though Powell said “no” in January, he may say something very different in March.

Then we got the latest earnings report from Meta (Facebook), which showed that despite higher interest rates the big tech companies were still very profitable. The jobs number also blew away expectations (more in the next section). The trend of “bad news is good” didn’t play out, since stronger jobs and a resilient economy run counter to the case for lowering rates.

Still, the data didn’t seem to dampen enthusiasm as we ended the week. Markets instead focused on solid earnings and visions of future rate cuts dancing in their heads. After all, if Meta can crank out earnings in the current rate environment, just wait and see what happens to Big Tech when rates start dropping.

The market quickly made the shift from waiting for the Fed to pause to now expecting cuts. How many and how soon remains to be seen, but it’s clear we will have rate cuts — and those will likely create some near-term volatility. The mood could also sour if the economic, job growth and inflation data remain stubbornly high, which could lead the Fed to keep rates where they are for longer. And the closer we get to the election, the less enthusiastic the Fed will be to cut at all. But markets seem stubbornly locked into their expectations for a rate cut sooner rather than later.

Jobs refuse to stop growing

The market was looking for weakness on the jobs front but definitely didn’t get it last week. Consensus was calling for 170,000 new non-farm payrolls, and we got more than twice that at 353,000. Wages also grew above expectations (+4.5% vs. 4.1% year-over-year), while the unemployment and labor participation rates remained unchanged.

The continued strong jobs and fourth-quarter gross domestic product (GDP) readings, along with a stalled inflation rate at just over 3%, are consistent with the Fed’s stated desire to hold back on lowering rates lest we see a resurgence of inflation. Markets were initially buoyed by the ADP report showing 107,000 new jobs, far below the consensus estimate of 145,000 and significantly lower than last month’s 158,000 reading. But then the Bureau of Labor Statistics (BLS) comes in nearly three times higher. Who is right: ADP or BLS?

Based on the data, maybe we don’t need to see six rate cuts this year. The markets can turn anything to suit the prevailing mood, and right now expectations are based on an optimistic upward bias. Like a grounded teenager trying to explain why they need to use the car on Saturday night, the market seems to be torturing truth and logic in pursuit of the end goal. Markets were expecting six cuts, were flatly told there would be three possibly, and the data currently leans toward fewer cuts. Plus jobs, GDP and inflation are all signaling maintaining rates at current levels. Still, it’s Saturday night for the markets — “everybody” is going to this party and they don’t want to miss out.

Coming this week

- With the Fed meeting behind us and jobs numbers still pointing to a stronger and more resilient economy, the coming week will be about assessing what that means and if the narrative about how many rate cuts to expect this year has changed.

- There will be a veritable cornucopia of Fed speakers this week, with several Fed presidents stepping up to the mic. Anything and everything they say could impact markets.

- We’ll see earnings again all week. We’ll also get the latest U.S. trade deficit, consumer credit and MBA mortgage applications (Wednesday) plus unemployment claims and wholesale inventories (Thursday).

- So far, 25% of S&PR 500 companies have reported fourth-quarter 2023 earnings, with 69% reporting positive earnings per share and 68% showing positive revenues. However, the blended year-over-year earnings decline for the S&P 500 is -1.4%. If it holds, it will mark the fourth time in the last five quarters that the S&P 500 has reported a year-over-year earnings decline.

Sources:

https://www.morningstar.com

https://www.cnbc.com

https://www.marketwatch.com

https://www.cnbc.com

https://markets.businessinsider.com

https://ycharts.com

Accessed 02/02/2024

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

2/24-3358715-1