AE Wealth Management: Weekly Market Insights | 3/31/24 – 4/6/24

Weekly Market Commentary

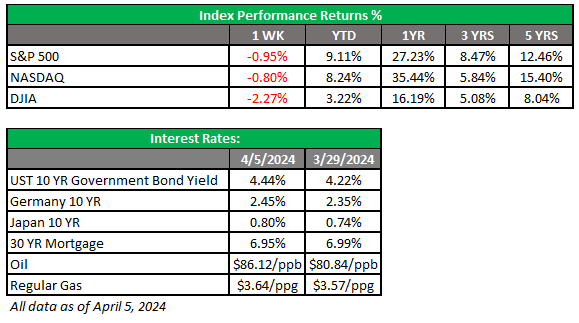

THE WEEK IN REVIEW: March 31 – April 6, 2024

Markets pull back slightly from record highs

After hitting record highs in late March, markets pulled back a bit last week. Stocks moved lower after the March Institute for Supply Management’s (ISM) manufacturing reading came in higher than expected and indicated slight expansion for the first time in over a year. The ISM prices paid index also surprised on the upside, showing a rebound in input prices.

This “good news” rattled markets, which have been looking for signs the economy is shrinking so the Federal Reserve can start interest rate cuts in June. But the ISM services report on Wednesday provided a bit of solace; the report showed services fell back for the second month in a row and prices paid for those services fell to their lowest level since the beginning of the pandemic in March 2020.

And then there’s the data on jobs. The ADP employment report released on Wednesday showed we added 184,000 private sector jobs in March. Industries adding the biggest numbers? Construction, financial services and manufacturing. Meanwhile, the Bureau of Labor Statistics (BLS) reported 303,000 new non-farm payroll jobs were added in March, mostly in the health care, government and construction industries. The unemployment rate stayed steady at 3.8%.

All of this data says the economy is still healthy, which seems like good news on the surface. However, it’s continued cause for concern that the Fed will put off rate cuts. In response, the yield on the 10-year U.S. Treasury jumped to its highest intraday level since November.

Remember a year — and even six months — ago, when all the talk was about a coming recession? The hubbub seems to have evaporated, and experts’ expectations for a recession are dwindling. The U.S. economy seems to have reached a balance where steady commercial activity, growing employment and rising wages can coexist despite higher interest rates.

Coming this week

- What’s the latest on inflation? We’ll find out this week, as the consumer price index (CPI) will be released on Wednesday. The current forecast is calling for a year-over-year increase of core CPI (all expenditures minus food and gas) of 3.7%. Then we’ll follow up with the producer price index (PPI) on Thursday.

- Other than CPI and PPI, there won’t be a lot of data to drive markets this week. We’ll see wholesale inventories (Wednesday), initial weekly unemployment claims (Thursday), and the import price index and consumer sentiment (Friday).

- Fed officials are making the rounds again this week, plus the minutes from their March meeting will be released on Wednesday.

Sources:

https://www.morningstar.com

https://www.cnbc.com

https://www.marketwatch.com

https://markets.businessinsider.com

https://ycharts.com

Accessed 04/05/2024

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

4/24-3481697