AE Wealth Management: Weekly Market Insights | 6/5/22 – 6/11/22

View PDF Version

THE WEEK IN REVIEW: June 5 – June 11

Inflation gets worse

The Consumer Price Index (CPI) climbed back to 8.6% after dipping to 8.3% in May, setting a new 40-year high. (The previous recent high was 8.5% in March.) So much for peaking inflation; it seems we’re heading in the wrong direction. Prior to the data coming out, markets were working on the hope that inflation was on a downward trend and the Federal Reserve would potentially have an excuse to stop raising rates in September. All this hope seems misguided, as the Fed has merely said it would “reevaluate” its approach when so far it has only raised rates by 0.75% and currently plans to raise another 1%.

The market was supposed to have all this priced in, right? Now the market is predicting another hike of 50 basis points (.50%) at its September meeting. (There is no meeting in August.) So much for a September “pause.” The mathematical solution as to how much more the Fed needs to raise is as follows: If inflation remains around 8.5%, and we’ve already been committed to raising the fed funds rate by 1.75% plus targeting 2% inflation, to truly fight inflation the Fed needs to raise rates by 4.75%. It currently looks like the market hasn’t factored in anything close to that.

The Consensus was calling for CPI to come in at 8.2%, with the top estimates at 8.4%. It seems as if lots of people were still mentally stuck in the “transitory” trap, not believing what they were seeing and willing inflation to drop on its own. Hope is a poor excuse for a well-executed plan.

In January 2021, inflation was at 1.4%; now, we’re at 8.6% 16 months later. After the 2020 election, we expected it would take some time for the new administration to implement its policies and undo or rethink the prior administration’s policies. The Biden administration’s use of excessive stimulus measures will likely prove to have been wrong from the start, plus, the Fed has been behind the curve on inflation the entire time, unwilling to commit to a direction. They dangled a September “pause” after two hikes this summer, and now it looks like we’ll have another 50-basis-points hike a few months from now.

The problem is twofold: a weak Fed plus a clear lack of a plan of action from the administration. The Biden administration and headlines say the economy is growing, but gross domestic product (GDP) was -1.5% in the first quarter. The Atlanta Fed is estimating that second-quarter GDP will increase 0.9%, and if that holds, we’re looking at the first half of 2022 contracting by 0.6%. We are being told there are tons of jobs, and the inflation is only in food and gas prices (spoiler alert – it’s not). There appears to be a disconnect between what people are seeing in their day-to-day lives and what is being put out officially.

The Fed will have to get more aggressive, because the longer this goes on, the worse things will get. But without effective policy measures from Washington — such as a 180-degree change in energy policy — the current situation will just continue.

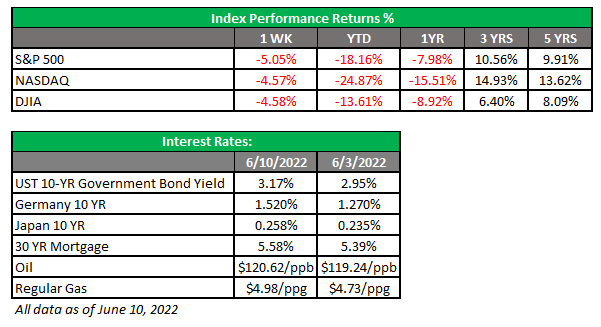

To make matters worse, both the two- and five-year treasury curves inverted with the 10-year U.S. Treasury note last week. This means nearer-term maturities have a higher yield than longer ones and signals less confidence in the economy going forward, a further sign of trouble for the U.S. economy.

Housing stumbles

The housing market is still red-hot, but it appears there may be trouble lurking here, too. For example, the 30-year fixed mortgage rate has doubled to 5.6% from 2.75% last fall. Applications for a mortgage to purchase a home fell 7% last week, 21% lower than the same week in 2021. With mortgage rates marching higher, it was no surprise that refinance demand also dropped 6% and was down 75% year-over-year.

The market is still hot because there is little inventory and lots of demand. However, people are being priced out, due to both higher asking prices and rising interest rates. Focusing on the housing numbers is important due to ripple effects on both the retail and services sectors. Think about all the Home Depot visits, appliances and electronics and furniture sold, remodeling projects, etc., that go along with home ownership. A slowdown in housing is on the way, and with the current state of the economy, it will not be welcomed at all.

Coming This Week

- The Fed will meet this Tuesday and Wednesday. Expectations are for them to raise rates another 50 basis points (.50%) and for the fed funds rate to rise to 1.25%. If there is no surprise announcement of an even higher rate or change in upcoming rates, markets should be calm.

- Markets will wait for Fed Chair Jerome Powell’s news conference after the meeting, which can be a significant market mover. When Chairman Powell spoke in early May, he told us he could not guarantee a soft landing. Following his remarks, the Dow rallied nearly 1,000 points in the last 1.5 hours of trading, only to lose it all and then some the following day. The comments turned out to be the catalyst to take us to a new 2022 low later in the month.

- The Producer Price Index (PPI) for May will be released on Tuesday. Costs for producers are expected to rise.

- Mortgage applications, retail sales and business inventories will likely confirm the economy is softer and slowing. On Friday, leading indicators will close out the week. Perhaps they will provide a bright spot.

- Make no mistake: This week will be all about the Fed and how Chairman Powell walks the tightrope on inflation and raising rates.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

6/22 – 2230390-2