AE Wealth Management: Weekly Blog Insights | 1/22-1/29/22

The markets take a wild ride!

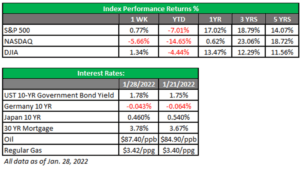

The market continued its volatile ride last week, with massive swings before and after the Federal Reserve’s announcement. (More on that below.) We had major gyrations as various factors weighed on a market that’s desperately seeking consensus. After wiping out a 1,000-point drop on Monday, the wildness continued with another 1,000-point swing on Tuesday and a 900-point swing on Wednesday. On Thursday, we got a surprise fourth-quarter gross domestic product (GDP) number of +6.9%. Markets initially rose on the news but Who would have thought we’d end in the red on a day when we saw +6.9% GDP growth?

The high GDP increase was somewhat of a surprise. October must have been incredible in the gap between the Delta variant surge subsiding and Omicron taking hold, while November and December were pretty slow. Even with the growth, there is a lot to be pessimistic about concerning the economy. Tensions in Ukraine, oil creeping closer to $90 per barrel, the 10-year U.S. Treasury closing in on 1.9% last week, the Fed talking interest rate increases and tapering, and the consumer wilting in the face of higher prices all make it difficult to get excited about markets.

Finally, Apple reported record earnings after the close on Thursday, which pushed markets upward to end the week. After finishing 2021 on a high note, markets have drifted downward toward correction territory. (In fact, the Nasdaq is already there.) There has been ample opportunity for investors to position themselves for the turbulence we are experiencing, and there still may be time as we experience false rallies amid mostly gloomy news.

We caution against timing the market since you have to make two calls correctly (when to get out and when to get back in) when it’s hard enough to make one. For most of us, this will be a speed bump on the journey, and like 2018 and 2020, we will likely come back stronger. In 2018, we dropped to 2,400 on the S&P 500, and in 2020 we dipped to 2,200. Last week, the S&P 500 closed at 4,300.

Let’s put things in perspective: As grim as things may seem, think about how much worse we could be right now if we acted on our fears. Benjamin Graham once said, “In the short run, the stock market is a voting machine. Yet in the long run, it is a weighing machine.” Right now, the vote appears to be bearish, but it will likely not last. Volatility is here for 2022, and returns will be challenged in the first half of the year. However, once we get clarity from the Fed and markets level off, we’ll likely have a strong second half, and many of these worries will likely subside.

Fed lays out its tightening plan

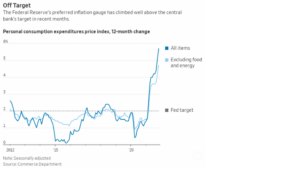

There was consensus going into last week that we would see the end of quantitative easing and that we could expect four rate hikes in 2022, starting in March. The Fed meeting left us with the details that bond purchases were lowered to $30 billion per month and a likely rate hike would take place in March, although the Fed made no real commitment on that front. Fed Chair Jerome Powell also confided that inflation should have been worse and that the supply chain won’t get fixed for a year. All of this combined killed a pretty decent rally last Wednesday.

Here’s our question: If inflation is worse than what you thought, shouldn’t you stop putting more money into the economy? Why not end the bond purchases altogether and send a strong signal in March that you will definitely raise rates in a “meaningful manner” — and that you will do so at each Fed meeting until we see inflation return to more normal levels? Let the market figure out what you mean by meaningful, whether that’s 25 or 50 bps per meeting or four or five increases per year. If things are moving in the right direction, then Powell can pull back on the tightening and the markets will rally on the surprise news. This “we are prepared to raise rates in March depending on the data” appears to be a weak dovish stand meant not to upset the markets. Unfortunately, it did because the markets are smart enough to know that the Fed will need to act or it may lose control of the inflation fight (if it hasn’t already done so). Give us all of the bad news at once so we can process it and move on from this death by a thousand cuts. Parlor games and furtive glances — that’s a tough way to invest.

On the supply chain statements Powell made, it’s difficult to project when that mess gets cleaned up. Many things impact the supply chain: worker availability, regulations, government interference and consumer behavior among them. However, these are all things the Fed cannot control. The Fed needs to realize that the high levels of inflation we are experiencing exist because of excessive liquidity they’ve created through accommodation, along with the federal government’s deficit spending. Inflation was not caused by “Big Meat,” “Big Gas,” “Big Auto,” “Big Grocery” or “Big Toilet Paper.” It was caused by putting all this money into the hands of people, and more was demanded than our ability to produce it, so logically pulling money out of the system will result in less being consumed and supply will not be strained.

Coming This Week

- After a pretty tumultuous week, we should be fairly quiet data-wise as we close out the first month of 2022. This week’s major economic data points will be around the jobs picture, with ADP on Wednesday and January jobs numbers from the Bureau of Labor Statistics (BLS) on Friday. Despite the stronger-than-expected Q4 GDP last week, the economy is slowing and slumping jobs numbers could further solidify weakness going forward. Remember, the December number was +199,000, the lowest for 2021.

- On Tuesday, we’ll get a look at the Labor Department’s Job Openings and Labor Turnover Summary (JOLTS) report, which tracks the monthly change in job openings and offers rates on hiring and quits. We saw a net 10.562 million openings last month. The continued narrative around this is with unemployment at rock bottom, we still have 10+ million job openings. In theory, this places pressure on wages since there are way more openings than workers available to fill them.

- Several Fed officials will give speeches this week, and after Chairman Powell’s latest Fed meeting press conference, we can expect almost anything.

- Finally, mortgages and car sales numbers will be released this week. They are expected to remain strong, based on scarcity more than anything else.

Have a great week!

Tom Siomades, CFA®

Chief Investment Officer

AE Wealth Management

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The personal opinions expressed by Tom are his alone and may not be those of AE Wealth Management or the firm providing this report to you. The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

1/22 – 1973321