AE Wealth Management: Weekly Blog Insights | 1/9-1/15/22

Inflating Inflation

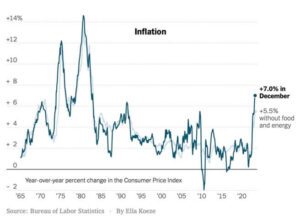

Inflation numbers keep setting the wrong kinds of records. Last week’s inflation data showed consumer prices rose 7.0% over the past year, the largest 12-month gain since June 1982. Core inflation — which doesn’t include food and energy — rose 5.5%, the most since 1991, while core producer prices were up 9.7% year over year, hitting the highest level in records going back a decade. Add in a 1.9% drop in December retail sales, and it made for a rocky week in the markets.

Last week, Federal Reserve Chairman Jerome Powell told lawmakers that the Fed would take strong action to curb inflation, and some analysts have said they now expect four interest rate hikes in 2022, not three. Employment numbers are only adding to the inflationary pressure; the unemployment rate fell to 3.9% in December. Low unemployment now could signal we’re headed toward a wage-price spiral later, where higher prices cause workers to demand higher wages, which leads to higher prices, which leads to … well, you see where this is going.

Talk about interest rate hikes wasn’t the only thing causing market jitters last week. Minutes from the Fed’s December meeting revealed comments about winding down their $9 trillion balance sheet. We also kicked off the unofficial start to earnings season, with JPMorgan Chase and Citigroup reporting lower profits in the fourth quarter. Hopefully, this isn’t a foreshadowing of other earnings reports to come.

Remember two years ago, when “flatten the curve” was all the rage? Seems we’ve flattened the curve of a different kind. Short-term rates continued their ascent ahead of tighter monetary policy, leading to a flatter yield curve last week.

One bright spot among all the doom and gloom was retail inventories, which rose 1.3% in November. It doesn’t sound like a lot, but it was the highest increase since February 2021. Is it a sign that supply challenges are beginning to ease up? Retailers and manufacturers alike would love to be able to answer that question with a resounding “Yes.”

Fun facts about the S&P 500

The S&P 500 outperformed both the Dow Jones Industrial Average (by 8.16 percentage points) and the Nasdaq (by 5.5 percentage points) in 2021. This marks the widest outperformance by the S&P 500 against both peers in the same calendar year since 1997. It’s also only the sixth time the S&P 500 has outperformed both the Dow and the Nasdaq in the same year.

Coming This Week

- Data is compressed in this four-day workweek, as most agencies were closed in observance of Martin Luther King Jr. Day.

- Housing data will be plentiful this week. We’ll get the building permits and housing starts numbers on Wednesday, followed by existing home sales on Thursday. As mortgage rates continue to tick up, could the housing market cool over the next few months?

Have a great week!

Tom Siomades, CFA®

Chief Investment Officer

AE Wealth Management

| Equities: | 1 WK | YTD | 1YR | 3YRS | 5YRS |

| S&P 500 | -0.30% | -2.17% | 22.85% | 21.77% | 15.44% |

| NASDAQ | -0.28% | -4.80% | 13.58% | 29.20% | 21.72% |

| DJIA | -0.88% | -1.17% | 15.88% | 14.52% | 12.55% |

| Interest Rates: | 1/14/2022 | 1/7/2022 | |||

| UST 10 YR Government Bond Yield | 1.78% | 1.76% | |||

| Germany 10 YR | -0.034% | -0.040% | |||

| Japan 10 YR | 0.152% | 0.135% | |||

| 30 YR Mortgage | 3.51% | 3.43% | |||

| Oil | $83.55/ppb | $78.96/ppb | |||

| Regular Gas | $3.39/ppg | $3.38/ppg | |||

| All data as of January 14, 2022 |

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The personal opinions expressed by Tom are his alone and may not be those of AE Wealth Management or the firm providing this report to you. The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

01/22 – 1973321-3