AE Wealth Management: Weekly Market Insights | 1/22/23 – 1/28/23

Weekly Market Commentary

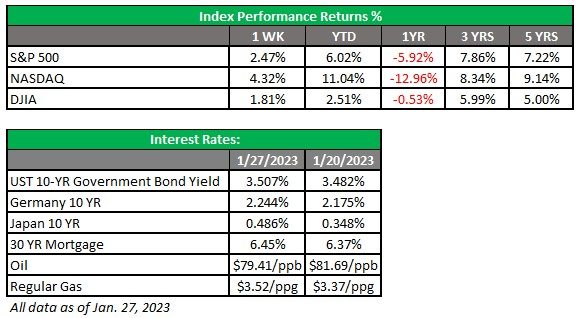

THE WEEK IN REVIEW: Jan. 22 – 28

Fourth quarter 2022 stronger than expected; U.S. notches 2.1% growth for the year

The initial reading of fourth-quarter gross domestic product (GDP) came in at 2.9%. While the reading was higher than the consensus estimate, it was much lower than the Atlanta Fed’s forecast of 3.5%.

Overall, the U.S. economy grew at an annual rate of 2.1% in 2022. It’s a pretty modest number, but if you consider that growth was negative in the first six months, the fact that we managed to get above 2% for the year is pretty remarkable. Expectations for the economy to slow thanks to inflation and a more aggressive Federal Reserve failed to materialize in the back half of the year. (However, we are showing signs of a slowing economy now.)

The increase in real GDP in 2022 primarily reflected increases in consumer spending, exports, private inventory investment and non-residential fixed investment (such as offices, industrial, retail, etc.). These were all partly offset by decreases in residential fixed investment (housing) and federal government spending (stimulus spending mostly ended). Imports also increased thanks to consumers. Stock markets suffered as we wrestled with higher interest rates and the uncertainty of when the Fed will decide it has done enough to cool the economy and tame inflation.

Last year, pundits conveniently punted any talk of recession into the early part of 2023 and beyond. We’re now in the early part of 2023 — and there is talk of a recession in mid- to late-2023 from the same people who told us we would have a recession by now. Here’s the conundrum: We’ve been in “economic neutral” since the beginning of last year. Yes, there have been up quarters to counter the down quarters, but that choppiness doesn’t mean all is well with the economy. We still have elevated inflation and high energy prices. Consumers seem to be showing signs of weariness, plus savings are being depleted just as credit card balances are rising along with interest rates. Tech companies are laying people off, earnings are deteriorating and the housing market has stalled.

The challenge now is to negotiate the next three to six months without getting caught up in the negativity we are likely to start seeing in the economy as higher interest rates take hold. The markets seem to be turning and signaling what we may be in for by the summer heading into fall. Economic news will likely get worse, but the equity market is forward-looking. Given the resilience of the market, so far we are optimistic, even though Main Street looks like it will begin feeling the pain more acutely.

Earnings weaken but markets hang in there

The long-anticipated decline in earnings has begun. There have been some painful announcements (Chevron, Intel, etc.), one or two upside surprises (Tesla), and some outright ugliness (Bed Bath & Beyond). Overall expectations are that fourth-quarter earnings will be down around 2.2%.

If that’s the worst of it, is it any surprise markets have hung in there so far? The S&P 500 continues to hover around 4,000 and the Dow is maintaining between the 33,500 and 34,000 level. If the Fed slows and/or pauses rate hikes, we may have seen the worst of the market declines. If that’s the case, it feels like we’re in a really good place to begin our march back to records set in early 2022. Companies will likely shed excess costs and workers as we head into the depths of the recession everyone seems to believe we’re headed toward.

But just as things appear to be at their darkest, some companies will report much better earnings off depressed levels — and we’ll be back on our way up. When will this happen? It will start when the Fed pauses, GDP dips and unemployment rises. Until then, we need to stay focused and disciplined and wait for the opportunity to present itself.

Coming this week

- The Fed is scheduled to meet on Tuesday and Wednesday, the first meeting of 2023. Expectations are for a rate increase of 25 basis points (.25%). The odds of a 50-basis-point (.50%) increase are very remote; if it materializes, markets will likely have an adverse reaction.

- The earnings drumbeat will continue this week. So far, early earnings have been mostly muted. Any uptick will propel markets upward.

- We will see jobs data this week, with the ADP report and Job Openings and Labor Turnover Survey (JOLTS) released on Wednesday and the Bureau of Labor Statistics (BLS) employment situation coming out on Friday. The BLS December report showed we added 223,000 jobs in December, and expectations are we’ll see some signs of weakness. If the numbers persist in exceeding expectations, the Fed will continue to raise rates and keep them higher for longer.

- Car sales and factory orders will also provide some meaningful data in the coming week.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

01/23 – 2659492-5