AE Wealth Management: Weekly Market Insights | 1/15/23 – 1/21/23

Weekly Market Commentary

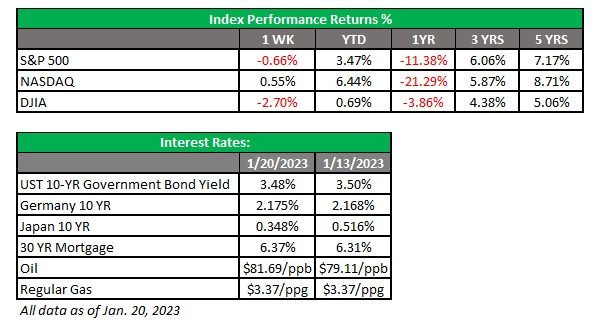

THE WEEK IN REVIEW: Jan. 15 – 21

Fed officials refuse to soften stance despite lower inflation and weak earnings

It’s always a good idea to watch those Federal Reserve officials and their remarks. Markets were set to rejoice last week, after the December Producer Price Index (PPI) came in at -0.5%, well below the consensus estimate of 0.1%. Year-over-year producer prices also declined, dropping from 8.0% in October to 7.4% in November, then 6.8% in December.

This is great news and clearly where we want to see inflation heading. As we’ve discussed here before, the PPI is a lead indicator for the direction of consumer inflation; if manufacturers’ prices for the materials they need to provide their products or services drop, logic dictates that the prices we all pay for those goods and services will also decline. That was the theory markets were applying when they took off early Wednesday after the latest PPI number was released.

Then St. Louis Federal Reserve President James Bullard said U.S. interest rates have to rise further to ensure inflationary pressures continue to recede. And Loretta Mester, president of the Federal Reserve Bank of Cleveland, welcomed actions to tame inflation, while the Kansas City Fed’s Esther George said the central bank must restore price stability and defined it as “returning to 2% inflation.” Overall, Fed speakers maintained their hawkish stance and hinted at more rate hikes ahead.

Just like that, the nascent market rally sputtered and began a downward spiral. Fed officials clearly don’t believe enough has been done to tame inflation and that they need to do more. If you take George’s comments literally, does that mean we need to see 2% inflation before they stop raising rates? We don’t know — but the lack of softness in their comments doesn’t give the market any hope. You would think three months of decreasing inflation would at least merit some discussion of a pause.

Fourth-quarter earnings reports also upset markets last week. Goldman Sachs had its worst earnings miss in a decade, while several other major banks also reported less-than-stellar earnings. (Banks are first to report earnings every cycle.) Clearly the rise in rates is impacting markets and earnings and will eventually filter down to the rest of the economy. The lack of any rays of hope or flexibility from Fed officials is worrying markets. Now earnings aren’t offering any comfort, and soon the economy will feel the weight of higher rates.

Holiday sales fizzle, sparking more concerns of an economic slowdown

There’s been much talk of a dreaded global economic slowdown. We get a decline in global oil demand and it’s a signal that the world is falling off a cliff. But here’s something interesting: Our fourth-quarter gross domestic product (GDP), scheduled to come out this week, is forecasted to be 2.8%! That doesn’t sound like a slowdown.

However, it could be all smoke and mirrors. After all, China reported last week that its GDP grew at a 3% rate last year, its lowest growth rate in decades. Remember how Goldman Sachs said only a month ago that China was going to overtake the U.S. as the world’s largest economy by 2035? Our economy sure doesn’t feel like it’s growing at 3.5%, and we’re not sure any economic data out of China can be fully relied on to be accurate, so which is it?

If December retail sales are any indicator, we may be well on our way to a slower economy. The U.S. consumer has been a rock star over the past three years, and if the U.S. consumer were to falter — as the December data is suggesting — we could have trouble. Perhaps inflation, negative wage growth and higher interest rates have pushed the consumer to exhaustion. Let’s hope the December retail sales figures were an anomaly, but with a choppy market, sour economic outlook and overall lack of enthusiasm on the public’s part, it will be hard to see how consumer spending might improve in the coming months.

Coming this week

- This will be a full trading week, with fourth-quarter earnings reported all week. No Fed speakers are scheduled, but earnings reports could douse the markets.

- The initial fourth-quarter 2022 GDP reading will be reported on Thursday.

- Other data released this week will be secondary to the GDP reading and earnings. Leading indicators will be released on Monday, while mortgage applications and State Street Investor Confidence will come out on Wednesday. New home sales, retail and wholesale inventories will be reported on Thursday and consumer sentiment and personal spending numbers will be reported on Friday.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

1/23-2659492-4