AE Wealth Management: Weekly Market Insights | 2/12/23 – 2/18/23

Weekly Market Commentary

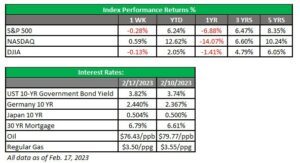

THE WEEK IN REVIEW: Feb. 12 – Feb. 18

Markets shrug off hot inflation data — then get nervous again

Markets were pretty stoic when the Consumer Price Index (CPI) for January came in higher than expected last week. Although CPI declined, it only dropped from 6.5% in December to 6.4% in January. Lots of reasons were given for the minuscule decline, but here’s a primary one: The relationship between higher gas prices and the increased cost of goods is not a casual or insignificant one. You need energy to make and transport products, and if those input costs are higher, your product will cost more.

The Producer Price Index (PPI) was also hotter than anticipated last week, which means that input and manufacturing costs will continue to be higher and prevent the inflation rate from dropping. The markets and the Fed keep slapping the pingpong ball back and forth (more on this in the next section), but the real culprits for stubborn inflation seem to come from governmental overspending and a broken energy policy, with its reliance on the whims of the international oil markets. Until we address those two factors, we could remain locked in this spiral.

Governmental overspending might be tamed during the upcoming debt ceiling debate, and we can certainly revert to proven policies to take the initiative toward becoming energy independent again and stabilize fuel prices. However, that would require the government to act boldly and decisively — characteristics that are glaringly absent in our current government on both sides of the aisle.

Back to PPI. Markets didn’t like the latest numbers, and they tumbled on Thursday to close out a poor week. Perhaps the most disturbing piece of data, however, was the Philly Fed manufacturing index, which came in at -24.3 versus expectations of -7.4. Any reading below zero signals economic contraction. It’s a stunning drop. If the trend is broader, the economy is in terrible shape and a difficult recession is imminent (more on that below). It’s time to explore obviously good ideas — like lower taxes, getting people back into the workforce and energy independence — to prevent a prolonged recession. Markets are generally optimistic, but optimism can only last so long, and right now it is wearing thin.

Inflation maintains its stubborn grip

Just when we thought the path forward was clear, we got a curveball. Both CPI and PPI didn’t continue the recent downward trend. Whatever the reasons behind this doggedly stubborn inflation, it throws the theory that the Federal Reserve may pause or pivot in 2023 into question. It had seemed as though once we hit peak inflation in June 2022 that tightening from the second half of last year would accelerate inflation’s decline and that we might even experience a light recession followed by a strong rebound.

Now it appears that, unlike volatile energy prices that fluctuate in the commodity markets, other items like food, housing and consumer goods will require a hard recession to force these industries to stop increasing or even lower prices. Right now, it doesn’t appear that the Fed will engineer anything other than a hard landing for our economy. It also doesn’t seem as though anything other than layoffs, the fear of layoffs and the deterioration of the wealth effect will slow demand. Consumers are already carrying record levels of credit-card debt; higher interest rates make servicing debt even harder, while layoffs will lead to defaults on that debt. Once manufacturers and service providers begin to lose significant sales, they, too, will be forced to lay off workers and lower prices. This race to the gloomy bottom will force the Fed to not only stop but to lower rates to correct what it has over-corrected.

Here’s my prediction: If the economy and the Fed continue on their current path, we will be in recession by late summer. Then the Fed will not only pause but will also aggressively begin cutting rates as we close out the year. I don’t see the Fed Funds rate rising above 5.5% before the Fed makes this shift. It seems like a good time for people to lock in higher rates, and we should all watch for a strong equity market to emerge later in the year.

Coming this week

- This will be a short (although busy) week. Three Fed members are scheduled to speak this week, and their comments might provide some insight into what the Fed is currently thinking.

- The minutes from the most recent Fed meeting will be released on Wednesday. We’ll see how insightful they are in light of the latest inflation readings.

- The second reading of fourth-quarter 2022 gross domestic product (GDP) will be released on Thursday.

- Other data of interest during this shorter week include existing home sales (Tuesday), mortgage applications (Wednesday), personal spending, new home sales and consumer sentiment (Friday).

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

02/23-2722061-3