AE Wealth Management: Weekly Market Insights | 3/5/23 – 3/11/23

Weekly Market Commentary

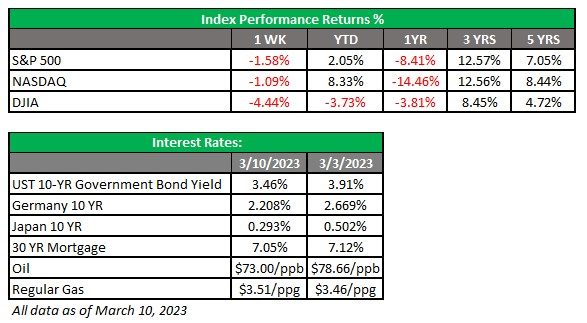

THE WEEK IN REVIEW: March 5 – 11

Powell disappoints markets – again

“More work to do” and be prepared to sit on higher rates, is what Federal Reserve Chairman Jerome Powell effectively told Congress last week. The Fed will likely raise interest rates more than expected to combat high inflation at their meeting next week, and after Powell’s testimony, a 50-basis-point (0.50%) hike was potentially on the table.

Despite a strong January for the markets, the big bounce in economic activity at the start of the year — particularly the strong hiring and spending reports — blew up the narrative and expectation that the Fed was close to pausing rate increases. The market has lost momentum and seems nervous, and Chairman Powell didn’t help calm the market when he told lawmakers the process of bringing inflation down to the central bank’s 2% target would be “bumpy” and could require a faster pace of rate increases.

After three months of easing, the year-over-year inflation rate (excluding food and energy categories) rose to 4.7% in January from 4.6% in December, as measured by the Commerce Department’s personal consumption expenditures (PCE) price index.

As expected, the market tanked at the outset of Chairman Powell’s testimony, dropping nearly 600 points last Tuesday. The freefall continued into Wednesday, then accelerated on Thursday in advance of the Bureau of Labor Statistics (BLS) jobs report on Friday morning. Needless to say, the jobs report didn’t help the market as it slumped like a beaten dog into the weekend. (More on that below.)

The lack of a story remains the story, as we have moved into a strange place where the market is looking for softer language from the Fed but the Fed is sticking to its tough talk until it sees enough weak data to show rate increases are finally impacting inflation. It almost feels like we’re waiting for the economic data wind to wag the Fed’s tail, which will, in turn, wag the economic dog. The problem with that type of scenario is the wind might end up needing to be so strong that it will blow the economy over and the Fed will have to reverse course very quickly to keep the economy on track.

The most likely scenario is that the Fed will wait for confirmation that inflation is tamed, which means it will raise rates far too high and will be forced to do an about-face because it will have driven the economy into the ditch. Once that happens and we re-enter a declining rate environment, the market will get on a roll.

The challenge right now is to stick to your convictions. Psychologically, investors experience a similar feeling to that of being in a dark place, trying to move forward with only a brief glance ahead of you before the lights go out. Your mind tells you what the path ahead is like, but the rest of your senses want to panic. I would say trust logic and history and do not give in to the urge to panic. And remember, it’s always darkest before the dawn.

Jobs just won’t give the markets what they want to see

Another strong jobs report last week fueled speculation that the Fed will stick to raising rates until it breaks the back of the labor markets and the wage inflation accompanying it. The problem? The economy is far more likely to break before the labor markets do.

Once again, jobs defied expectations and threw the market into a tizzy. The ADP employment report last Wednesday came in at +242,000 jobs, higher than the expectation (+205,000) and also higher than January (+106,000). The BLS employment situation (nonfarm payrolls) number, the most significant employment tracking statistic, was expected to come in at +225,000 after a very strong and surprisingly robust January reading (+504,000). Instead, we beat expectations again, adding 311,000 new jobs in February. Wage growth seemed to be slowing somewhat, but the slowdown in job creation just isn’t there.

This week’s consumer price index (CPI) and producer price index (PPI) readings might stir up the dust more about hints of a potential hike of 50 basis points at the Fed’s meeting next week. However, nothing is certain at this point. We continue to add jobs at a healthy pace consistent with a robust economy, and the Fed has only one lever at this point to slow them. If it sees a declining jobs market as the key to taming inflation, it’s hard to assume anything other than more rate increases on the horizon.

However, the problem with jobs data is that it’s rearward-looking, and the Fed and expectations of its impact are forward-looking. Some are concerned the Fed will overdo it. By the time the Fed figures out what it broke by examining all the scattered pieces, we could be in a recession. Then the Fed would have to whipsaw into rate cuts, leaving no period of elevated yield plateauing before we see a gradual decline in rates.

Coming this week

- The major hurdles this week will be CPI (4% year-over-year last month) on Wednesday and PPI (6.0% year-over-year last month) on Thursday. Both are coming down but not quickly enough to convince the Fed to stop raising rates.

- This week’s other economic data includes mortgage applications, retail sales, business inventories and the Atlanta Fed business inflation expectations (Wednesday); the Philly Fed manufacturing index, housing starts, import and exports, and Fed balance sheet (Thursday); and consumer sentiment and leading indicators (Friday). This is all significant data but will be noise compared to the CPI and PPI.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management. The information and opinions presented are those of Tom Siomades and do not necessarily reflect the views of the firm providing you with this report or AE Wealth Management, LLC.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

3/23-2773573-2