AE Wealth Management: Weekly Market Insights | 2/26/23 – 3/4/23

Weekly Market Commentary

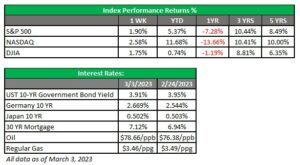

THE WEEK IN REVIEW: Feb. 26 – March 4

March picks up where January left off

Remember the phrase, “March comes in like a lion and goes out like a lamb?” As we closed out a turbulent February, where we gave back almost half of our sparkling January returns, March started much like February ended. Last week was mostly a sluggish market yawner; we saw a distinct downward bias early, then some “Fed speak” from Federal Reserve member Rafael Bostic boosted markets and helped us recoup losses to end the week.

We ended February and kicked off March at around 33,000 on the Dow, 4,000 on the S&P 500 and 4% on the U.S. 10-year Treasury. What’s going on? Did the market suddenly lose interest in itself? Is it due to the dead-of-winter gloom period? I think we all know that’s not the case.

After the economic data readings we’ve been discussing recently came in much higher than the markets and the Fed were looking for, the market’s preferred narrative unraveled. Until recently, the market felt that the Fed would pause and maybe even cut rates a few times in the back half of the year as inflation came down. And sure, inflation has come down from its peak last summer, but the magnitude of the declines has flattened. The market also didn’t believe the Fed when it said interest rates need to stay higher for longer to beat inflation.

Well, it seems the market believes the Fed now, if our results in February are any indication. With the data where it is, all the talk of a “soft” landing (slowing the economy just enough to lower inflation and not drive us into a recession) or even “no” landing (where the economy slows only to pick up speed without a recession) is out the window. The Fed seems committed to beating inflation. If that plays out, the odds favor an eventual “hard” landing (higher rates that crush economic activity and drive us into recession.) Interest rates could stay too high for too long and the recession will be more severe.

The market is looking for a new narrative, and that’s why it’s been behaving as it has. All the wishful talk of the Fed “threading the needle” and reducing inflation without harming the economy feels to be just that — talk. It was just one potential outcome, but if we ignore other plausible outcomes, we get a month like February. The Fed has clearly stated its focus is to tame inflation, even if it tanks the economy. We still think “too high” will not necessarily result in “too long.” We believe the Fed will break things and the economy will quickly unravel, but with 2024 (an election year) around the corner, pressure will be immense to restimulate the economy and the Fed will be forced into a position to cut rates. We’ll see what it actually does when the time comes, but the best bet right now might be to not fight the Fed, at least in the near term.

Sometimes 60/40 is just the right proportion

Last year, we heard from a lot of people that the 60/40 portfolio was anachronistic and passé. And if you looked at stock and bond performance in 2022, you’d probably agree. Stocks and bonds were both down, so a 60/40 split would equal a portfolio that was down for the year. But this year, as the stock markets wobble to and fro, bonds are actually doing what they’re supposed to do: zig when stocks zag.

Once again, for the record, we are not supportive of trying to time the markets. If you have a long time horizon for your investments, you should stick to your current age-appropriate strategic allocation. If, however, you are part of the crowd that abandoned fixed income in the recent low-yield environment or threw in the towel on a balanced portfolio after last year, it’s time to get back in the fold.

Although last year was disappointing for the traditional 60/40, no investment strategy is 100% effective. There has always been and will continue to be a relationship between risk and returns, and volatility is the price we pay for those higher returns. Although not foolproof, long-term investing generally leads to higher returns, but you have to be in the game in the first place. After all, to quote hockey great Wayne Gretzky, “You miss 100% of the shots you don’t take.”

Coming this week

- Two major forces will be on display this week. Fed Chair Jerome Powell will speak to Congress in what cognoscenti would refer to as the Humphrey-Hawkins testimony. This is the Fed Chair’s biannual report to both chambers of Congress, and what Powell says will either be reinforced or contradicted by the Job Openings and Labor Turnover Survey (JOLTS), ADP National Employment Report and Bureau of Labor Statistics (BLS) nonfarm payrolls number for February, all scheduled to come out this week. If the stars align, the market may find its new narrative. The tug of war between what Powell says, what the markets want to hear and the actual situation on the ground will be on full display this week.

- While jobs will be the big newsmakers this week, we’ll also see a smattering of economic data, including factory orders (Monday), wholesale inventories and consumer credit (Tuesday), mortgage applications, Beige Book, ADP and JOLTS (Wednesday), Challenger job cuts report and Fed balance sheet (Thursday), and the BLS employment situation (Friday).

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

3/22-2773573-1