AE Wealth Management: Weekly Market Insights | 4/21/24 – 4/27/24

Weekly Market Commentary

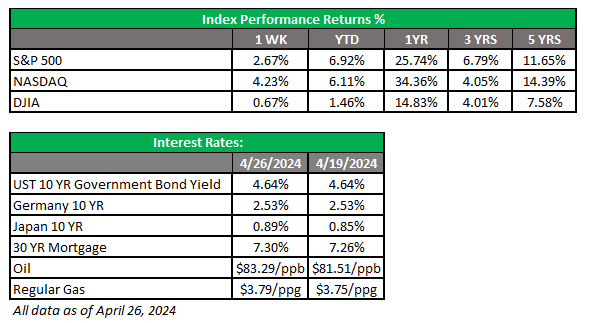

THE WEEK IN REVIEW: April 21-27, 2024

April showers continue

After a strong start to the week, markets took another tumble as first-quarter gross domestic product (GDP) decelerated much more steeply than anticipated on Thursday. The Dow was down over 700 points at one point and the S&P 500 was down over 70 points before recovering about half of the losses. Lingering fears of elevated inflation, recessionary worries and Friday’s personal consumption expenditures (PCE) report all combined with disappointing guidance and earnings reports from Meta and IBM to create a toxic environment.

Friday was much calmer with a nice rebound, and the market broke its three-week losing streak. PCE rose 0.3% in March, bringing the year-over-year reading to 2.7% (versus 2.5% in February). An increase was expected given the latest consumer price index (CPI) and producer price index (PPI) readings. Much of the angst and negativity was expressed on Thursday, but markets rallied to close out the week on a high note.

Personal income rose 0.5% in March and is up 4.7% in the past year. Somewhat troubling was that government pay rose 0.8% in March and is up 8.5% in the past year. The government is also spending less, which may help explain the decreased GDP number we just saw. Real GDP for the first quarter came in at +1.6%, significantly below the consensus of 2.5% and even outside the consensus range of +1.7% to 2.8%. Personal spending was the primary positive driver, while net exports (exports – imports) were the largest detractors. GDP dropped from 4.9% in the third quarter of 2023 to 1.6% just two quarters later, which is quite a deceleration.

In our view, this is what deceleration looks like: inflation outpacing growth. We are not outgrowing inflation, and that is exactly what we do not want to see. Once the government stops spending, the cracks of a fragile economy can’t be covered up. Sure, consumers are spending, but not as much as before, and for how long? The 1.6% rate is the slowest growth rate in almost two years. Inflation remains a big problem, while prices are up. This means short-term interest rates will stay higher for longer, and recession is in play. Earnings will be further hampered and markets will likely suffer. Let’s hope there’s not a bigger storm brewing, and we see the markets bloom in May after a stormy April.

Earnings contribute to the market’s turbulence

It’s important to note that not every market driver is macroeconomic. Sure, major data surprises, disappointments or confirmations keep things moving, but earnings are still the market’s lifeblood. Yes, the economic environment should be considered if the markets are to perform or stall, but if the underlying securities making up the markets aren’t healthy, all the negative macro news simply contributes to declines and volatility. No amount of great economic data will help if earnings are weak for a prolonged period.

After several years of higher inflation, higher interest rates and heightened regulations, companies are starting to show signs of weakness. The cost of doing business is rising, and it is much more difficult to pass costs on to consumers. Companies are having a hard time keeping up.

Last week was a prime example, with 30% of S&P 500 companies reporting first-quarter earnings. Verizon disappointed on Monday, but markets may have felt a little oversold from the week prior and we pushed higher. Tuesday brought some bright earnings from Spotify, General Motors and GE. Then we received the first estimate for first-quarter GDP. Markets reacted to the news as you would expect, but earnings disappointments from Meta added to the nervousness. We clawed some of the losses back, but the week was a classic example of how weakness in one area can make things worse somewhere else, and the combination can lead to dramatic market movements.

Coming this week

- The Federal Reserve isn’t expected to do anything with rates at its meeting on Tuesday and Wednesday. Chairman Jerome Powell’s post-meeting comments will be the highlight, as everyone will be listening carefully to see what he says about the direction of rates.

- The other big news this week will be April jobs. Last month, the ADP report stood at +184,000, and the Bureau of Labor Statistics came in at +303,000. Both need to show signs of weakness for markets to start beating the rate-cutting drums again.

- On Tuesday, we’ll see consumer confidence and the Case-Schiller home price index. Then MBA mortgage applications will be released on Wednesday.

- Finally, just like last week, there will be a lot of earnings reported, which can always throw markets off balance. We still have over 50% of the S&P 500 yet to report, including big names like Eli Lilly, Coca-Cola, Amazon, McDonald’s, Starbucks, Pfizer, CVS, Apple and ConocoPhillips.

Sources:

https://www.morningstar.com

https://www.cnbc.com

https://www.marketwatch.com

https://markets.businessinsider.com

https://ycharts.com

Accessed 04/26/2024

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

4/24-3481697-5