AE Wealth Management: Weekly Market Insights | 4/14/24 – 4/20/24

Weekly Market Commentary

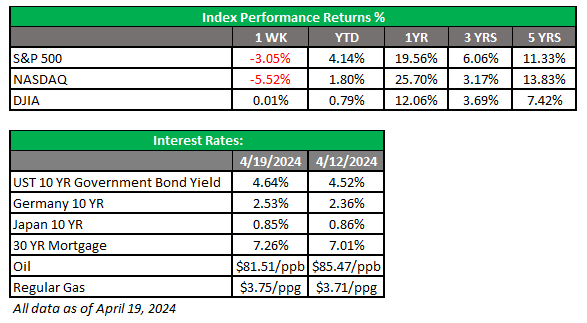

THE WEEK IN REVIEW: April 14-20, 2024

It was a bad month last week

The market’s pain continued last week, as Federal Reserve speakers doused hopes of coming rate cuts in the face of persistent inflation and continued strength for the economy and jobs. Adding to market misery was the anticipation of Israel’s possible response to a massive drone and missile attack from Iran. The drone attack was mostly ineffective; Israel shot down almost all the missiles and drones. Casualties were light, but sadly, one 10-year-old girl was severely injured by shrapnel.

The big news regarding the Iranian attack wasn’t that it was going to happen or that it was ineffective but it was the first time Iran fired at Israeli and U.S. forces from inside its own borders. That’s a significant change; prior to last week, Iran was using its proxy forces in Gaza (Hamas), Lebanon (Hezbollah), Yemen (the Houthis), and Iraq and Syria (the Islamic Resistance in Iraq) to attack Israel and U.S. forces in the region. Markets feared the Israeli response would target Iranian energy infrastructure and send oil prices soaring. They were also worried the conflict in the region would spill over into something larger, involving more nations.

Israel responded early Friday by targeting an Iranian military base in a very limited attack. Oil spiked overnight, but settled back to its recent levels on Friday. The worst didn’t happen, but markets were still very nervous and sold off most of the week. Bond yields didn’t benefit from any flight to safety, as Treasury yields oddly increased instead of dipping, as you might expect when people turn to bonds. Volatility rose by nearly 50%, shifting from a sleepy 12-13% range to over 18%.

Are we out of the woods? Not by a long shot. Israel isn’t a country that forgets, and they will respond when they feel the time is right. Until this crisis subsides, we will have to live with the volatility.

Fed speakers talking down rate cuts (more in the next section) only added to the tension, while lukewarm earnings contributed to the sour mood last week. However, with the exception of the last couple of weeks, all of the markets are up significantly from October 2023 lows. We’ve had a recent retraction, but that’s something we should expect from time to time in the stock market. We’re not overly concerned with the current state of the markets, but it’s always good to remember things can deteriorate quickly. Discipline, patience and vigilance are all in order.

Hope for rate cuts in 2024 begins to fade

Stubbornly high inflation, solid job growth and a resilient economy (according to the latest numbers, at least) have all converged to deny the directional data the Fed would like to see before starting rate cuts. According to the CME FedWatch tool, it is looking increasingly likely that we will not see a rate cut until September.

Fed Chair Jerome Powell spoke last Tuesday and offered the following: “We think policy is well positioned to handle the risks that we face.” He also said, “Right now, given the strength of the labor market and progress on inflation so far, it’s appropriate to allow restrictive policy further time to work.” That translates to no rate cuts until we see lower inflation, slower job growth and a softer economy. Powell did say the Fed was prepared to cut rates if the economy slowed significantly. That would also mean we were headed into a recession, and no one wants rate cuts under those circumstances.

We went from a possible six or seven cuts starting in March to three cuts starting in June — and now we’re at maybe one or two starting in September. But the longer the Fed waits, the less likely we are to get a rate cut. September is already uncomfortably close to the elections and cuts could be viewed as a political move by the Fed. We have said earlier that the window for the Fed was tight given the election, and for now the window appears to have closed for cuts in late spring and early summer. If we do see rate cuts, they likely won’t happen until November and/or December. That would be after the election, but will it be enough to revive sluggish markets and propel us to a strong ending to the year? Or will it be too little too late?

Coming this week

- On Tuesday, we will see March new home sales, which hopefully will climb from the 662,000 we saw in February. Wednesday will include durable goods and MBA mortgage applications.

- Earnings will be in full swing this week, and we will definitely get a feel for how good or bad this earnings season will turn out. Some of the better-known names reporting this week are: Verizon, Albertsons and SAP (Monday); Pepsi, Visa, Tesla, GM, UPS, JetBlue, Raytheon and Spotify (Tuesday); AT&T, Boeing, IBM, Meta and Ford (Wednesday); Merck, Microsoft, Alphabet, Caterpillar, Astra Zeneca, American Airlines, Comcast, Intel and Southwest (Thursday); and Exxon, Phillips 66, Chevron, HCA Healthcare[AR1] and AbbVie (Friday).

- The fireworks will start on Thursday with the first reading of first-quarter gross domestic product (GDP). We saw growth of 3.4% in the fourth quarter of 2023, and the Atlanta Fed is forecasting 2.9% growth in the first quarter of 2024.

- Finally, Friday will be all about the Fed’s favorite measure of inflation: personal consumption expenditures (PCE). If it stays in line with other data, it should be hotter. If it comes in cooler, we will start rallying as expectations for rate cuts perk up. However, it seems most likely that PCE will be a little hotter, which won’t sit well with an already jittery market.

Sources:

https://www.morningstar.com

https://www.cnbc.com

https://www.marketwatch.com

https://markets.businessinsider.com

https://ycharts.com

Accessed 04/19/2024

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

4/24-3481697-4