AE Wealth Management: Weekly Market Insights | 4/28/24 – 5/4/24

Weekly Market Commentary

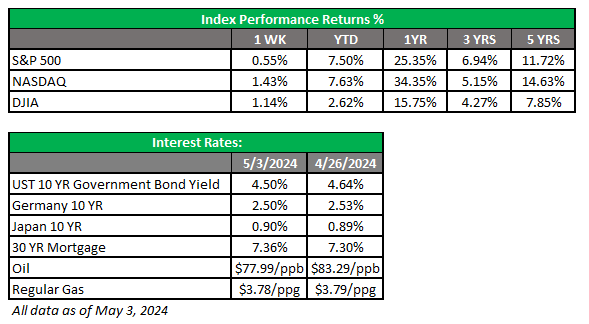

THE WEEK IN REVIEW: April 28 – May 4, 2024

Fed stays put

Expectations for a rate cut going into last week’s Federal Reserve meeting were practically zero. Markets were anxious to see what Chairman Jerome Powell’s post-meeting tone would be in light of continuingly stubborn and sticky inflation numbers. We are nowhere near the targeted 2% the Fed would like to see before considering rate cuts; in reality, we have trended higher in recent months.

Markets sold off hard on Tuesday, and it was the worst day for markets in over a year. In a brief four-month period, we have gone from expecting as many as six or seven rate cuts this year to anxiety that the Fed wouldn’t confirm no rate raises in the next few months. But Powell did indeed confirm the Fed plans to stay put (with the appropriate disclaimers, of course) and markets initially liked what they heard. The Dow was up over 400 points at one point during Powell’s press conference on Wednesday, swinging over 560 points and nearly recouping the prior day’s losses. Markets ended the day mixed, with the Nasdaq and S&P 500 both down and the Dow ticking up slightly.

The markets rebounded the next day as they took comfort in the Fed’s confirmation that a rate increase isn’t on the table, at least for now. Another encouraging sign was the easing of some of the Fed’s quantitative tightening measures, which is a stealthy way of cutting rates. The Fed has been unloading Treasuries to shrink its balance sheet, removing money from the economy and keeping rates higher. On this topic, the Fed commented, “Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion.” In theory, that will increase the money supply and potentially lower rates.

Markets were calm after the meeting, but what a letdown from where we were just a few short months ago. We went from six possible cuts to praying for rates to stay where they are for the rest of the year. But for the Fed to get us to 2% inflation, the amount of pressure would need to be immense and would lead to a recession. There are a lot of inputs to inflation that higher interest rates can’t quickly impact, like higher wages and housing. Pay cuts would do the job but that isn’t realistic, but if people lose jobs and their replacements are hired at lower wages that would also lower inflation. If people are forced to sell homes at distressed levels because they’re out of work and there aren’t many buyers to step in, that would drive down housing costs. All these are terrible scenarios in which the overall economy would have to suffer greatly.

Driving inflation down from 3.5% to 2% will take a long time to achieve, given where rates are currently. Rushing to drive inflation to 2% via further Fed rate hikes would lead to a recession — and no one is up for that. Fed Funds futures are currently saying we have about a 70% chance of a rate cut in September and another in November or December. But after what we’ve seen in the first four months of the year, the prediction of a possible November rate cut is almost laughable and utterly useless. The only good news is the market seems to have woken up to the possibility of no rate cuts this year and has hung in there, so when we actually get a cut, it will really get the markets moving.

Jobs come in soft, rescuing a nervous market

The Job Openings and Labor Turnover Summary (JOLTS) report for March came in at +8.49 million job openings. That’s the lowest number in three years and was lower than estimated. Quit rates eased and hiring continues at a slower rate. The ADP employment number released on Wednesday was stronger than expected for the corporate side, adding 192,000 jobs versus a consensus 175,000. ADP’s report covers more than 500,000 companies totaling more than 25 million employees.

We finally caught a break from the string of negative inflation readings on Friday. The Bureau of Labor Statistics (BLS) nonfarm payrolls reading for April came in at 175,000, well below the consensus of 243,000 and the range of predictions (190,000-303,000). Unemployment ticked up to 3.9% from 3.8%, and wage growth slowed more than expected while hours worked declined from the prior month. February’s payroll number was revised down from 270,000 to 236,000, while March was revised slightly upward from 303,000 to 315,000.

Markets clearly welcomed the weaker jobs data, which broke with the recent trend of hotter inflationary data. We managed to salvage a pretty bad week on Friday and finished pretty much where we started the week. The weaker jobs number reaffirmed the Fed will not have a reason to raise rates. Plus, with the unemployment rate creeping toward the psychologically important 4% threshold, markets will begin to buzz about the Fed having to do something about its second mandate, full employment.

So far, the Fed has been primarily focused on the first of its dual mandates, price stability or inflation. If jobs start to dry up, markets figure the Fed will need to pivot and cut rates to keep the jobs market healthy. Given the Fed’s posture of waiting on data before committing, we would need to see several more months of steady declines in jobs. The concern is that, just like the Fed was late to the inflation game, so too it may be late to bolster jobs because we may already be on the slide to recession.

Coming this week

- Fed officials will be giving their post-meeting perspectives this week, with many of them making the rounds.

- There will be little new economic data this week. We’ll see consumer credit (Tuesday), MBA mortgage applications (Wednesday), weekly jobless claims (Thursday) and consumer sentiment (Friday).

- Markets will still be digesting the Fed meeting and the April jobs readings, but we still have lots of earnings left to see. As of April 26, 46% of S&P 500 companies had reported results, with 77% of those companies sharing positive earnings per share and 60% reporting positive revenues. Earnings growth has been positive in the first quarter, with an earnings growth rate for the S&P 500 coming in at 3.5%. If that’s the actual growth rate for the quarter, it will mark the third straight quarter of year-over-year earnings growth for the index.

Sources:

https://www.morningstar.com

https://www.cnbc.com

https://www.marketwatch.com

https://markets.businessinsider.com

https://ycharts.com

Accessed 05/03/2024

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

5/24-3559928-1