AE Wealth Management: Weekly Market Insights | 5/5/24 – 5/11/24

Weekly Market Commentary

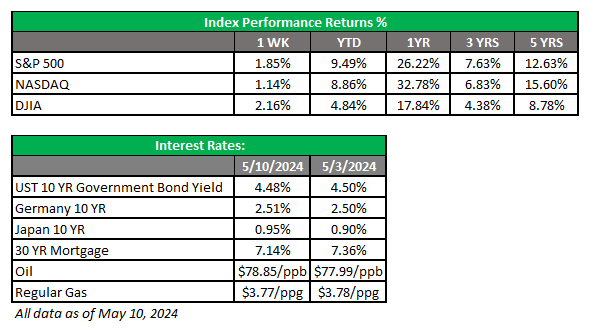

THE WEEK IN REVIEW: May 5-11, 2024

Calm before the storm?

Last week was quieter after the Federal Reserve meeting and the most recent jobs report. Markets resumed their upward march as the narrative of two to three rate cuts in 2024 was resuscitated. After a soft first-quarter gross domestic product (GDP) reading, Fed Chair Jerome Powell wasn’t as hawkish in his comments at the conclusion of the most recent Fed meeting, and he reiterated that there were no expectations for rates to go up from current levels. In addition, the April jobs report surprised to the downside as unemployment ticked closer to 4%.

That all seemed to calm the markets as we plowed ahead. Remember: Powell wants to cut rates and the markets want to push higher, so there is plenty of fuel to ignite the market. The fact that we are within a day or two of fresh all-time highs (except for the Dow, which has its quirks), pretty much tells you all you need to know about markets right now — and the word to describe the mood is definitely not “pessimistic.”

We are seemingly beginning to tread over familiar territory. The market will likely notch a new high and then begin to fret about the economy slowing, with the usual talk of “soft landings” and the Fed’s ability to manage a slowdown of the economy without driving us into a recession. That seems to be the nature of markets; in the absence of news, worry will fill the vacuum and volatility will creep in.

Here’s what we know: Consumers are still spending and earnings have been better than expected (more in the next section). But the economy is slowing and inflation is still a problem. Counting on the Fed to negotiate these cross-currents is pretty ambitious. The Fed can either raise rates or lower them, but there isn’t some sort of Fed mission control room that monitors and tweaks markets and the economy. It’s an election year and people are uneasy for several reasons. We have international tensions and markets will react to any developments, good or bad. The markets want to run right now, and until the news turns negative there seems to be no reason for concern. We aren’t close to recession territory, and the markets appear content with slower growth and the possibility of a rate cut or two. The closer we get to the election, the more the Fed likely will sit on its hands and hope things work out.

All this talk of engineering a soft landing — given that the Fed has never been able to achieve one — is probably just that … talk. Six months is an eternity for the markets. Stick to your plan, and if you are nervous, pull back into a more conservative allocation when we hit new highs. If your allocation is out of whack, rebalance. Focus on the long game. We could possibly see more volatility soon, but don’t let that distract you from your goals.

Earnings matter — and they always will

Earnings haven’t been a source of pain for markets. Instead, the linear relationship between interest rate expectations and inflationary data has caused market turmoil over the past month. Despite all the handwringing over rate cuts (how many, how soon), earnings have weathered higher rates and appear to be doing pretty well.

As of May 3, 80% of the S&P 500 has reported first-quarter results. About 77% reported positive earnings per share (EPS) surprises, while 61% reported a positive revenue surprise. EPS for companies in the S&P 500 now look to be up 5.2% from a year earlier, better than the 3.4% analysts expected at the end of March and marking the strongest growth in nearly two years. That’s pretty good, given short-term rates are around 5%.

Earnings kept the markets from dropping off aggressively last month, and now that we are perhaps seeing weakness in the economy and job growth, it may finally lead to the Fed cutting rates. It seems fair to say that barring a collapse into recession (which appears not to be the case), the news for companies can only get better if we see the Fed begin to lower rates.

Coming this week

- Most of the Fed speakers last week stayed on message, which is some form of a) “it’s too early to commit to cuts” or b) “we need to see the data that confirms what we are doing is working” or even c) “we need to keep rates higher for longer so inflation doesn’t come back.” We’ll hear from more speakers this week, and we’ll see what their tune is after the latest inflation data is released.

- Speaking of inflation data, we’ll get the latest Producer Price Index (PPI) and Consumer Price Index (CPI) numbers this week. CPI came in hotter than expected last month and inflation has been trending upward over the past few months. Needless to say, a cooling in the inflation readings will fuel more talk of cuts and get the market cranking upward.

- Other data this week includes retail sales, inventories and MBA mortgage applications (Wednesday) plus weekly jobless claims, the Philly Fed manufacturing survey, building permits and housing starts (Thursday).

- We will close out the week with leading economic indicators. Year-over-year growth remains negative but is on an upward trend.

Sources:

https://www.morningstar.com

https://www.cnbc.com

https://www.marketwatch.com

https://markets.businessinsider.com

https://ycharts.com

Accessed 05/10/2024

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

5/24-3559928-2