AE Wealth Management: Weekly Market Insights | 5/14/23 – 5/20/23

,Weekly Market Commentary

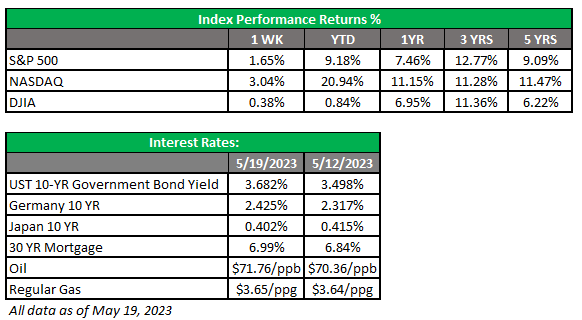

THE WEEK IN REVIEW: May 14-May 20

Dancing on the debt ceiling

As talks come down to the wire (again), the debt ceiling limit debate continues to loom over the markets and economy. You could barely turn around last week without hearing all the dire predictions of what could happen if we don’t raise the debt ceiling and the catastrophic results of a potential default. But both parties signed that default isn’t on the table and a deal will be reached, which calmed markets somewhat as the week wore on.

Simply put, there is a limit on the amount of debt the government can issue. And since the government spends an increasing amount of money over time, the ceiling needs to be raised periodically so that prior commitments can be met. Whether you agree on what the government is spending its funds on or how much it loans itself is another matter. We are still in limbo right now because Congress and President Biden seemingly haven’t felt pressure to fix the problem until markets really seem to freak out — and that hasn’t happened yet because they probably believe our elected officials aren’t dumb enough to default on the government’s debt. The fact is we have gone from no compromise on either side to possibly getting a “workable deal” soon. In fact, the talks may be so far along that the president felt he could go to Japan on a state visit and return on Sunday.

Ironically, in this situation, demand for U.S. treasury bonds goes up, while prices rally and interest rates decline. These are the same bonds that will not be paid if the government defaults. In times of uncertainty, U.S. bonds are considered a safe haven, even when the uncertainty stems from the possibility of them defaulting.

We may still be on the brink of a default, and any slight miscalculation could potentially blow up in our faces. We waited this long to address the problem, but market volatility has seemed to be benign so far. Bond yields have only begun to tick up in the past month as markets grew more nervous. If the debt ceiling is raised in time, we likely will quickly forget about it until next time. If something crazy happens, stock prices could drop and bond yields could then spike — and that would not be a welcomed development.

Market Funk

Equity markets have seemed nervous up until the past few trading days. But as the possibility of a debt deal appeared, markets began to push back to highs we saw in March. Now that the Federal Reserve appears to be finished raising interest rates, that source of worry seems to have subsided. And believe it or not, the markets think we may be in store for rate cuts before the end of this year.

After breaking the housing market and nearly breaking the banking sector, it appears the Fed has been frightened to the point where its desire to slow employment (and, therefore, the economy) may have gone just out of reach. The consumer price index (CPI) has declined from over 9% last June to 4.9% in April, and regular gas is hovering around $3.60/gallon nationally. This isn’t where the Fed would like to see inflation, but if the Fed continues to hike rates it would appear to be just plain mean and piling on to an economy with an already faint pulse. Jobs and consumer spending appear to have helped keep this economy limping along, but with rates much higher than a year ago and consumer debt piling up, an effort to crush job growth would have significant ripple effects on an already weakened economy and quickly spiral into a painful recession.

As we hopefully near a debt ceiling deal and put that conversation behind us, the markets will likely focus once more on the Fed and what it will (or will not) do in June and the rest of the year. It will be hard for the Fed to justify additional rate increases in the face of current economic weakness and remain “higher for longer” by resisting the pressure to lower rates and try to improve the economy ahead of an election year. Just like it takes time for rate increases to work, it also takes time for rate decreases to work their way through the economy. That process might be faster, but in order to make a difference by Election Day, the process needs to start earlier so it can be felt throughout the economy. The pressure on the Fed to lower rates sooner than it would like will be acute — and that could help equity markets later in the year.

Coming this week

- Debt ceiling negotiations will continue to be a big topic of conversation this week.

- The Producer Manufacturing Index (PMI) composite on Tuesday will give us a fresh look at the pace of inflation. New home sales will also be reported. Thanks to higher rates, the housing market is in limbo during the crucial spring buying season.

- On Wednesday, we’ll see the latest data for mortgage applications. We’ll also get the minutes from the last Fed meeting, which may give us some insight as to how close the Fed is to stopping rate hikes.

- The second reading of the first-quarter gross domestic product (GDP) will be out on Thursday. The first reading showed anemic growth of 1.1%. Pending home sales will also be reported on Thursday.

- There will be bond auctions all week. If debt ceiling talks turn sour, it may create some havoc with rates.

- Finally, on Friday, we’ll get the latest numbers on personal spending (in decline), retail and wholesale inventories (rising), and consumer sentiment (falling).

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

5/23-2876775-4