AE Wealth Management: Weekly Market Insights | 5/7/23 – 5/13/23

Weekly Market Commentary

THE WEEK IN REVIEW: May 7-May 13

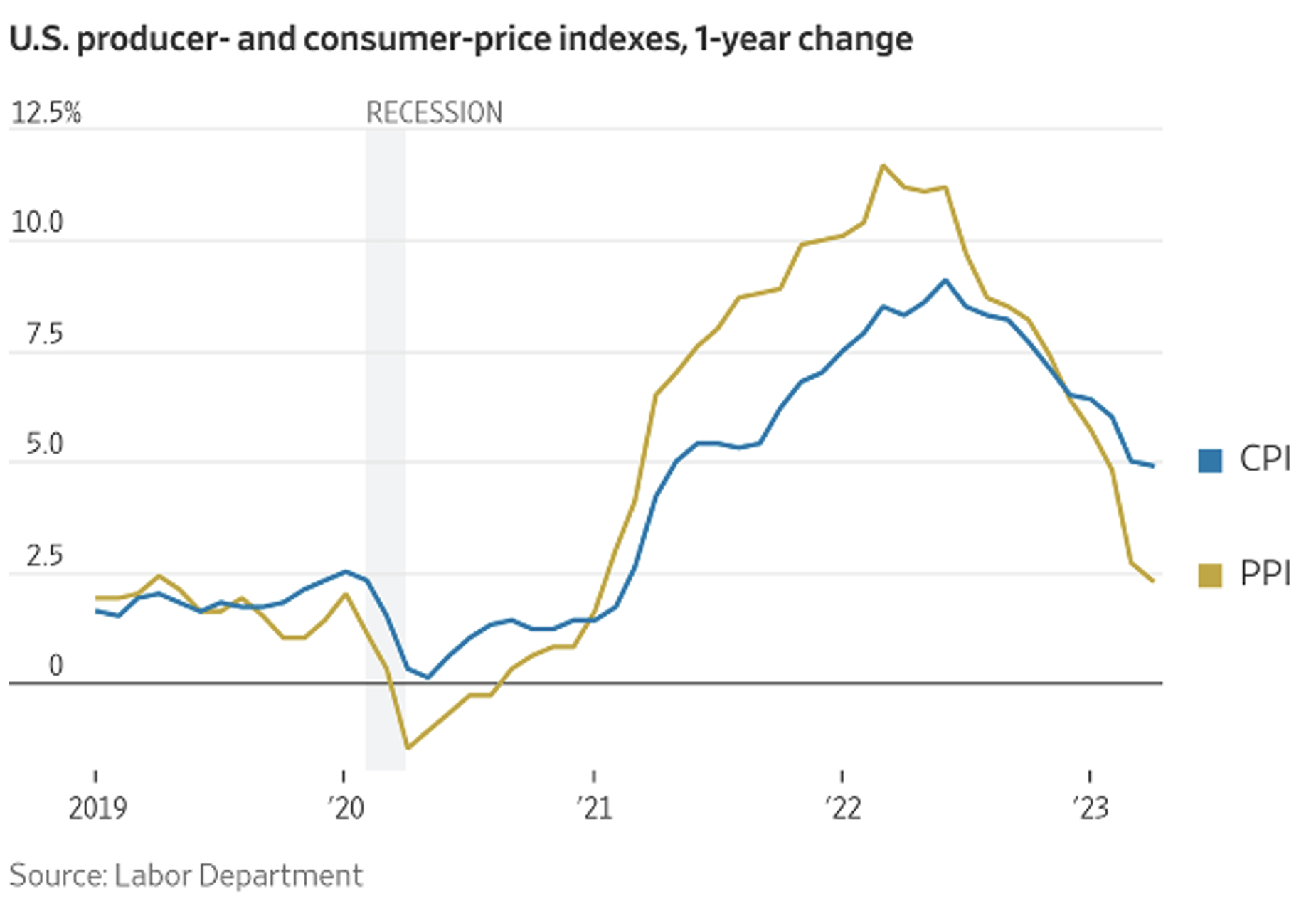

Inflation numbers tick down — but is it enough for Fed?

New inflation data came in last week. The consumer price index (CPI) came in at 4.9% year over year in April, just slightly under the 5.0% reading from March. It’s not much, but it should be enough to keep the Federal Reserve on course to pause interest rate hikes at its next meeting in late June. For those keeping score at home, the CPI was 9.1% in June last year, so it’s improved significantly over 10 months. However, it’s still more than double the Fed’s target inflation rate of 2%.

The producer price index (PPI), which generally reflects supply conditions across the economy, rose 2.3% in April, down from 2.7% in March. That’s good news for consumers; lower producer costs usually mean lower prices for consumers in subsequent months.

While the Fed may not hike rates again soon, cuts aren’t on the horizon yet. New York Fed President John Williams said last week that he does not expect a rate cut later this year. And in a talk to the Economic Club of New York, Williams commented, “We haven’t said we’re done raising rates.”

Although inflation isn’t slowing as quickly as the Fed had hoped, other signs of a cooling economy are also promising for a rate-hike pause. The Department of Labor reported that initial jobless claims from the previous week increased by 22,000, bringing the total to 264,000 claims for the week. That’s the highest level since 2021 and could be a clue that the labor market is beginning to slow somewhat.

The once red-hot housing market has also slowed significantly. The National Association of Realtors reported last week that home prices fell in nearly a third of U.S. metro areas in the first quarter of 2023. The housing slowdown can be attributed back to two things. The first is mortgage rates, which are still in the 7% ballpark. And the second is higher monthly payments due to those mortgage rates. The NAR said the monthly mortgage payment on an existing single-family home with 20% down is currently $1,859, an increase of 33% from just a year ago.

The ceiling is crashing in

Congress still hasn’t reached agreement on what to do about the debt ceiling, despite Treasury Secretary Janet Yellen’s warning that bad things will happen if we don’t take action by June 1. (Short recap of what’s happening: The debt ceiling was last raised by $2.5 trillion to $31.4 trillion in 2021. The government maxed out the new limit in mid-January, and if the ceiling doesn’t get raised, the U.S. may default on its debt.)

The impasse is happening along party lines: Republicans have said they’ll vote to raise the ceiling if spending cuts are also enacted, while Democrats just want to see the ceiling raised with no promises for cuts. What happens if the parties can’t reach an agreement? The U.S. may not be able to pay creditors, salaries for federal employees, or veterans’ benefits. It also won’t be able to fund Social Security.

The U.S. has never defaulted on its financial obligations, but it came close in 2011 when Congress waited until two days before defaulting to reach a consensus. Back then, the back-and-forth bickering and stalling depressed the stock market and led to higher borrowing rates for the U.S. Hmmm … sounds familiar.

Robbing Peter to pay Paul

The Federal Deposit Insurance Corporation (FDIC) said it plans to charge the country’s top banks $15.8 billion in additional fees over the next two years in an attempt to replenish the deposit insurance fund following recent bank crashes. Each bank will pay a specified amount based on a “special assessment” of which banks benefited the most from the coverage of uninsured depositors.

Meanwhile, lending officers at major banks said they have tightened standards in response to the banking failures. They also reported reduced demand for loans in the first quarter, probably due to both skittish borrowers and the higher cost of borrowing money.

Coming this week

- Fed officials will continue their rounds this week. Markets will be looking for signals of a potential pause next month or even rate cuts before the end of the year.

- Housing data will be on display this week. We’ll see the home builder confidence index (Tuesday), housing starts and building permits (Wednesday), and the latest numbers for existing home sales (Thursday).

- Other data this week will include retail sales minus autos and business inventories (Tuesday) and U.S. leading economic indicators (Thursday).

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

5/23-2876775-3