AE Wealth Management: Weekly Market Insights | 7/24/22 – 7/30/22

Weekly Market Commentary

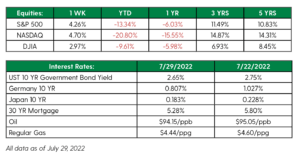

THE WEEK IN REVIEW: July 24 – 30

It’s official — U.S. economy is in a recession

Much has been made about the condition of our economy. After growing nearly 7% in the fourth quarter of 2021, first-quarter gross domestic product (GDP) for 2022 showed a contraction of 1.6%. Last week, the initial reading of second-quarter GDP showed a further contraction of 0.9%.

Technically, two consecutive quarters of contraction is a recession, defined as a period of temporary economic decline during which trade and industrial activity are reduced. Some will quibble about whether we are in a recession or try to define a recession in other terms, especially those whose political future may hang in the balance. Let’s put this into perspective: There are any number of positive things going on in the economy, just as there are any number of negatives. When combined, you get an overall picture of the economy — and the current picture isn’t a positive one.

Cherry-picking a few positive data points and ignoring the negatives is not an effective way to deal with our current challenges. You have to acknowledge a problem before you can fix it. Denial that we’re in a recession follows the same pattern previously taken about inflation: First it didn’t exist, then it was transitory and then it was someone else’s fault. Inflation continues to be a problem because no one wanted to take it on until it was too late.

If the same tactics are followed with the recession discussion, it could also be dragged out and likely make life worse for investors and the general public. Generally, since World War II, recessions have lasted on average six to 12 months, so theoretically we could be halfway through this current one. The closest comparison in recent memory to current conditions would be the 1981-82 recession, which featured the Federal Reserve tightening spending and increasing rates to lower runaway inflation. That recession lasted from July 1981 through November 1982 — at 17 months, a bit longer than average.

Given the lack of focus from policymakers, this recession could persist well into 2023. That doesn’t mean we won’t have a positive quarter here and there, but we could continue to be mired in a low-growth inflationary environment for some time. Confidence for a strong ending to 2022 is starting to wane.

Fed raises rates again; markets shrug off rate concerns

As expected, the Fed raised rates by another 75 basis points (0.75%) last week, bringing the total increase to 2.25% so far this year. Federal Reserve Chairman Jerome Powell did not provide any guidance as to what the Fed will do at its next meeting, which takes place in September, saying instead they will refer to the data. However, he did state the Fed was committed to bringing inflation down to a 2% level. He also denied we would be in a recession if we had a negative reading for the second-quarter GDP (which we did).

The market took the lack of guidance as a signal the Fed will not increase rates in September and rallied hard into the close on Wednesday. The rally continued to end the week, despite the confirmation we are officially in a recession. The markets clearly don’t respect the Fed and feel it is squeamish about going further with rate hikes as the economy heads deeper into recession.

That may be good news for the stock market, but it will not help tame inflation. With 2.25% in rate hikes so far this year and a stated 2% target inflation rate, the math shows we would need the Fed to increase another 4.5% to combat inflation, which is running at 9%. If they stop here, we can expect inflation to sit at about 7%. Ultimately, that will filter down to companies’ bottom lines and shares will likely tumble once more. As it is, markets have been ignoring what otherwise would be cautionary news in the most recent round of earnings and continue to rally on the hopes the Fed will stop because we are in a recession. But as we discussed earlier, policymakers do not appear to be acknowledging the situation. Is Chairman Powell looking for the slowing economy to lower inflation? That could be a tactic, but it is a risky one that might prolong the recession while inflation remains stubbornly high. For now, the markets appear to have no fear of the Fed.

Coming This Week

- After a really busy week with major announcements such as second-quarter GDP and rate increases from the Fed, this week won’t be as spectacular, but we will have some significant data announcements.

- On Tuesday, the latest Job Openings and Labor Turnover Survey (JOLTS) data will be released. Last month, job openings stood at 11.3 million. If we begin to see a decline in this number, it could mean one of two things: Either people who have been out of work are finally re-entering the workforce or openings are being cut before actual layoffs.

- On Friday, we’ll get the nonfarm payroll number for July. In June, we added 372,000 new jobs, and a decrease here would further the argument the economy is deteriorating.

- Finally, on Friday the unemployment rate for July will be announced. That number has been 6% for the past few months, and again, an increase here would not be a good thing.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

8/22-2330610-1