AE Wealth Management: Weekly Market Insights | 12/5-12/11/21

Markets shake off omicron and look to the Fed

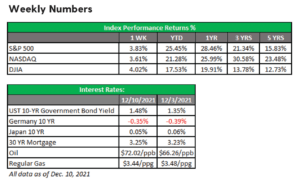

After selling off the week prior, markets decided the omicron variant likely is not something that will bring us back to the same places we were in initially with the coronavirus or delta variant. News of no new widespread restrictions, mandates or lockdowns was enough to get the markets to wipe out much of the prior week’s losses, when little was known about omicron’s severity.

It was interesting to see just how jittery the markets were with omicron, since they did not seem to behave similarly when delta was raging. In fact, the markets seemed to ignore delta through the spring and summer, when they were running up record after record and volatility was practically dormant.Why did omicron seem to have the opposite effect? Here’s one theory: The outlook seemed to be brighter back in the spring and summer. Back then, inflation wasn’t as big of an issue, supply chain challenges weren’t as prevalent as they are now and the government was discussing more massive spending. Plus, the Fed likely wasn’t contemplating tapering or rising rates, and there was still hope of an additional lift from an economy further reopening and growing. The markets liked the optimism early in the year and marched upward.

Fast forward to today: The market is skittish and seemingly unwilling (or unable) to absorb more negative news. Inflation is running three times the Fed’s target (more detail on this below). The Fed is tapering; in fact, they’re considering speeding up the taper and may even begin to raise actual rates by the first half of 2022, if not sooner. We’re dealing with fresh geopolitical worries from potentially aggressive Russian involvement in Ukraine to China’s increased belligerence toward Taiwan. And don’t forget to add in a slowing economy, with 11 million open jobs. There’s really nothing new on the horizon from Washington, and what is pending out there is perceived as unnecessary and inflationary. Add to all of this the fact that we haven’t had a meaningful correction for well over a year — no wonder things got volatile when a new strain threatened even more potential bad news.

In hindsight, we will look at this time as a clear signal that we were at an inflection point and should have taken action: either doubled down on our convictions, rebalanced back to targets we were comfortable with or taken on a more conservative posture. Whatever the case, this may be a time for action. We are at a crossroad, and the market has given us a rare chance and the rarer comfort of time to make a decision.

Inflation continues to rage

The Consumer Price Index (CPI) number for November came out last week. The report showed year-over-year consumer prices running at 6.8%, well over three times the Fed’s target rate of 2% and at a level we haven’t seen since 1982.

Inflation — which was at first ignored then touted as a good thing and eventually transitory — has now become the No. 1 topic of concern for Americans. Inflation was never really transitory; policy makers mistakenly thought inflationary pressures would just go away by themselves. The free markets are a wonderful thing, but when they are actively hindered and stymied, even they cannot perform miracles.

Now we’re in a slowing economy with high inflation, or what is commonly known as “stagflation.” The government is proposing to spend more borrowed money that will likely create more inflation in an effort to “fix” inflation. Let’s be clear: 6.8% inflation is a tax on everyone, because it leaves all of us with less to spend. Policymakers should have seen this coming and done something about it sooner. Now we will likely have to take a heavy-handed approach to stamping out inflation at the cost of everything else, and higher rates and economic pain may follow.

For now, the stock market seems convinced that higher prices can be and will be passed on to consumers, and earnings will remain healthy. As a result, the stock market in the short run is a pleasant place to be as we see inflation rise. The time may come, however, when the consumer will cry “uncle”and put a crimp on earnings, forcing the stock market to reprice. Again, this is a rare opportunity to reassess how we proceed from here.

Coming This Week

- The Fed will meet for the final time in 2021 this week. After last week’s inflation data and prior proclamations of inflation no longer being “transitory,” all eyes will be on whether the Fed speeds up the taper and if we can expect rates to rise sooner than the markets think they will.

- In addition to the Fed meeting, retail sales on Wednesday will gauge how things are going so far this holiday season. We’ll also need to monitor mortgage applications this week.

- Thursday will feature an extensive bond auction plus numbers on private mortgage insurance(PMI) and housing starts.

- Finally, Friday is a quadruple witching day. This once-a-quarter event happens when stock index futures, stock index options, stock options and single stock futures expire simultaneously. If we’re having a rough week through early Friday, quadruple witching will add more volatility.

Have a great week!

Tom Siomades, CFA®

Chief Investment Officer

AE Wealth Management

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The personal opinions expressed by Tom Siomades are his alone and may not be those of AE Wealth Management or the firm providing this report to you. The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

12/21 – 1946501-2