AE Wealth Management: Weekly Blog Insights | 10/31-11/6/21

The Fed makes its move

The much-telegraphed taper was announced after the Federal Reserve concluded its meeting lastWednesday. Markets didn’t seem to notice the very real fact that additional liquidity would be removed to the tune of $15 billion per month. Remember, the Fed was adding $120 billion total per month in quantitative easing; at this rate, we are looking at eight months (June 2022) before additional liquidity is removed entirely, and we will have to consider whether the Fed will raise rates. There will still be money sloshing around until then — and eight months for the markets is an eternity.

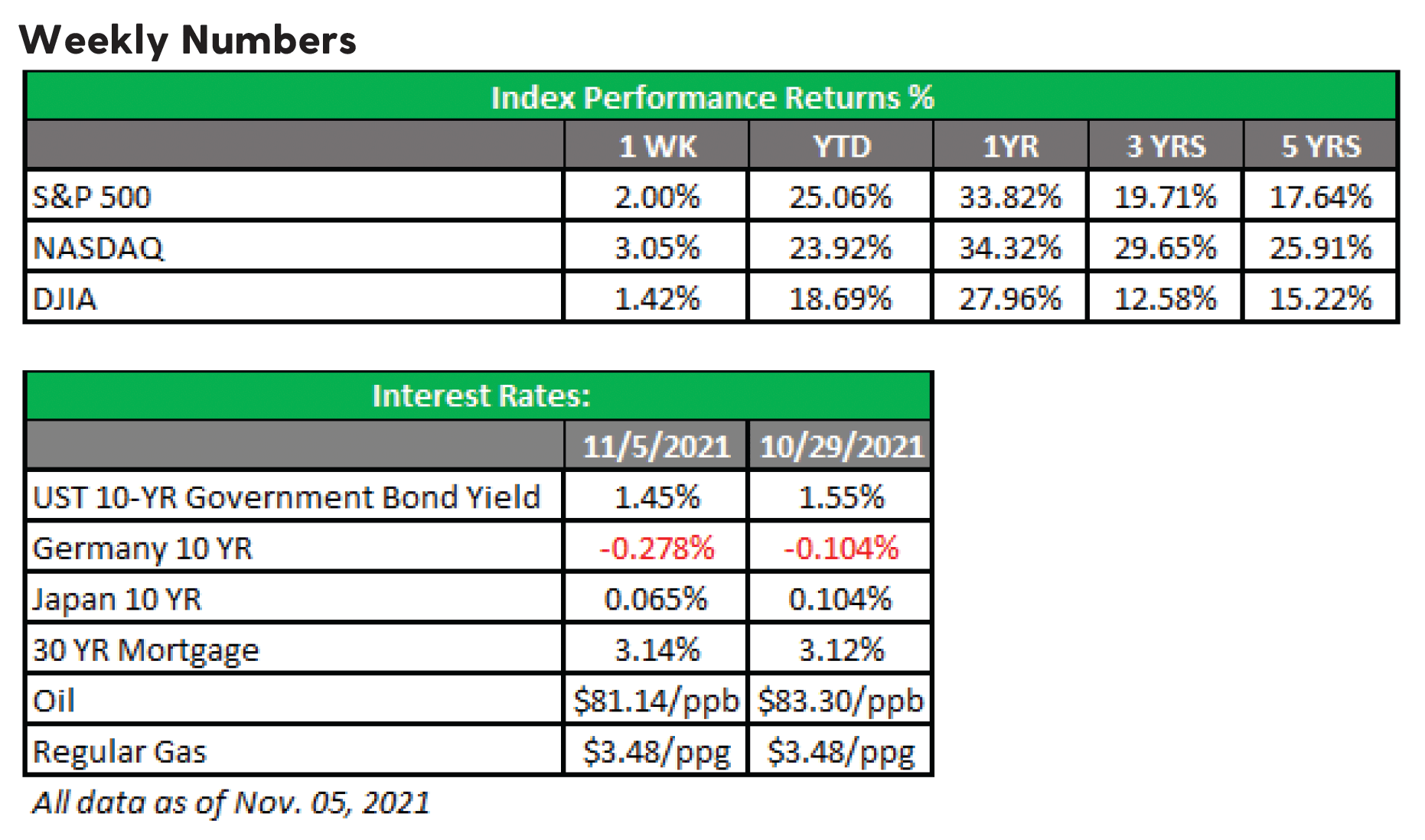

Speaking of the markets, last week was another week of records. (The Dow and S&P 500 have posted over 40 and over 60 new highs so far this year, respectively.) After a rocky September, a historically scary October failed to deliver on the gloom-and-doom predictions. Instead, thanks to solid earnings, we are now over 36,000 on the Dow and 4,600 on the S&P 500.

Paradoxically, we seem to be in a place where more aggressive action by the Fed, such as the removal of liquidity, hasn’t impacted the markets. Eventually, rates will rise and the adage of “Don’t fight the Fed”will come to pass. Right now, the markets seem to be oblivious to rate hikes. The 10-year Treasury has dipped below 1.50% yield again, while volatility has remained mostly comatose the past few weeks, hovering around the 15-17 range.

Infrastructure done amid off-cycle election fallout

After some high-profile elections around the country took up most of the airtime in Washington last week, the House finally voted on the infrastructure bill late Friday. The vote effectively decoupled the link between the infrastructure bill and the Build Back Better legislation. President Joe Biden and House and Senate leaders have been telling us for the past few months that the two bills would move together. The impasse was that progressives within the Democratic party were holding out for more social spending in the reconciliation bill (Build Back Better) while holding up voting on the infrastructure bill. At the same time, more moderate Democrats were concerned about the cost of the reconciliation bill. With a few Republicans and progressives supporting the infrastructure bill, the die-hard, all-or-nothing contingent was outmaneuvered.

The challenge is that the recent elections made some moderates nervous. They are less likely to support additional spending if they risk losing their reelection bids and cannot show anything of their efforts in Washington. With infrastructure, everybody wins — making that legislation more appealing. The passage of the infrastructure bill makes the Build Back Better legislation

even less attractive to moderates, which was probably why the progressives wanted the two bills linked in the first place.The debt ceiling deadline is also creeping closer and closer, and the Republicans have already said they will not help with that issue. As we head into the holiday season, it’s good to remain mindful of these issues that could have a pretty big impact on the markets.

Jobs return?

Following two miserable monthly jobs reports, October’s Bureau of Labor Statistics (BLS) nonfarm payrolls were better but still not gangbusters. The October number came in at +531,000, while the prior two months were revised upward but nowhere near the +700,000 readings forecast for those two months. October’s estimates were for +450,000 and the actual number easily beat that, but if you lower your expectations enough, then a modest result looks really good.

Two main reasons were given for the low job growth in August and September. The first was that the delta variant of the coronavirus was holding back job seekers. The second was everyone would flock back into the job market in October after enhanced unemployment benefits rolled off — predictions were that we would see closer to 1 million new jobs that month. It’s all in the messaging: Here’s one take on Friday’s numbers from The Wall Street Journal: “After two months of disappointment, the job market roared back to life in October, adding 531,000 jobs, while private payrolls jumped 604,000.Both were the most since July and both beat expectations. The unemployment rate dropped to 4.6%from 4.8%. For a change, the numbers were better than expected.”

Obviously, 500,000 new jobs is not 1 million. We also still have nearly 11 million openings, which hopefully the Job Openings & Labor Turnover Survey (JOLTS) report this week will show are declining.Then again, it depends on whether you’re a “glass half-full” or “glass half-empty” type of person. Right now, we’re in the latter camp and unconvinced that the situation is materially better.

Coming This Week

- The rate of increase in inflation should be slowing — or so we’re being told. We’ll see if that’s really the case as we get readings on the Producer Price Index (PPI) on Tuesday and ConsumerPrice Index (CPI) on Wednesday.

- Now that the Fed has announced its tapering plan, Fed officials will be out in force giving speeches this week.

- We’ll check in on consumer sentiment on Friday and see if the record number of job openings has declined with the JOLTS report.

- Finally, Thursday is Veterans Day. Bond markets are closed, but the stock market will be open normal hours. Most importantly, seek out a veteran and thank them for their service to our country.

Have a great week!

Tom Siomades, CFA®

Chief Investment Officer

AE Wealth Management

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The personal opinions expressed by Tom Siomades are his alone and may not be those of AE Wealth Management or the firm providing this report to you. The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

11/21 – 1901033-2