AE Wealth Management: Weekly Market Insights | 4/17-4/23/22

VIEW PDF VERSION

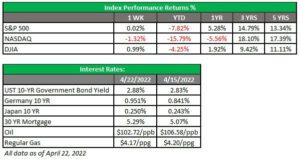

Chaotic week for markets

Q1 2022 GDP and where this economy is headed

After growing by 5.5% last year, some analysts predict a major economic downturn. Gross domestic product (GDP) grew by 6.9% in the last quarter of 2021, and now some expectations are calling for growth to slip to 1.5% in the first quarter of 2022. Why the slowdown? The usual culprits are to blame: inflation, the war in Ukraine, the Federal Reserve, COVID, the government, etc.

The price of gas, inflation and rising interest rates are likely the primary drivers. As terrible as the war in Ukraine is, that conflict currently is not impacting our economy as much as some might say. Be wary when you hear people blaming the war in Ukraine for all their failings. To be sure, the war increased already-high gas prices and led to an increase in volatility. But fuel prices, interest rates and inflation were already on the march before Russia invaded Ukraine. The current administration’s war on fossil fuels made us vulnerable to other global producers like Russia. Regulations, red tape, the extension of COVID benefits and more stimulus caused delays in the economic reopening and created supply chain hiccups. All this helped lead to the currently elevated inflation levels. With consumers feeling the impact of the past and current administrations’ decisions right in their pocketbooks, it gives the appearance that there is dysfunction in our government. It’s also leaving Americans to wonder what the current administration’s plans are for long-term relief as the economy finally wears down.

Q1 earnings strong so far— but can they continue?

Corporate earnings released this week with Delta Air Lines posting strong profits. It’s no surprise with airfares having risen substantially since the beginning of the year. But how long will it be before people cannot pay for tickets that have doubled in price over recent months for certain destinations? Overall earnings have been fairly strong, but that has been on the back of higher prices rather than growth. How to sustain strong earnings is the real question, and given all the headwinds the economy is facing, plus a flagging consumer, it will be difficult for earnings to remain strong. Higher interest rates meant to tame inflation will further squeeze earnings since more will be required to service new and existing debt. Dropping from a 6.9% growth rate in the fourth quarter of 2021 to potentially a 1.5% growth in the first quarter of this year may not seem like a big deal to some, but a decrease of 5.4 percentage points is a big deal. It’s fair to worry things may worsen in the second quarter, especially if the Fed overdoes it with interest rate hikes.

On the tails of earnings reports, FAANG (Facebook, Apple, Amazon, Netflix and Google) stocks lost a tooth this week when Netflix missed on earnings and announced a net subscriber loss for the first time. Netflix’s management blamed much of the loss on the Russia-Ukraine conflict and their decision to pull out of Russia.

Yet, here’s the thing: Netflix had disappointed in one way or another in the past four earnings calls. People exhausted Netflix’s content library during the lockdowns, and folks also have more streaming services to choose from as that segment gathers steam. The cost of content keeps rising due to competition from other streaming services, including Disney+, HBO Max, Amazon, Paramount, etc., and Netflix raised its subscription price in response. The surprise was that people got excited in advance of the earnings announcement and — predictably — were disappointed for the fifth time. Netflix lost one-third of its market cap last Wednesday.

Then there’s the Elon Musk saga over on Twitter. The social media platform has struggled with profitability since its IPO and has been looking for a buyer ever since. Disney and Salesforce walked away, and things didn’t work out with Facebook.

All that said, Twitter is a glorified electronic billboard allowing anyone to say whatever is on their on their mind to whoever is open to receiving it. You can simply yell “I HATE BRUSSELS SPROUTS” and be done. The one benefit for public figures not wanting to be filtered and wanting more control over their message is the ability to bypass the traditional media and instead reach out directly to their followers. Predictably, in our divided society Twitter has been politicized, and some groups or stories have been banned (most notably former President Trump). In contrast, others were allowed to continue tweeting (the Chinese Communist Party, Iran, etc.). Enter Elon Musk, who has said he is more concerned about leveling the free speech field than making a profit. He also can afford to see it differently with a personal fortune north of $200 billion.

Where is the lesson here? These two stories simply illustrate what we have been saying about the status of the market and our economy. We have an unprofitable, controversial company that is unwilling to be bought when it has been trying to sell itself for 15 years and a group of companies that were previously lockdown winners and have now been played out. There is nothing bold or exciting to get this market moving, so we are mesmerized by the Twitter-Musk drama. Hey, maybe Netflix can do a series on that?

The Fed’s making moves in May

Finally, Fed Chair Jerome Powell helped drive markets downward last Thursday and Friday by confirming the Fed will raise rates by 50 basis points (.50%) at its next meeting in May. At the same meeting, the Fed will also detail the winding down of its massive $9 trillion balance sheet. Will Powell deliver on his talk? It remains to be seen.

We’ve already had all this volatility and we’ve only moved 25 basis points (.25%). What happens when we move 200 or 300 more basis points (2-3%)? If the Fed is serious about combating inflation, raising rates by three-quarters of 1% in the first half of 2022 and at a .5% pace after that is unlikely to cut it.

Coming This Week

- On Thursday, the first quarter GDP will be announced. This indicator of economic data is expected to show a significant slowdown from the fourth quarter. Since a slowdown is widely expected, it will be interesting to see how the markets and the Fed react. A stronger-than-expected number may encourage the Fed to move more aggressively, as they will perceive the economy as being strong enough to handle higher rates. A weaker-than-expected number will throw the market into fits with concerns that the Fed is driving us into a recession if it continues to raise rates.

- New home sales and consumer confidence will be reported on Tuesday. Both have been sliding as of late.

- Mortgage applications and pending home sales plus retail and wholesale inventories will be released on Wednesday.

- After the GDP report on Thursday, we’ll see personal spending data on Friday. It will be a busy week for data and earnings, giving us a healthy picture of where we’ve been, where we are and where we’re going.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

4/22-2109496-4