AE Wealth Management: Weekly Market Insights | 5/1-5/7/22

View PDF Version

Markets move wildly as Fed makes announcement about rates

The Fed makes its move and markets react

Last Wednesday, the Federal Reserve raised rates by 50 basis points (.50%), its biggest hike in 22 years. The Fed had already raised rates for the first time since 2018 at its March meeting, moving the Fed funds rate from 0.0 to 0.25%. The latest increase moves the rate from 0.25% to 0.75%.

Markets were fretting about the potential pace and magnitude of rate increases and had been mostly in a glum mood leading into the Fed’s May meeting. April was a brutal month for both stocks and bonds, leaving investors with seemingly no place to hide. With inflation worries, a negative first quarter reading of U.S. gross domestic product (GDP), a mostly OK earnings season, and the continuing Russia-Ukraine war, there wasn’t really anything positive for the market to rally around.

So, all eyes were on Fed Chair Jerome Powell as he stepped up to the mic in his first live press conference since the pandemic. He announced the Fed’s decision to raise rates by 50 basis points (.50%). Then he went on to say there would be no chance that the next increase would be 75 basis points (.75%), but instead the next several hikes would be 50 basis points. In response, the market went wild. After being flat and meandering for most of the day, the Dow rocketed nearly 1,000 points in the last 1.5 hours of trading. Chairman Powell’s comments had the desired effects, and we experienced a massive relief rally on Wednesday.

Like some parties, when people overdo it there’s often a hangover the next day. Upon further review, the market appears to have decided it doesn’t believe Chairman Powell’s claim and now sees a high likelihood that the Fed will bump rates by 75 basis points at their June meeting. The apparent contrast drove markets down on Thursday just as sharply as they’d risen on Wednesday.

Here’s how it looks to shake out: If the Fed believes the market can take higher rates to cool the red-hot employment and housing markets and tame inflation, they’ll need to make significant raises. If you increase rates to only 1.7% when inflation is running at 8.5%, an attempt at a “soft landing” likely won’t happen. (They’re not even near an airport at those levels.) Also, the Fed has never managed “soft landings,” so what makes us think they can accomplish it now?

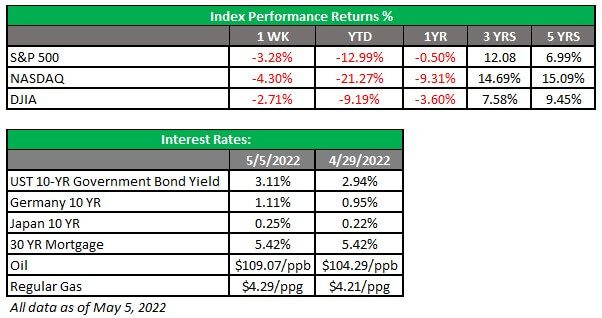

Markets were negative most of the day on Friday, and a strong April jobs report did little to pause the Fed from raising rates. A strong jobs report would normally be a good thing, but in this case, a weaker report might have forced the Fed to reconsider raising rates because the economy might do some of the heavy lifting. It still seems the Fed is unwilling to make the hard choices and is expecting outside forces to bring inflation back in line. They were late to the game and are not as fully engaged as they need to be. The markets are leading the way as we see the 10-year Treasury over 3% and 30-year mortgages over 5%. The concern is that the Fed will lag while the markets bob around and slide downward. If the Fed overcorrects, the economy will slip into recession. Not a great choice.

Fixing inflation is not as simple as some say it is

Inflation — and the inputs creating it — is no longer just the Fed’s problem. Sure, the Fed can help by raising rates. Doing so will slow borrowing and economic activity, as firms make less investments and workers compete for lower-paying jobs.

But some factors outside the Fed’s control are contributing to inflation. The Fed cannot stop the Russians and Ukrainians from shooting at each other and the subsequent effect on energy and commodities (wheat, corn fertilizers, etc.). The Fed cannot order the production of more oil and natural gas, and it cannot stop the U.S. government from borrowing and spending more. The Fed cannot lift the lockdowns in China or restart the flow of goods to ease the supply chain.

What the Fed can do is work in tandem with the federal government to curb inflation. If the federal government commits to rebooting our domestic energy production, it will send a huge message to oil markets that we are going to produce enough to moderate and stabilize oil and natural gas prices. Then gas prices would fall, easing the burden on consumers.

We can also onshore more (if not all) production to the United States, or at least our hemisphere. Doing so would make us less dependent on China and other overseas producers and allow us to eliminate a significant length of the supply chain. We can produce more wheat, grain, corn, etc. to export. All these initiatives would need the support of the government, which so far has not stepped up in these areas. Solving inflation is not as easy as the Fed playing with rates. Instead, it will need a willing partner to help. So far, the federal government has not been willing to step up.

Coming This Week

- While last week was all about the Fed, this week will feature inflation. Consumer Price Index (CPI) and Producer Price Index (PPI) data for April will be reported on Wednesday and Thursday. Inflation continues to climb, and expectations are for an increase in the CPI from the last reading of 8.5%. Surprises are always possible, but lately the surprises have been negative — so no surprises, please.

- Now that the Fed meeting is over, the gag order for Fed officials is lifted and we will see multiple speakers this week. After Chairman Powell asserted that a 75-basis-point hike wasn’t on the table and markets were not confident that was true, it will be interesting to see just how unified the voting members of the Fed were on the “not doing 75 basis points” position. Again, surprises here can move the markets — and as we saw last week, it could be significant and very quick. We have traditional centrist, dovish and hawkish speakers scheduled this week, so opinions will vary.

- Mortgage applications data will be released on Wednesday. With conventional rates above 5% for a 30-year mortgage, the number of applications could start to drop.

- Consumer sentiment will come out on Friday. This metric has been waning, and more deterioration will not be welcomed.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

5/22-2180545-2