AE Wealth Management: Weekly Market Insights | 12/31/23 – 1/6/24

Weekly Market Commentary

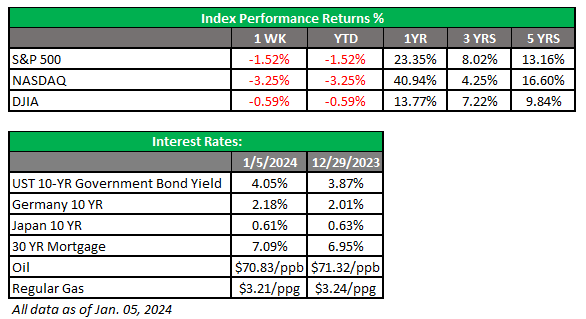

THE WEEK IN REVIEW: Dec. 31, 2023 – Jan. 6, 2024

Market stumbles out of the gate

Markets had a rough start to the year last week. The drop could have been due to a number of things: Folks taking profits to push capital gains into 2024, concerns over the continuing (and possibly escalating) war in the Middle East, or the Federal Reserve’s meeting minutes showing the Fed isn’t completely ready to lower rates. Whatever it was, the combination of these events seemed to conspire to send the markets skidding downward in the first days of 2024, as investors grew more cautious and reverted to the safety of bonds, which resulted in rising yields. The 10-year U.S. Treasury, which finished the year yielding around 3.9%, popped back over 4%.

Let’s keep things in perspective. The economy is still slowing. But holiday spending was decent, unemployment is still relatively low, and interest rates aren’t going up. Everything is still in place for the Fed to cut rates in the summer, and we can still manage a soft landing. The forces that drove us upward in the final two months of 2023 are still in place. Barring a major international incident that shocks global oil supplies and gets us into a conflict or some disastrous government shutdown, we should be set for a strong open to 2024.

Sure, there will be jitters, and the market wants six rate cuts instead of three — but we aren’t talking about rate increases anymore! Inflation remains higher than the Fed wants, but the risk of pushing the economy into a recession is a far greater worry than being 1-percentage-point above their 2% inflation target for a while.

We’re also in an election year, and the Fed is far more likely to be timid with any talk of hiking rates. No incumbent running for reelection wants to face angry, unemployed workers at the polls. In fact, incumbents are far more likely to lean on the Fed to lower rates to improve the economy and ensure we don’t slip into recession, at least until after the election. We will see rate declines eventually, which the markets will like. Don’t let a slow, short opening week taint your view for the rest of the year.

Continued strong jobs data complicates the “more rate cuts sooner” narrative

Jobs continue to hang in there. The ADP employment report surprised to the upside last Thursday, showing we added 164,000 new private-sector jobs in December. This was higher than the consensus +115,000 and significantly above November’s growth of 101,000 jobs.

The Bureau of Labor Statistics (BLS) employment situation (better known as non-farm payrolls) was anticipated to be lower than November’s +199,000, with the consensus calling for 158,000 jobs to be added in December. In reality, the BLS number came in much higher than expected at 216,000.

Neither of these readings was so out of line that they would cause concern, either from the standpoint of the Fed having to resume raising rates to cool a hot jobs market or that the economy was so bad that we should be alarmed about a looming recession. Both reports showed there wasn’t a need for the Fed to act further and made a stronger case for lowering rates if the economy slows more and job gains remain muted.

Coming this week

- The early part of this week will be pretty uneventful. We’ll see some consumer credit data on Monday and the trade deficit on Tuesday. Then we’ll get wholesale inventories, MBA mortgage applications and comments from New York Fed President John Williams on Wednesday.

- The real action will take place on Thursday, as we get the December consumer price index (CPI) and Core CPI readings. Inflation has been trending down largely due to lower energy costs, as the other components used to measure inflation (such as housing and food prices) have remained stubbornly higher. Last month’s CPI reading was 3.1%; expectations are for a slight increase. However, the rise shouldn’t be so dramatic as to alter the current thesis that the Fed will hold steady on rates and begin cutting them later in the year.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

01/24-3302609-2