AEWM Wealth Report – 7 Things to Know About Social Security Before Starting Benefits

Download PDF Version

Social Security is a significant source of income for many retirees. Your financial professional can help you explore your options and make sure you’re getting the most retirement income possible.

Overview

For many Americans, Social Security is a primary source of income in retirement. But understanding how benefits work and when you should start your benefits can be confusing. Here, we break down seven basics you should know about Social Security benefits before you begin receiving monthly payments.

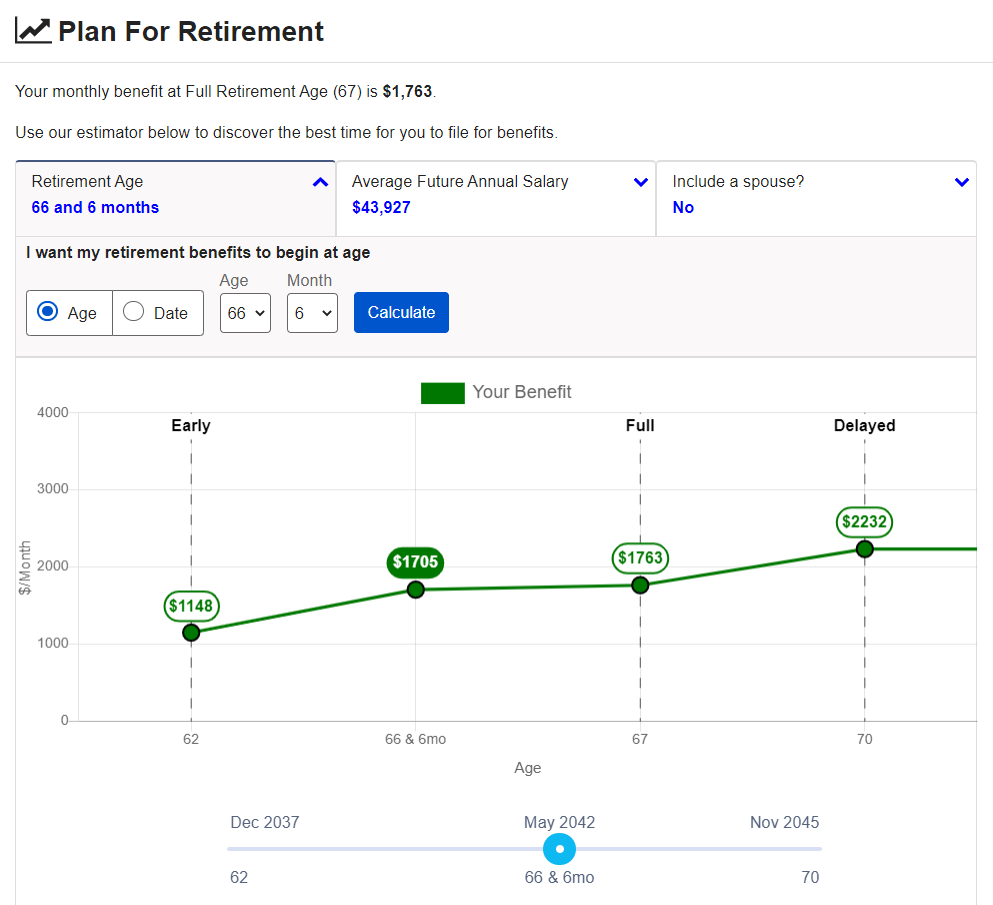

1. You can know exactly how much you’re eligible to receive.

One of the most common questions we get is, “How do I know how much I’ll receive every month in Social Security income?”

When you log in to www.ssa.gov/myaccount, you’ll see a summary including your payment amount when starting benefits early, waiting until full retirement age or delaying payments until age 70. The interactive tracker lets you see how much your benefits will be at different ages.

Source: www.ssa.gov/myaccount. The above image is for example only. Your benefits will vary based on age, work history, full retirement age, and past and future earnings.

Your benefits are calculated using several variables, including number of years in the workforce, average annual earnings and full retirement age. Since these variables are always changing, it’s a good idea to check the monthly benefits calculator annually to get an updated estimate of your future Social Security income.

2. The right time to start taking benefits is different for everyone.

Deciding when to begin taking Social Security benefits is a big decision. Start them too early, and you could end up with less income during your later years than you need. But if you start too late, you run the risk of depleting your other retirement savings or even dying before you have the chance to take much of what you’ve earned.

Every American is currently eligible to begin Social Security benefits at age 62. But use caution: If you begin taking income earlier than your full retirement age, you’ll receive a discounted monthly amount. For every month you wait to start benefits, you’ll earn a little bit more, up until age 70.1

Your FRA is based on your year of birth:

| Year of Birth | Full Retirement Age |

| 1943-1954 | 66 |

| 1955 | 66 and 2 months |

| 1956 | 66 and 4 months |

| 1957 | 66 and 6 months |

| 1958 | 66 and 8 months |

| 1959 | 66 and 10 months |

| 1960 and later | 67 |

Source: Social Security Administration. www.ssa.gov/benefits/retirement/planner/agereduction.html

There’s no one-size-fits-all when it comes to starting benefits. One person might benefit from taking Social Security income as soon as they’re eligible at age 62; another might be better served to wait until age 70.

(Side note: Your benefits stop growing after you turn age 70. So make sure to start your benefits — or you could be leaving retirement income on the table!)

3. Your Social Security benefits could increase your taxable income.

Yes, you can keep working while receiving Social Security benefits. If you’re under full retirement age, your benefits will be subject to the earnings test and reduced by $1 for every $2 over the earnings limit. (The earnings limit is $21,240 in 2023.) Then in the year you reach full retirement age, your benefits are reduced by $1 for every $3 in income over $56,520. That continues until the month you reach full retirement age. But the earnings aren’t lost: Social Security will credit it to your record when you reach full retirement age, resulting in a higher benefit.2

4. You may be eligible for spousal benefits.

If you spent time out of the workforce, you may not meet the eligibility requirements for receiving benefits based on your lack of employment history. But if you’re married and your spouse worked, you could be eligible for spousal benefits.

Nonworking spouses can qualify for a portion of their partner’s full retirement benefit, as long as they meet certain criteria:

- The working spouse must already be receiving benefits.

- The nonworking spouse must be at least age 62.

Like traditional benefits, spousal benefits are also reduced if the nonworking spouse begins taking Social Security income before their full retirement age. The difference is that spousal benefits stop growing after the nonworking spouse reaches their full retirement age. At that time, they can receive up to 50% of their partner’s full benefit.3

5. Your spouse might be able to take over your benefits when you die.

If you’re married at the time of your death, your widow becomes eligible to take your benefits once they reach age 60. (If they’re disabled, they can take over benefits at age 50.) The surviving spouse can decide whether to keep their own benefits or take over their spouse’s Social Security benefits, based on which is higher. The benefits will be reduced if the surviving spouse hasn’t reached full retirement age.

A couple things to keep in mind: If the surviving spouse is still working, the earnings test applies. (See item 3 for more about the earnings test.) And the surviving spouse isn’t eligible for benefits if they remarry prior to age 60.4

6. You may be entitled to spousal benefits — even if you’re divorced.

Divorce doesn’t necessarily disqualify you from spousal benefits. You have to meet a few criteria to be eligible:

- The marriage lasted at least 10 years.

- You haven’t gotten remarried.

- You (and your former spouse) have reached age 62.

- You aren’t eligible for higher benefits on your own.

If you meet the above criteria, you may be eligible for 50% of your former spouse’s full benefit.5

7. You have a limited time to change your mind.

Whether you’re 62 or 70, once you’ve made the decision to start benefits, you only have one year to make changes. Social Security lets you withdraw your application for benefits one time in the 12 months after you turn them on.6 That’s why it’s so important to understand how Social Security works and what your options are before turning on Social Security as an income stream.

Final Thoughts

When is the time for you to start taking benefits? It depends. Your financial professional can help you make a decision based on your personal situation, including how much income you will need in retirement, how much you have saved and other factors that could impact your future. If you’re starting to think about Social Security, we recommend calling your financial professional for a full retirement income review.

SOURCES

1 Social Security Administration. “Starting Your Retirement Benefits Early.” https://www.ssa.gov/benefits/retirement/planner/agereduction.html. Accessed Feb. 13, 2023.

2 Social Security Administration. “Receiving Benefits While Working.” https://www.ssa.gov/benefits/retirement/planner/whileworking.html. Accessed Feb. 13, 2023.

3 Social Security Administration. “Benefits for Spouses.” https://www.ssa.gov/oact/quickcalc/spouse.html. Accessed Feb. 13, 2023.

4 Social Security Administration. “If You Are the Survivor.” https://www.ssa.gov/benefits/survivors/ifyou.html. Accessed Feb. 13, 2023.

5 Social Security Administration. “Benefits For Your Family.” https://www.ssa.gov/benefits/retirement/planner/applying7.html#h4. Accessed Feb. 13, 2023.

6 AARP. Dec. 23, 2022. “Can I stop Social Security benefits and restart them later to get a bigger payment?” https://www.aarp.org/retirement/social-security/questions-answers/social-security-going-back-to-work.html. Accessed Feb. 13, 2023.

This content is provided for informational purposes. It is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security. Individuals are encouraged to consult with a qualified professional before making any decisions about their personal situation. The information and opinions contained herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management. Neither AEWM nor the firm providing you with this report are affiliated with or endorsed by the U.S. government or any governmental agency. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IARs) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM. Information regarding the RIA offering the investment advisory services can be found at http://brokercheck.finra.org.

2/23-2734231