AE Wealth Management: Weekly Market Insights | 5/21/23 – 5/27/23

Weekly Market Commentary

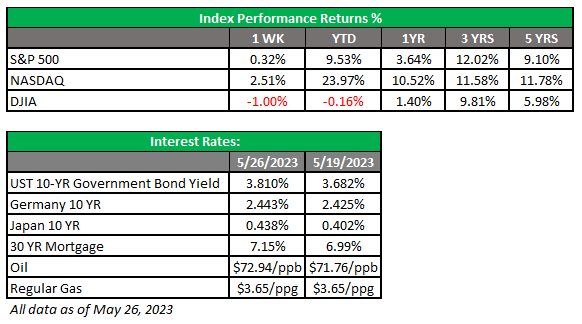

THE WEEK IN REVIEW: May 21-May 27

Take it to the limit — one more time!

“So put me on a highway

And show me a sign

And take it to the limit one more time”

Remember the Eagles song? It must feature prominently on our elected officials’ playlists, because no matter how dire the warnings, the game of brinkmanship continued last week. We keep getting closer and closer to hitting the debt limit without a workable resolution. So, what can happen? There are several scenarios that could play out here:

– A deal just under the wire. Phew! The stress will be alleviated, and we move on. There are reputational risks, but we will revert to more pedestrian discussions about the Federal Reserve and a potential recession.

– The fracas continues beyond the deadline, but an agreement is reached shortly thereafter. In this scenario, the markets will likely grow much more concerned, equities could decline and yields will most certainly rise. The government will have to prioritize who it will pay; without a debt ceiling increase, revenues will fall short of expenses. What that looks like is pure speculation, but it can run the gamut of missed or reduced salary payments to federal workers (including the military and veterans) to delaying contractors’ payments. In any case, it will increase the chances of a recession sooner rather than later.

– No deal is reached. This is the most disastrous scenario. In order for the U.S. not to default, it would have to divert dollars to service debt and interest on the money borrowed so far. When it comes to refinancing, we would have to pay even higher rates, which would make the cycle even worse. Who would suffer? Social Security and Medicare recipients and anyone paid by the government are all possibilities. This third scenario would put us into recession, while the dollar, bonds and stocks would plummet. This scenario is almost too mind-boggling to contemplate.

The parties reached a tentative deal over the weekend, so it seems scenario No. 1 is the most likely to play out. Still, the agreement must be finalized by June 5, the new date set by Treasury Secretary Janet Yellen. Taking it to the limit, indeed.

GDP improves slightly, but Fed still divided

The markets seemed enthusiastic going into the long weekend. The second reading of first-quarter gross domestic product (GDP) improved slightly from +1.1% year-over-year to +1.3% — better, but still not great. The economy feels like it’s contracting, but we aren’t officially in a recession. People are getting laid off in select industries and spending less, but job growth is still strong and spending on services (hotels and travel) continues. It’s a good-and-bad story, and that waffling adds to the overall feeling that the economy isn’t in great shape.

Perhaps this is just how things will proceed for a while. Instead of a traditional recession, we could bounce along with choppy and barely positive growth, always seemingly one catastrophe away from a disaster (like the debt ceiling debacle). Predictions are rarely accurate; the only certainty is that the economy moves through cycles. From all appearances, we are on a downward slope of a cycle right now, but whether we’re in a full-blown recession remains to be seen.

The minutes from the last Fed meeting were released last week and revealed a very divided committee regarding a potential pause in June. Some officials have said inflation and economic activity aren’t slowing enough to justify an end to rate increases. But others, including Chairman Jerome Powell, have hinted that they might prefer skipping a rate hike in June to assess the effects of their past increases and the banking sector. I think this debt ceiling mess might just seal the deal for a pause in June.

The market has been pretty stoic through it all. Yes, we sold off early last week but not in a major way. As the week ended, the markets began sensing a debt ceiling deal was near and rallied. We’re managing to stay at year-to-date highs of over 8% and haven’t dipped below 4,100 on the S&P 500 since early May. The tale here is that the markets believe we’ll get a debt deal, and the Fed will pause. Those two factors could push markets upward in June until something new to worry about arises.

Markets were closed Monday in observation of Memorial Day. We hope you took some time to reflect on the sacrifices our men and women in uniform have made for us to enjoy our freedoms.

Coming this week

- Debt ceiling talks will likely continue to dominate markets until a deal is finalized.

- On Tuesday, we’ll get the latest consumer confidence numbers. Bond auctions are also scheduled.

- Thursday will bring more bond settlements and auctions. We’ll also see the Challenger job-cuts report as well as the ADP employment report. (Last month’s reading was +296,000.)

- Finally, the Bureau of Labor Statistics will release the May nonfarm payroll numbers. The last reading was +253,000, and the Fed wants to see this number softened significantly.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

5/23-2876775-5