AE Wealth Management: Weekly Market Insights | 5/28/23 – 6/3/23

Weekly Market Commentary

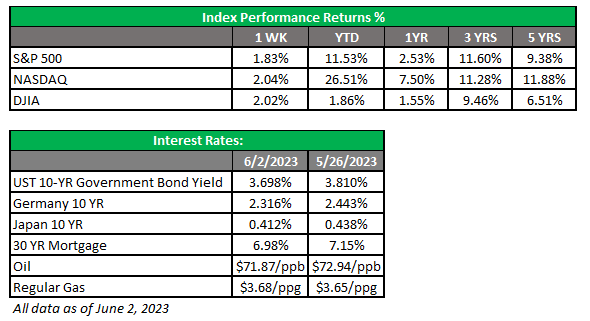

THE WEEK IN REVIEW: May 28-June 3

Done deal!

The debt ceiling drama finally ended last week with a deal that seemed to please no one. Of course, that’s the way compromise works — no one gets everything they want. The good news is we avoided a self-inflicted wound to our economy and our standing as a financial world leader. The government will fund itself through more borrowing and pretty much continue spending like it always has.

While the fallout from this mess will be minor, we still managed to look foolish trying to accomplish a basic governmental function. Our elected officials demonstrated just how divided our political system really is, and it took the threatened collapse of our economy and world economic standing to reach a last-minute deal.

In the end, it appears that we had a president who said he would not negotiate (but did) and congressional members who said they would make massive spending cuts (but did not). This exercise was nothing more than what might have been an episode of “Arrested Development,” where the family spends an hour arguing in increasingly outrageous ways about paying down their massive credit card bill only to agree to make the minimum payment and wait until the next time to address the issue.

The only thing that happened was we will not default, and the status quo was mostly retained. The Senate passed the bill after some in that chamber huffed and puffed; it was always going to happen in the House, and once the bill cleared that chamber 314-117, nothing would have stopped it. We averted one self-manufactured crisis and only two (inflation and interest rates) are left to go. At least it’s one less thing for markets to worry about.

What’s next for markets?

Now that the debt ceiling deal is done, we can focus on other factors clouding investors’ horizons. The latest data from the Labor Department showed job openings in the U.S. rose in April over March, while layoffs declined from the prior month’s levels. The Job Openings and Labor Turnover Survey (JOLTS) report showed openings rose to 10.1 million in April, up 358,000 from the prior month. More than half of this increase came from the retail sector.

Job-hopping continues to moderate, as the number of people quitting their jobs ticked down to 2.4%, just above the average in 2019. This isn’t great news for investors hoping the Federal Reserve would pause rate hikes at its upcoming meetings. The other concern there is that inflation is still hovering close to 5%, rather than the 2% the Fed would like to see.

Job creation is also creating a conundrum for the Fed. The May nonfarm payrolls report surprised to the upside yet again; we added 339,000 jobs, well above the expected +190,000. Meanwhile, ADP reported 278,000 new private jobs versus a consensus estimate of 180,000.

ADP’s chief economist, Nela Richardson, stated, “This is the second month we’ve seen a full percentage-point decline in pay growth for job changers. Pay growth is slowing substantially, and wage-driven inflation may be less of a concern for the economy despite robust hiring.”

Maybe that’s the sweet spot for the Fed — people working but earning and spending less due to higher prices. That may work to get the Fed to pause in the short term but would also mean it will take much longer for inflation to come down. Will the Fed have the patience to wait it out? Probably, but politicians in an election year will not. Plus, markets will begin punishing companies that cannot grow earnings because people are buying less due to lower wages and higher prices.

Despite all this conjecture about the Fed’s reaction to the employment numbers, the market climbed on Friday after the Senate approved the debt ceiling deal and sent it to the president. Strong job growth did little to stop the euphoria that had been pent up over the past few anxious weeks. With the government’s fiscal mess behind us for a couple of years, the market’s attention will now turn to the Fed. Current expectations are that the Fed will pause rate hikes at next week’s meeting and assess current rates’ impact on the economy. That will bring the usual angst about when we can expect to see cuts from the Fed and how severe a recession may be — if it comes at all.

Coming this week

- Now that the debt ceiling is lifted, a slew of bills and notes will settle and be auctioned this week. It will be interesting to see how those auctions are received.

- This week will be pretty quiet from a data standpoint. Factory orders (Monday), mortgage applications and consumer credit (Wednesday) and the Fed balance sheet (Thursday) are pretty meager data points.

- Markets will be looking at recent data this week, now that the debt ceiling negotiations are no longer flooding the economic news. Markets will refocus on what the Fed will be doing at its next meeting, especially after last week’s unemployment number.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

6/23-2937057-1