AE Wealth Management: Weekly Market Insights | 9/25/22 – 10/1/22

Weekly Market Commentary

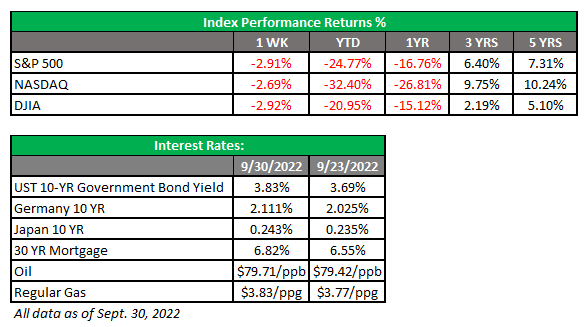

THE WEEK IN REVIEW: Sept. 25 – Oct. 1

Bank of England pivot sends shudders through a fragile market

Markets kept sliding downward last week, as Hurricane Ian battered Florida and the Nord Stream pipelines sprung leaks. The human and economic impact from the hurricane on Florida will be significant, but we don’t know the full effects. Suffice it to say that it will take a while for the state to recover.

The Nord Stream mess is another negative story that filled the news. (For those who don’t know, the Nord Stream pipeline is used to ferry gas between Europe and Russia. A series of explosions hit the pipeline last week.) The conversation about who is responsible for the explosions has dwarfed the discussion about the potential environmental impact. The upside was that Russia had already shut off gas shipments to Western Europe in response to sanctions, so the immediate effects were negligible. The remaining gas is leaking into the ocean, which is a bad thing, but it’s difficult to understand how the Russians are responsible. All they have to do is turn on or shut off the spigot on their end. Why go to the trouble of blowing up your own pipeline? Hopefully, we will get an answer soon as to how this happened and who is responsible, but the longer-term impact is that if the conflict in Ukraine ends soon, the pipelines will not be available to deliver energy to Western Europe. That will make bringing industries back online that much slower and hamper the recovery in Europe, especially in Germany.

The other major development last week: Bank of England (BOE) announced it would suspend its quantitative tightening scheme (rate hiking) to support the falling pound. On the surface, the explanation didn’t make sense. Why signal that you aren’t going to raise rates further when you are already behind the U.S., and the higher rates in the U.S. are driving foreign asset flows in the U.S., which strengthens the dollar at the expense of the pound and other local currencies? Why would you buy a British bond (called a gilt) if you can get a better yield in the U.S.? The BOE official bank rate is currently 2.25%; this is their version of our fed funds rate, which is currently 3%. The U.S. equity markets took the BOE’s actions as a sign that our Federal Reserve would consider a similar move and stop raising rates sooner than current expectations, which isn’t until 2024. As a result, last Wednesday was our best day in the markets since July.

What a difference a day made. On Thursday, it was brought to light that British pension funds had expressed distress that their bond holdings would be severely devalued if the BOE continued to tighten. This information made much more sense. As you can imagine, the same old concerns of a global economic slowdown returned, and markets reversed their gains from the day before. Initial unemployment numbers were the final nail in the coffin, as they once again failed to deliver the higher jobless claims that would show our Fed’s rate increases are having the desired effect of cooling the red-hot jobs market.

All these negatives have been hanging over the market, leaving it in a sour mood. There has been no sign that inflation is declining and no indication the Fed will take its foot off the brakes. The market got a little hopeful on Wednesday, but that quickly evaporated on Thursday. Markets ended a miserable month and quarter on a violent note. Selling accelerated into the final hour of trading on Friday, with the S&P 500 ending the month down over 9%.

Shine comes off the Apple

Apple was downgraded by Bank of America last week, a rare move given that Apple has always been the go-to for investors as a company that can do no wrong. Apple has long been viewed as an aristocrat among stocks. This may be the last shoe to drop for this market downturn; after Apple gets hammered, what else will be left?

To be fair, Apple has been smacked around pricewise, dropping significantly from $180 to $140. Yet a lot of that was trading and news that chipped away from the periphery. This time, Apple has said it is paring back producing for its new Apple iPhone 14 after failing to see as high demand as anticipated. This is monumental. Each new iPhone for over a decade has been greeted with immense excitement, with people sleeping outside of stores to be the first to get the newest model and paying increasingly higher prices for models that offered few new breakthroughs. In fact, the most innovative move was back when the iPhone 6 was introduced with a bigger screen after Samsung had wiped the floor with the iPhone 4. Modest improvements were made, and gadgets were added, but in the end, there was always yet another more expensive version of the same old phone. The only notable changes were more camera lenses and new shell colors. It seems people are sick of paying close to $1,000 for something that may be obsolete in a year. Since Apple is the largest S&P 500 member by market cap, maybe this is a sign we’re close to bottom with this market.

Coming this week

- Jobs will take center stage this week. This is even more important given that it will be an indicator to see if the Fed rate hikes are having the desired effect on slowing job growth.

- We will get to see the Job Openings and Labor Turnover Survey (JOLTS) reading on Tuesday. This number is backward-looking for August, so it will be a bit stale. The July reading was 11.24 million, and expectations are that August will drop to 10.45 million. If we don’t see a decline, markets will most likely react negatively even though it’s an old number.

- On Wednesday, the ADP jobs report will be released, the first one using its revamped methodology. The last report came in at 132,000 new jobs, while the nonfarm payrolls were at 315,000. This data point may slide into irrelevance unless we begin seeing some alignment with the government’s figures. Until that happens, it won’t be of much interest as a predictor.

- Wednesday will be a busy one for data. We’ll also see mortgage applications plus oil and gas inventories.

- Finally, on Friday, we’ll get the September jobs reading from the Bureau of Labor Statistics (BLS). Expectations are for more than 275,000 new jobs, with the unemployment rate staying at 3.7%.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

10/22 – 2454690-1