AE Wealth Management: Weekly Market Insights | 10/22/23 – 10/28/23

Weekly Market Commentary

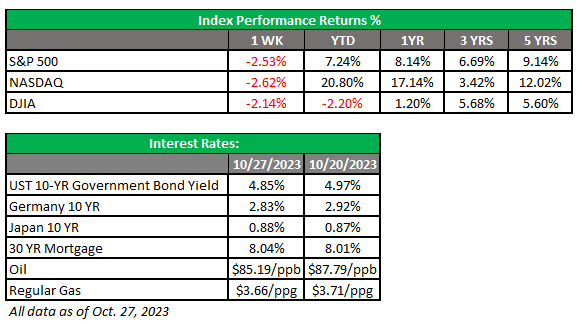

THE WEEK IN REVIEW: Oct. 22-28, 2023

Q3 GDP comes in hot — but will it stay that way?

Experts were saying that third-quarter gross domestic product (GDP) would be strong — but just how strong was a surprise, coming in at an eye-popping 4.9%! Where did all this growth come from, and will it continue? Third-quarter GDP growth came mostly from personal consumption (individuals buying things), inventories and government purchases. Other components of GDP were little changed.

Personal consumption growth shouldn’t surprise anyone. In fact, personal consumption expenditures (PCE) is a key inflation metric for the Federal Reserve. PCE didn’t drop from last month’s levels, which tells us inflation is stubbornly hanging around. If you’ve been on an airplane or in a hotel or restaurant this year, it’s obvious people are spending. But savings are diminishing, credit card bills are piling up and interest rates to service debt have risen to levels not seen in over 30 years. Everything also costs more, so you have to spend more to “consume” the same amount. Plus, student loan repayments have resumed, so people have less money to spend.

The argument that all the pent-up demand from the pandemic is driving this growth is getting long in the tooth. At some point, we either will be exhausted from spending or run out of money. This pace of travel and leisure cannot be sustained.

The next item — that inventories contributed to higher-than-expected GDP growth — makes sense: People are spending more, so businesses are stocking up! When people stop spending, businesses will be stuck with inventory. Then they won’t order or make more until they sell what they have. This also isn’t sustainable for the same reasons that the pace of consumer spending can’t go on forever.

This brings me to the final contributor of recent GDP growth: government spending. I’m not going to catalog how much is being spent, who is receiving the money or what it’s earmarked for. What I will say is that government spending is also unsustainable at its current levels. We owe over $33 trillion overall and are running a $2 trillion annual deficit. There will be increased pressure to cut government spending and reduce our debt. To sum up, we saw a big number for third-quarter GDP — but we cannot keep this up, and the economy may be headed for some trouble.

Markets tense as world awaits what happens next in Middle East

Three weeks after the Hamas terrorist attacks on Israel, the Israeli Defense Force (IDF) has been holding back on a full-scale ground invasion in Gaza. The world is waiting to see how long they wait and how far the conflict will spread if the IDF moves.

It’s highly likely that Hezbollah will attack in some form from Lebanon, which is already happening with rocket fire and border skirmishes. The markets would not consider active engagement with Hezbollah a prelude to an expansion of the conflict, but it doesn’t seem like the markets are pricing in anything more than a ground invasion of Gaza by the IDF and increased aggression from Lebanon by Hezbollah. Frankly, that is enough and has been weighing on the stock market for the past few weeks.

But all bets are off if Iran or other Middle Eastern nations join the attack on Israel and the U.S. is drawn into direct involvement in the region. Oil prices will spike from already high current levels, and Western economies (despite our recent GDP reading) could drop into recession.

For now, markets are worried about the situation in the Middle East, and we have given up over 400 points on the S&P 500 since July. We made runs to the July highs at the end of August and in early October but fell short both times.

It’s important to note that the conflict in and around Israel isn’t the only concern for markets, which were still smarting from higher rates and wondering if (or when) a recession would begin and the Fed would potentially reverse course. The most recent events in Israel can accelerate things rapidly if they spread beyond the region, and it doesn’t appear that markets have priced in that possibility.

Coming this week

- Markets will be focused on the Fed meeting (Tuesday and Wednesday) and the most recent jobs picture this week.

- The action will begin on Tuesday with the Fed meeting. Current expectations are for the Fed to remain on pause, keeping the federal funds rate where it is.

- Tuesday will also include a sizable bond auction, along with the latest Consumer Confidence Index, Case-Shiller Home Price Index, Federal Housing Finance Agency (FHFA) House Price Index and Chicago Producer Manufacturing Index (PMI) numbers.

- On Wednesday, we’ll see the Job Openings and Labor Turnover Summary (JOLTS) report for September, plus the ADP employment report. JOLTS was at 9.6 million open jobs last month, a decline from over 11 million earlier in the year. The ADP was at 89,000 last month. We need to see JOLTS drop further and the ADP to remain at these levels for the Fed to stay put.

- Weekly unemployment claims, the Challenger job-cuts report, productivity and factory orders will also come out on Wednesday.

- Finally, the Bureau of Labor Statistics nonfarm payrolls reading will come out on Friday. We added 336,000 jobs last month, which was not aligned at all with the slowdown in the ADP. This could be a pivotal number: If ADP was right last month and the government’s job number was off, we could see a significant decline in jobs and wages.

- Earnings season is chugging along, with 17% of the S&P 500 reporting as of Oct. 20. So far, the majority of those reporting have had positive earnings per share (EPS) and positive revenue surprises.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

10/23-3143466-5