AE Wealth Management: Weekly Market Insights | 10/30/22 – 11/5/22

Weekly Market Commentary

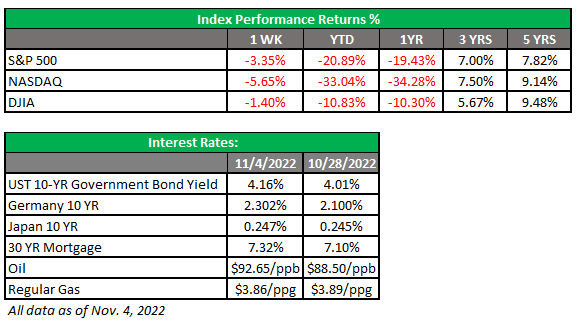

THE WEEK IN REVIEW: Oct. 30 – Nov. 5

Fed raises rates as Powell disappoints markets (again)

The Federal Reserve met last week and raised the federal funds rate another 75 basis points (0.75%) to a range of 3.75%-4.00%. This really wasn’t a surprise; the markets pretty much expected the fourth consecutive increase of 75 basis points. (It’s the sixth move upward in 2022.)

The anticipation going into the recent meeting centered on what kind of guidance the Fed would give as to the size of future rate hikes, when such increases would potentially stop and how long the Fed would leave higher rates in place. Markets once more rallied into the Fed’s announcement, hoping we were close to the end on rate hikes.

In its announcement, the Fed seemed willing to consider the cumulative effect of its rate increases and the potential impact they may have on the economy and inflation, instead of waiting for the actual rear-looking numbers to catch up and confirm what has already happened. In essence, the Fed signaled it has shifted from a data-dependent stance to a forecasting mindset, which seems like a pragmatic and logical approach given the rapidity of this year’s increases.

The market was fine with the shift and actually rallied shortly after the release of the announcement, perceiving a softening in the Fed’s approach. The decision was unanimous — so all good, right?

Not so fast. The market didn’t get the pivot it was looking for when Federal Reserve Chairman Jerome Powell stepped up to the podium. He basically went completely counter to the dovishness of the initial announcement, saying that the Fed was not done with its work, there’s still a “long way to go,” and that the Fed is committed to get this done. He also said rates need to be higher and that it would be premature to consider a pause. The market reversed its upward course following Powell’s comments. We had a pretty ugly ending Wednesday and didn’t regain our balance until Friday’s job number came out (more below).

So, which is it? Will we wait and see what the hikes have done (or are doing), or is the Fed sticking to its rate-hiking cadence to move the federal funds rate past 5% before stopping? Was this all jawboning and browbeating and the Fed will signal a pause after its December meeting?

In our view, the Fed will not fix the inflation issue without driving us into a recession. The Fed has already challenged the real estate market and will likely challenge a couple more industries, but inflation will only come down when consumers throw in the towel. Any more Fed activity beyond 4% will likely make the recession deeper, and it will take us longer to climb out.

By December, we could see abundant evidence that the economy is slowing significantly. It seems Powell continues to misread what’s happening because of his reliance on backward-looking data. Once this data confirms what he has been looking for, we may have gone too far and it will be a tough road back.

Jobs just won’t quit

The Bureau of Labor Statistics (BLS) released its October jobs report last week. We added 261,000 jobs last month, more than the expected +210,000. This was almost identical to September’s reading of +263,000, although October’s reading was the lowest monthly job growth since December 2020. The reading was well above the upper range of expectations, yet the unemployment number ticked up from 3.5% to 3.7% mostly on a decline in the labor participation rate. Earlier in the week, ADP also posted a solid increase of 239,000 private-sector jobs.

It’s an example of the recent trend of bad news being good; the market chose to focus on the increase in the unemployment rate — the one bad item in an otherwise strong jobs report — as a reason to head higher. Rising unemployment plus a lower inflation rate are the two things the Fed is looking for before it considers stopping interest rate increases.

After getting its teeth kicked after Chairman Powell’s remarks on Wednesday, the market had a nice rebound on Friday on the belief that we are on the road to satisfying one of the Fed’s requirements. It’s surprising that the jobs market hasn’t softened as much as expected given current market conditions. To paraphrase Ernest Hemingway, there are generally two ways to go bankrupt: first gradually, then suddenly. The concern is that the employment situation will gradually decline before suddenly dropping, and the Fed will miss the trend.

Coming this week

- Earnings season is winding down. As far as the markets are concerned, earnings were dwarfed by the Fed announcement last week.

- Tuesday is Election Day! Republicans are projected to win both the House and the Senate. If they do, we will return to divided government and gridlock, which the markets love.

- The consumer price index (CPI) for October will be out on Thursday. September’s reading was 8.2% year-over-year. This will be the first opportunity to see if rate hikes are taking hold.

- Consumer sentiment will also be reported on Friday.

- We’ll also hear from several Fed officials this week. After Chairman Powell’s comments regarding the level and pace of future interest rate increases sent markets lower last week, it will be interesting to see just how many other Fed officials feel the same way. If they close ranks and reiterate Powell’s comments, the markets could get gloomy until we start seeing concrete improvement in inflation or the unemployment number continues to climb. If we see a decline in the CPI, markets could moderate and some enthusiasm may return, especially after the elections.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

11/22-2578521-1