AE Wealth Management: Weekly Market Insights | 11/5/23 – 11/11/23

Weekly Market Commentary

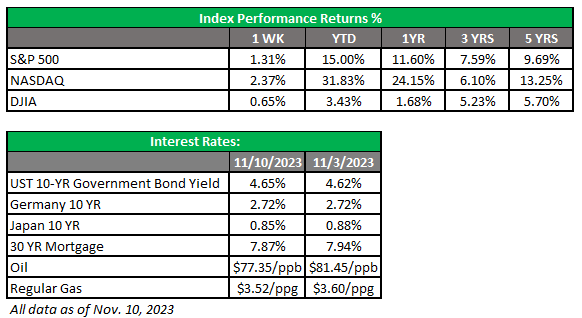

THE WEEK IN REVIEW: Nov. 5-11, 2023

Markets stall after hawkish comments from Fed officials

After last week’s decision to keep interest rates where they are, markets took a breath and focused on comments from Federal Reserve officials this week. First, Michelle Bowman said she expects further tightening will be needed, causing markets to initially tumble before rebounding.

Maybe markets should have taken Bowman’s comments more seriously because, on Thursday, Chairman Jerome Powell stepped up to the mic and got all Eeyore on us. This is the same guy who said the week before that the Fed was waiting to see what the data would say. He didn’t see any new data in the days between comments, but last week, he said monetary policy is in “restrictive territory” and the Fed would not be misled by “a few months of good data.” Wonder what he would say if we had a few months of really bad data.

Markets freaked out after his comments shattered the fragile narrative that the Fed was done, and we could start looking for signs of decreasing rates. The markets likely overreacted; the sell-off on Thursday would have been a little more earnest if we had some data to make us think more interest rate hikes were on the way.

One of two things is happening here. Maybe Powell knows the inflation numbers coming out this week and they will be bad or, at a minimum, static. It wouldn’t be surprising to see the Consumer Price Index (CPI) remain elevated, especially since gas has been going down but other prices are still high. There may not be marked improvement in CPI, which might only dip to 3.5% year-over-year.

Or maybe Powell doesn’t want markets to think the Fed is done, so he talks hawkish. This gets the bond yields to go up and stocks to sell off. It’s an old trick of saying “whatever it takes” without doing anything. The problem for Powell is if the Fed raises rates, it will most likely push us into recession. Then the weak numbers the Fed wants to see will signal a contracting economy, and we will have to reverse course. Inflation will eventually slow to 2%, but only if we have a recession, which all the politicians running for reelection don’t want. Expect this push-and-pull for the rest of 2023.

Time in the market is what matters

Attention market-timers: If you need yet another reminder of why trying to time the market is a no-win situation, you just need to look at 2023 so far. As of Nov. 8, the S&P 500 was up 14% year-to-date. However, most of the gains can be attributed to only eight days. Who is confident enough in their “skill” to have predicted which eight days you would need to be in the markets to capture these gains?

It’s similar to how a narrow set of securities accounted for the lion’s share of returns recently. Would any “timers” have been wise enough to select the seven securities ahead of time while living with the corresponding volatility?

The truth is, timing the markets and concentrating on individual securities is not a good game. The S&P 500 has posted a positive return nearly 75% of the time, and that’s a lot less stress and hand-wringing. Have you ever seen a coach who wins three out of four games get fired? Or a baseball player whose batting average is .750 not get into the Hall of Fame? (Spoiler alert: There has never been a Hall of Fame member with a batting average higher than Ty Cobb’s .366.) You get the point: Time in the markets — and not timing the markets — is usually an effective approach to working toward consistent results for investors trying to reach their goals.

Coming this week

- Now that the Fed has left rates alone and the jobs data has confirmed the economy is slowing and the smoking-hot gross domestic product (GDP) print from the prior week isn’t looking like the scary impetus for more rate hikes, it’s time to hear from regional Fed presidents. Jeffrey Schmid (Kansas City), John Williams (New York) and Lorie Logan (Dallas) will speak on Tuesday. On Wednesday, we’ll hear from Williams again. Then Raphael Bostic (Atlanta), Thomas Barkin (Richmond) and Kathleen O’Neill Paese (St. Louis) will provide comments on Thursday. Finally, Logan and Bostic will speak again on Friday.

- Why all the attention on the Fed speakers? With Powell basically telling us we’ll see how things go, it’s really important to listen to these Fed officials’ views on the direction of interest rates. Markets will be paying attention.

- Other areas of interest will include the consumer credit readout late Tuesday, especially as people are struggling with high credit balances and rates. We’ll also see MBA mortgage applications and wholesale inventories (Wednesday), the Fed balance sheet (Thursday) and consumer sentiment (Friday).

- Earnings will continue this week. Nearly half of the companies had reported by Oct. 27, with the majority reporting positive earnings per share.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

11/23-3214123