AE Wealth Management: Weekly Market Insights | 11/12/23 – 11/18/23

Weekly Market Commentary

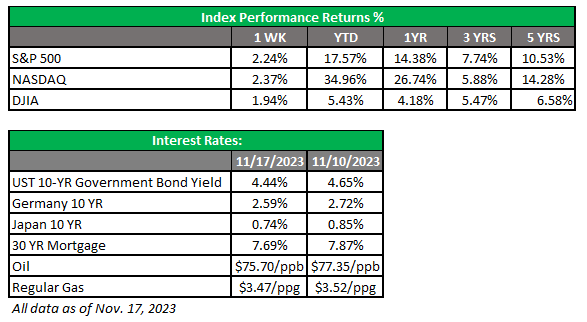

THE WEEK IN REVIEW: Nov. 12-18, 2023

Markets rally as interest rates dip and chances of additional hikes recede

Markets continued to climb back toward end-of-July highs last week. After the Federal Reserve’s last meeting and a softer jobs number indicated a slowing economy, markets began to look for additional confirmation of easing inflation. That arrived with a flourish last week (more in the next section) and all but sealed the end of additional interest rate hikes.

The 5-year U.S. Treasury, which was yielding above 5% less than a month ago, has tumbled to 4.4% and continues to have pressure on the downside. But stocks — especially tech stocks — have soared since the Fed meeting. As the 5-year treasury yield topped 5%, the S&P 500 was around the 4,100 level, well off its mid-year high of 4,588. Since the Fed meeting, the S&P 500 has bounced 400 points as we head into the crucial holiday season and year-end.

The past few weeks were a lot less about what went right than what did not go wrong or go worse. First, we had the Hamas attacks and inevitable response from Israel. People were on pins and needles with concerns the conflict could spread and evolve into a wider regional (and possibly global) conflict. Thankfully, that hasn’t happened and appears less likely with each passing day. From the market’s standpoint, an expansion of the conflict would have had an immediate impact on the price of oil and a ripple effect on economies all over the world. The 5-year yield rose, and stocks swooned with fear and uncertainty as we waited to see if the conflict would spread in the Middle East.

Then, there was the stronger third-quarter gross domestic product (GDP) print showing we were growing at an unsustainable 4.9% rate, which appeared to signal the Fed had room to raise rates even higher. The Fed’s actions so far had not shown a meaningful impact on curtailing job and wage growth, as both remained stubbornly strong. Inflation, although much improved from this time last year, had also begun to tick upward and was feeling like it would stick at about 3-3.5%.

The Fed was being dodgy at its last meeting, saying it would keep its options open. They also dangled another rate increase in the future just to keep us honest. But the markets didn’t fall for the ruse and seem convinced the Fed is done.

The lack of expansion in the Middle East conflict, stable and lower oil prices, a weak jobs number, the Fed’s non-committal comments, and inflation data last week have combined to send us off to the races. Enjoy the ride for the moment; markets are seldom tranquil and satisfied and will always need to fret about something. These past few weeks have been quiet in a good way, but it won’t be long before markets replace their worry with something else. Let’s hope they take a break from worrying, at least until after the holidays.

Inflation continues to moderate

The latest consumer price index (CPI) and producer price index (PPI) numbers confirmed slower inflation last week. We still aren’t back to levels the Fed would like to see, and all this is measuring is price increases. We will not see prices come down unless we see a deflationary environment, which is unlikely. Some commodities will go up and down, but more often than not, once manufacturers or service providers raise prices, they are unlikely to lower them.

This most recent cooling of the inflation rate is due to two things: gas prices, which are more prone to volatility, and shelter costs, which aren’t subject to as dramatic swings and don’t come down as quickly as gas. Strip out energy, and goods prices were unchanged on the month.

Shelter costs have played a large role in the decline in core inflation. Zillow data shows inflation in the prices of newly signed leases peaked earlier this year and has come down more quickly than the Labor Department’s rent measure. Rent and housing prices are a lot harder to bring down than volatile gas prices, but this is still good news.

The most recent decline in inflation is more of a result of the cratering of gas prices, which reflects slowing global demand for oil (and a lack of a spike in crude prices in the face of the Israeli-Hamas conflict) as a result of slowing economic activity. We could just as easily be above $4 per gallon if the conflict spilled over and impacted oil production — like what happened when Russia invaded Ukraine.

It’s good news that energy prices are down, but that can quickly shift if we have another oil spike. Services prices were unchanged in October, as higher costs for transportation and warehousing were tempered by a decline in margins received by wholesalers. We know producers will pass on costs to consumers if they are able, and prices tend to go up a lot quicker, drift down slowly and never seem to get back to prior levels. Leases and houses might have peaked, but they sure aren’t going back to where they were. But this all might just be enough for the Fed right now.

Coming this week

- It’s hard to believe that Thanksgiving 2023 is already here. Markets will be closed all day on Thursday and close early on Black Friday (stocks at noon Central and bonds at 1 p.m. Central).

- The most significant data news this week will be the release of the minutes from the most recent Fed meeting (Oct. 31-Nov. 1). Traders will parse the notes for an indication of just how hawkish the Fed continues to be. Bear in mind that these minutes will not have had the benefit of knowing the most recent jobs and inflation figures.

- MBA mortgage applications will be released on Wednesday. We’ll also see unemployment claims, and they may be wonky since they usually come out on Thursday. Things will slow dramatically throughout the week and will probably be quiet as everyone enjoys the long Thanksgiving weekend.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

11/23-3214123-3