AE Wealth Management: Weekly Market Insights | 5/19/24 – 5/25/24

Weekly Market Commentary

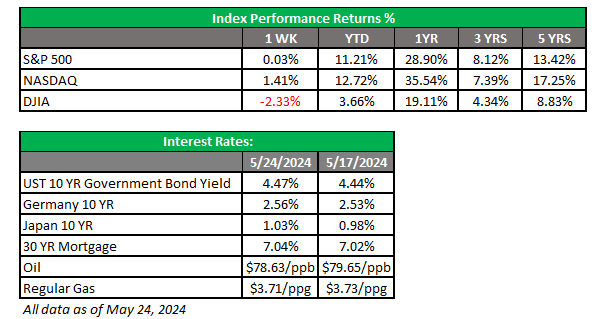

THE WEEK IN REVIEW: May 19-25, 2024

Sizing things up

The week started slowly, as expected, with markets mulling over the inflation data from the previous week and letting off a bit of steam as we recorded new all-time highs. Things picked up on Wednesday following the release of the Federal Reserve’s latest meeting minutes and anticipation of earnings from NVIDIA, the darling of the AI boom.

But not even blowout earnings from NVIDIA could stem the bleeding last Thursday, as we had the worst day for the Dow so far this year. The culprits? Lower-than-expected unemployment claims and a stronger-than-expected manufacturing reading. Both data points signaled that the jobs market is still robust and the economy may not be getting weaker as expected.

The situation was made worse by the Fed minutes, which showed some of the voting members were open to keeping rates higher for longer and possibly open to further hikes. All of this was enough to send markets spiraling downward. The jobs and manufacturing readings pointed to inflation continuing to be sticky with no concrete signs of approaching the 2% level the Fed would like to see. The talk is that we may even see an uptick before inflation falls further; if we do, it would put any rate cuts in July out of reach unless we see inflation drop further.

Markets modestly recouped some of their losses on Friday before we limped into the long weekend. It is also important to note that the Friday before a long weekend is notoriously plagued by lower volumes as traders generally take the day off. I would not say we are out of the woods until we see two or three solid sessions of gains, but with Personal Consumption Expenditures (PCE) data this week, we may have another bout of volatility. The 10-year Treasury is stubbornly clinging to the 4.5% yield level, and until it starts marching steadily downward. the markets will be nervous.

The Feds’ own Greek epic

Remember Homer’s Ulysses (aka Odysseus)? At one point in his journey, he and his crew had to sail through the Strait of Messina near current-day Calabria, Italy, to get home. In Greek mythology, that would involve running a gauntlet. On one side of the straight was Scylla, a six-headed monster that eats men passing on ships. On the other is Charybdis, a giant whirlpool that destroys everything in her reach three times per day.

Let’s apply that dilemma to Fed Chair Jerome Powell and the Fed’s current situation. On one side, Powell has proven to be a little less independent than we would like. He seems very open to cutting rates to help spur the economy, which might be helpful to incumbents in the upcoming elections but would also increase inflation. However, this approach could mean less of the crew would get eaten by Scylla. On the other side, if the Fed keeps rates higher for longer or even raises them more to tame inflation, it might send the entire economy into recession. That would be the Charybdis option.

How did Ulysses handle it? He sacrificed six of his crew to Scylla but saved the rest and his ship by avoiding Charybdis so they could continue on their journey home. If this situation sounds familiar to you, in today’s colloquialism we would say Powell is “between a rock and a hard place.” Cutting rates too soon may help the political fortunes of some, but cutting too soon will also keep inflation higher and hurt many in the long run. But keeping rates too high might suck everyone down into the whirlpool of recession. The entire economy and the whole country, politicians included, would suffer.

That’s where Powell and the Fed find themselves. Will they sacrifice a few in the near term for the good of the many longer term? We have heard that Powell needs to channel his inner Paul Volcker, who famously tamed inflation back in the late ’70s and early ’80s. I would argue he may need to channel a little of his inner Ulysses this time around as well.

Coming this week

- The short trading week will feature some meaningful data for markets. We’ll see consumer confidence on Tuesday and MBA mortgage applications on Wednesday. Wednesday will also include the Fed’s Beige Book, a speech from New York Fed President John Williams.

- On Thursday, we’ll see the first revision of first-quarter gross domestic product (GDP), unemployment claims and pending home sales.

- Friday will be eventful as we get the personal income and spending plus April PCE and Core PCE. These are two of the Fed’s preferred inflation readings and could be significant market-movers as we end the week.

- Earnings are pretty much done, with 93% of S&P 500 companies reporting as of May 17. The blended (year-over-year) earnings growth rate for the first quarter is 5.7%, which marks the highest earnings growth rate reported by the index since the second quarter of 2022.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

5/24-3559928-4