AE Wealth Management: Weekly Market Insights | 6/25/23 – 7/1/23

Weekly Market Commentary

THE WEEK IN REVIEW: June 25 – July 1, 2023

Fed chairman keeps sights set on potential rate increases

Federal Reserve Chairman Jerome Powell doubled down on talk of additional, consecutive interest rate increases in the coming months — forecasting a potential half-percentage-point increase through the end of 2023 as the Fed had implied at its June meeting. At a meeting of central bankers from across the globe in Sintra, Portugal, last week, Powell said, “Policy hasn’t been restrictive enough for long enough.”

Aside from its break in June, the Federal Reserve has increased interest rates at each of its meetings since March 2022, including four straight 0.75% increases. “I wouldn’t take moving at consecutive meetings off the table at all,” Powell said during a question-and-answer session.

The market seems to have priced in two additional hikes for the rest of the year, so there really is nothing concerning at the moment. If markets are hanging in at these levels with two more potential rate increases on the horizon, then any surprise from the Fed — say, a smaller interest rate increase — could likely ignite a furious rally.

Another scenario is also possible.

The economy isn’t slowing as much as previously expected; the first-quarter GDP reading was revised from an initial 1.1% and a second estimate of 1.3% to a final reading last week of 2%. That 0.7-percentage-point increase seems like an absurdly wide range for a revised GDP number, where we typically see a revision of plus or minus one- or two-tenths of a percentage point. Consumer spending growth accelerated to the strongest levels in nearly two years despite stubbornly high inflation. Spending on durable goods surged 16.3% and services rose 3.2%.

While our economy growing by an annualized 2% is good news compared to the second estimate of 1.3%, that could be the catalyst for the Fed to feel it has more runway in its attempt to engineer a soft landing. Another factor the Fed is likely considering in favor of continuing rate increases is the results of recent bank stress tests, which showed large U.S. banks were in good shape to weather a potential economic downturn. Banking sector health in the face of higher interest rates had spooked the Fed, especially after Silicon Valley Bank, Signature Bank and First Republic Bank collapsed in recent months. These stress test results may soothe some nerves and stiffen the Fed’s resolve.

At the moment, the Fed is saying it has more to do in its fight with inflation — and it clearly does — but getting to the desired 2% target for inflation will be more difficult, and the risks of pressing too hard will be elevated. There may be a longer runway to engineer a soft landing, but who cares how long the runway is if the Fed is nowhere near an airport at the moment?

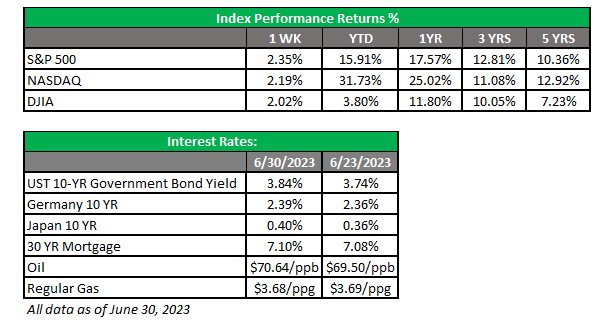

Markets end first half of year on a winning streak

We had a lot thrown at us in the first half of 2023. After a miserable year, markets picked themselves up from the lows of October 2022 to advance over 20% as measured by the S&P 500. Year to date, the S&P 500 is up just over 15%. The Fed’s continued rate increases, inflation has come down but remains sticky, constant imminent recessionary fears, regional bank failures and the debt ceiling fight were all hurdles the markets had to negotiate in the first half of the year.

The markets and the economy both seem to have hung in there despite the Fed’s determination to slow job growth and curb inflation as it tries to avoid recession. Sure, the growth has been uneven with only a narrow portion of the market accounting for a lot of the gains — the Nasdaq 100 had its best opening six months ever. The rest of the market has only recently begun to move upward. That is still progress, and with all the challenges of the first half of the year behind us, it’s hard to imagine a more difficult second half. There are bound to be “developments” and “challenges,” but this solid start to the year — despite all the potential negativity — will hopefully spark the follow-through for a strong ending to the rest of 2023.

Coming This Week

- With Independence Day falling on Tuesday, markets will open for an abbreviated session Monday, July 3 — equities close at 1 p.m.; bonds at 2 p.m. — and reopen for normal operation Wednesday, July 5. Trading volume will likely be light.

- Data is light Monday, too, with only the manufacturing PMI final reading and the manufacturing ISM index.

- The big news Wednesday will be the release of the minutes from the Fed’s June meeting. After all the breadcrumbs Powell has dropped hinting at another two 25-basis-point rate hikes this year, it will be of great interest how many other Fed members are on board with that plan. Mortgage applications and car sales will also be reported Wednesday.

- Thursday we will see JOLTS data for May and the ADP national employment report.

- June jobs numbers will close us out on Friday. Job growth continues to be strong despite the Fed’s attempt to slow it to curb inflation. Wage growth, however, has been stagnant.

Have a safe and happy Fourth of July!

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

7/23-2982871-1