AE Wealth Management: Weekly Market Insights | 8/11/24-8/17/24

Weekly Market Commentary

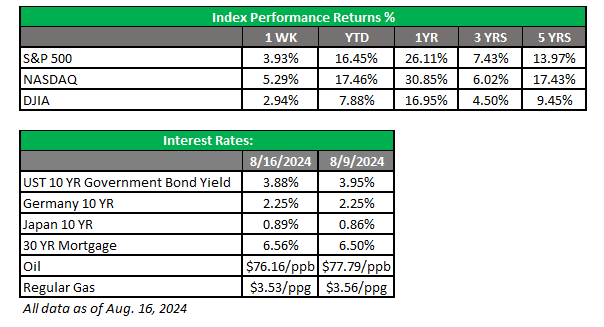

THE WEEK IN REVIEW: Aug. 11-17, 2024

Not enough just yet

The Producer Price Index (PPI) and Consumer Price Index (CPI) readings for July were reported last week. Both showed that inflation is declining but is inching downward in an almost painfully slow manner.

The decline from 3.0% to 2.9% in CPI year-over-year is an important psychological threshold, just like the unemployment number rising above 4% was important and signaled we had crossed a line that should cause concern. An inflation print below 3% is significant. The problem is it was only down 0.1%, which is not materially different from 3.0% or 3.1% and will not prompt the Fed to cut more aggressively than the 25 basis points (0.25%) markets have priced in for the September meeting.

We still believe that a deteriorating jobs market is the thing that will cause the Fed to accelerate its rate-cutting schedule. The major issue is that if we continue to see jobs unravel at the pace we’ve been seeing over the past five months, we will likely be sliding into recession, and inflation will take care of itself via a decline in spending as a result of people being unemployed.

We have been saying for months that the Fed risks driving us into a recession if it remains focused on driving inflation to 2%. The challenge is that the Fed has a problem juggling just one ball (inflation or price stability), let alone two balls (inflation and jobs). Trying to thread the needle of mitigating job losses and lowering inflation seems like a Sisyphean task; if you fix one thing, you immediately need to start paying attention to the other.

It would probably be more beneficial for the Fed to work on stabilizing prices (which it can control to some extent through its open market activities) and allow the rest of the economy to create or eliminate jobs. For now, inflation is below 3%, July sales are still fairly healthy and unemployment isn’t out of control. It all adds up to a Fed that isn’t willing to move boldly on interest rates and risks being sidelined as events move faster than they can react.

Market stages a quick comeback

There was a lot of handwringing and worry a couple of weeks ago, with people screaming for an emergency 50-basis-point (0.50%) rate cut between Fed meetings. But after a very quiet first half and a pretty strong summer, the market, like a sleeping dog caught unaware, decided collectively to let off some steam.

This sort of market action isn’t unusual, but it seems the violence and the speed of the sell-off on the back of a sleepy and undramatic first half was what threw people off. All of a sudden, we had volatility where we had none before, and there was uncertainty and fear. Fast-forward just one week: We not only made back most of our losses but are once more closing in on record highs, and volatility is back to levels prior to all the mayhem. In fact, we had the best week of the year so far.

What happened? After the soft weekly unemployment claims sparked a rally the week prior, the data last week confirmed inflation was continuing to decline, consumer spending was still healthy and nothing new by way of an escalating conflict in the Middle East had occurred. Volatility dropped and all seems right again. But is it? Sure, it made a Fed cut in September more certain. But the numbers also ensured we would see a miniscule cut and that higher rates (albeit 0.25% lower) would still be with us.

The same factors that drove markets the past two weeks are present. The economy is weaker, and many people already “feel” we are in recession or it’s just a question of time before we slip into one. There doesn’t seem to be any progress in the Middle East, and anything that happens will probably be bad rather than good. Plus, we’re headed into what could be the strangest election in U.S. history (at a minimum in our lifetimes).

Our advice? Stay the course. Trust your plan, do not engage in market timing and avoid making decisions when you are emotional or stressed out. The volatility we just saw may return soon, and if it does, our resolve will be tested. However, we’re still in a solid place as we head into the last four months of the year.

Coming this week

- This week will shine a light on which direction the Fed is headed. We’ll hear from Raphael Bostic, president of the Atlanta Fed, on Tuesday, and the minutes from the July FOMC meeting will be released on Wednesday.

- By far, the most important communication from the Fed this week will be Chairman Jerome Powell’s comments at the annual Jackson Hole symposium, where he has dropped some significant policy decisions in the past. Remember 2022? He basically sealed a crappy year for the market with a very short and terse speech, saying the Fed was nowhere near done. Then the Fed proceeded to double rates. Markets will keep a close eye on Powell’s comments.

- Events in the Middle East and the Ukraine-Russia war have the potential to impact markets this week.

- The current earnings season is winding down. With 91% of the S&P 500 reporting results by Aug. 9, 78% of companies reported a positive earnings per share (EPS) and 59% reported positive revenues. Earnings growth for the second quarter is 10.8%, the highest since the fourth quarter of 2021.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

8/24 – 3757920-3