AE Wealth Management: Weekly Market Insights | 10/8/23 – 10/14/23

Weekly Market Commentary

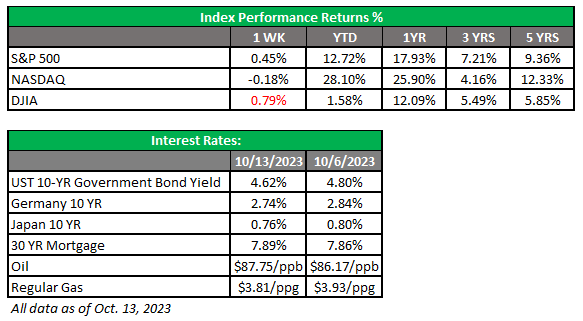

THE WEEK IN REVIEW: Oct. 8-14, 2023

Markets quietly come back

Despite the conflict in Israel, markets rallied early last week, and the potential for added turmoil in the Middle East had not had any measurable impact on the markets through the middle of the week. The Producer Price Index (PPI) numbers came in hotter than expected on Wednesday, which also didn’t faze the markets — but they’d had enough by Thursday, even though the latest core Consumer Price Index (CPI) report was below expectations.

The problem? Core CPI is the Federal Reserve’s preferred measure of inflation, but regular ol’ CPI rose and wages were soft. Plus, the realization of what Israel will need to do to rid the world of Hamas and the potential for a wider conflict sent markets tumbling. Things settled down somewhat on Friday while markets drifted downward, yet we somehow managed to end the week with a gain despite the geopolitics and inflation data.

We had dipped as low as 4,229 on the S&P 500 on Oct. 3, but last week we closed up slightly at 4,328. It appears the slide has ended for now, but the Middle East situation could have such an outsized impact that even if the Fed backs off, markets might hardly notice.

We talk a lot about the possibility of an unforeseen event dominating markets when we try to estimate what direction they will go. Usually, those events are geopolitical and completely unexpected, making it even more imperative to properly control the things we can: things like a functioning government, responsible fiscal policy, low inflation, affordable and abundant energy, plus happy and thriving consumers. Then if we do get blindsided, we can keep functioning even though recovery may be difficult.

We have a lot of manufactured, self-inflicted problems this time around, and less room on our financial and emotional shelves to deal with yet another major crisis. The Israel-Hamas situation could potentially get bigger and uglier quickly, and markets may not handle it well given what is already on our plate.

Fed signals dovishness

The minutes of the last Fed meeting were released last week and revealed the Fed was inclined to delay additional rate increases. According to a Reuters article: “Rising Treasury yields in recent months may be doing some of the U.S. central bank’s work for it, Dallas Fed President Lorie Logan and Fed Governor Christopher Waller have argued, preventing any urgent need for another rate hike.”

The minutes also showed the talk was more about the potential of additional increases driving the economy. The PPI data wasn’t hot enough to derail that talk, and that seemed to be enough to keep markets happy through the end of Wednesday. But reality finally caught up with markets on Thursday, as the CPI came in at 3.7% after bottoming out in June at 3%. The Fed’s preferred Core CPI dropped to 4.1%; the continued decline is enough to keep the Fed idle, but it underscores what we’ve noted before about the difficulty of taking inflation from 3%-4% to 2%.

Now Fed leaders are faced with the realization that if they move further, they could break something. But if they do nothing, inflation and rates will remain at these levels, ultimately strangling the economy. And if they lower rates while inflation is elevated, it could restart the inflationary cycle. All this rate posturing might seem really important at the moment (and if there’s nothing else out there it clearly will dominate the market’s conversations), but we know the asymmetrical effect of the conflict in the Middle East if it expands beyond just Israel and Hamas. If the conflict spills over and engulfs the region, the last thing we will be worrying about is interest rates. This isn’t a pleasant place to be, but at least the markets gave us some relief as we finished up last week.

Coming this week

- Lots of Fed officials are hitting the speaking circuit this week. Philadelphia Fed leader Patrick Harker will speak almost every day, while John Williams will discuss monetary policy on Tuesday and Wednesday. Raphael Bostic and Austan Goolsbee will chip in with their view on Thursday, while Loretta Mester of the Cleveland Fed will finish off the week. It will be interesting to see how aligned these individuals will be with what we saw in last week’s minutes. How open are they to stopping rate increases, and what will their timing be?

- There won’t be one major driver from a data perspective this week, but we will have a smattering of insights. We’ll see retail sales, industrial production, business inventories and the housing market index on Tuesday. Mortgage applications, housing starts and the Fed’s Beige Book will be reported on Wednesday. Then on Thursday, we’ll get jobless claims, the Philly Fed, existing home sales, leading indicators and the Fed balance sheet. Plus, there will be bond auctions all week, so there’s a chance for some excitement there.

- Earnings season has started and that, along with any new developments in Israel, will probably have an impact on markets all week.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

10/23-3143466-3