AE Wealth Management: Weekly Market Insights | 7/14/24-7/20/24

Weekly Market Commentary

THE WEEK IN REVIEW: July 14-20, 2024

The wheel in the sky keeps on turnin’ …

There’s some spinning and turning going on and we don’t know where we’ll be tomorrow. Last week, we continued to see a major rotation from high-flying tech and growth stocks to what has been called the “old economy:” more small cap and value, stable balance sheets and more reasonable valuations.

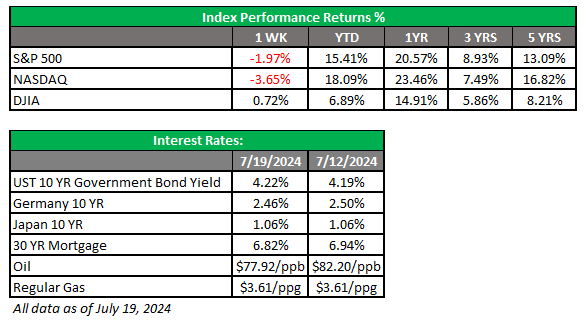

The week was punctuated with bizarre fluctuations, with the S&P 500 hitting an all-time high at the end of the day on Tuesday and closing at 5,667.20. Then, just as quickly, it sold off to end the week. The Dow finally closed solidly above 40,000 and stayed there for the first time as it set a new record (above 41,000 on Wednesday) before selling off as well.

The constant bummer last week was the Nasdaq, which has been soft since setting an all-time high on July 10. Investors began to see the limit of just how high some of these tech stocks can go in the near term and began moving profits out of the tech-heavy Nasdaq and, by extension, growth stocks that have been driven up. There was also concern through the markets about comments regarding Taiwan and the effect it may have on chip makers, plus higher-than-expected unemployment claims.

This all contributed to the general mood that some of these outsized valuations needed to be trimmed. But where did the money go? Here’s a hint: The Russell 2000 — the only other major index that has not had a new record high in 2024 — has been up nearly 10% since the end of June after doing nothing for the first half of 2024. The other beneficiary is large value, which is up over 6% since the beginning of this month. And some of this was likely plain ol’ profit-taking with money sitting in cash on the sidelines.

Last week’s moves aren’t unexpected. We have had hardly any volatility this year, and the VIX (which measures volatility) was up 33% last week. The run-up in a select group of very few stocks could not go on forever. Higher-for-longer interest rates, delayed rate cuts and this wacky presidential race have all converged, and the markets needed to make sense of it all.

When you have had as quiet a first half as we have had, any market noise is deafening. We need to get used to the reality that volatility is a fact of life when we invest in the markets. It is also unnatural for a few names to continue to grow forever while everyone else treads water, and last week is a classic example of profit-taking and reinvesting or setting money aside for new opportunities.

The economy is still sound; we have seen weakness but not collapse, so the “soft landing” narrative is still in play and what rate cuts we see will be gradual and orderly as our economy picks up steam rather than a desperate attempt to restart a failing boiler that has gone cold. To keep the Journey theme going, the wheel in the sky keeps on turning and so will the markets in the near term, despite last week’s volatility.

Talking politics

Speaking of a wacky election season, markets have so far been aloof when it comes to who gets elected in November. But things have definitely changed over the past few weeks, starting with the assassination attempt on former President Donald Trump. The Republicans had a really strong and unifying convention last week, while calls for President Joe Biden to step aside grew louder. Those calls came to fruition over the weekend when Biden said he would end his campaign and endorsed Vice President Kamala Harris to be the Democratic candidate.

With all this going on, the markets finally took notice last week. Not all of the volatility was due to politics, but markets began to realize that a shift in policy might be on the horizon if Trump is re-elected. Markets will calibrate this week as they begin to process the fact that the Trump-Biden rematch isn’t happening and that a new Democratic nominee will be named.

Coming This Week

- How’s the housing market doing? We’ll see some real estate data in the first half of the week, with existing home sales on Tuesday and new home sales and MBA mortgage applications on Wednesday.

- Thursday will be a big day for unemployment claims, which have been climbing steadily.

- The other big deal on Thursday will be the initial reading of second-quarter gross domestic product (GDP). This is the granddaddy of all economic indicators because it’s a measure of broad economic growth. Right now, the economy is decelerating, and GDP will tell us just how much and whether we’re on a path to a soft landing or not. The Atlanta Fed is currently expecting 2.7% annual growth in the second quarter, which feels on the high side. Suffice it to say that this will be a closely watched report.

- Finally, on Friday we will get the Fed’s favorite inflation readings of personal consumption expenditures (PCE). We need to see lower numbers on this front, which will show continued improvement on inflation and bolster arguments for a rate cut sooner than what the Fed is currently telling us.

AE Wealth Management, LLC (AEWM) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

7/24 – 3674748-4