AE Wealth Management: Weekly Blog Insights | 1/30-2/5/22

Meta’s faceplant!

The market was coming back after its worst month since March 2020 — but then the nascent relief rally received a reality check last Thursday. During the early part of last week, we ripped upward on the back of a strong fourth-quarter gross domestic product (GDP) reading, while blowout earnings from Apple and Google kept markets chugging along.

The market played this game of cherry-picking company earnings while ignoring weak economic data, as well as Ukraine/Russia tensions and its potential impact on energy prices even as oil surpassed $90 per barrel. The Federal Reserve is still on track to raise rates in March and the U.S. 10-year Treasury yield crossed over 1.90%. The ADP jobs number showed a net loss in jobs in January and the Job Openings and Labor Turnover Survey (JOLTS) shows nearly 11 million job openings.

But then we had disappointing news, earnings and guidance from Meta (Facebook’s parent company) and PayPal, which showed just how fragile this market is. On Friday, the markets fixated again on stellar revenues from Amazon to push higher. We also had a strong Bureau of Labor Statistics (BLS) employment report, which all but solidifies a move in March from the Fed. Last week was less hectic than the one prior, but it was turbulent just the same. It’s possible we will put in fresh lows before things get better.

The jobs conundrum and the Fed

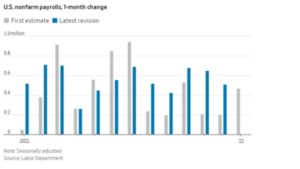

After much hullabaloo over the fourth-quarter GDP increase of 6.9%, the grim reality of a slowing economy has resumed — but is the economy really slowing? Not if you look at jobs this past month. The ADP number showed a net loss of 300,000 jobs, while consensus expectations for Friday’s BLS non-farm payrolls called for a gain of only 150,000. There was a lot of handwringing, and all kinds of reasons were given in advance for a weak number (on top of an already weak +199,000 in December). But the actual number on Friday was an eye-popping +467,000. In addition, the unemployment rate inched up to 4% from 3.9%, while the December and November jobs numbers were dramatically revised from +199,000 and +249,000 to +510,000 and +647,000, respectively. Wages also climbed 5.7% year-over-year but still trail the rate of inflation.

The BLS cited “changes in their benchmarks” for the revisions, but you have to wonder: How could they be so off? Whatever the case, it appears that if you want a job, you can get one — and there are simply not enough workers available, so wage pressure will continue. Since unemployment has settled in the 4% range, we are pretty much at full employment; you can likely never get to 0% because people move in and out of jobs. This is known as “structural unemployment” and averages about 3%. Structural unemployment can happen for many reasons, including the inability to afford or decision not to pursue further education or job training, choosing a field of study that did not produce marketable job skills, or the inability or decision not to relocate.

That said, it looks as if we are close to full employment, so the only thing likely left for the Fed at this point is to focus on inflation. With the inflation rate running at 7% and wage inflation becoming a bigger deal, the Fed may have to act more aggressively than what the markets are anticipating right now. The challenge is trying to determine how many times — and to what extent — the Fed will raise rates to get inflation in check. There has been no indication other than to expect an increase in the Fed Funds rate in March, and no further guidance other than the data will dictate additional moves. Well, the jobs data has just told us that we are fully employed and wages are going up. Both of these things are an apparent signal that there will be more increases on the table after March.

Coming This Week

- We should see another quiet start to the week, with earnings dominating the conversation.

- On Wednesday, mortgage applications will be reported. If there is weakness in mortgages, that’s usually a bad sign for economic growth. Wholesale inventories will also be reported on Wednesday.

- Finally, the biggest data points this week will be the CPI reading on Thursday and consumer sentiment on Friday. The former will give us a mile marker on inflation and whether there is relief on that front. The latter will provide a glimpse into the consumer’s mood, which has been growing less and less optimistic. Any improvement in either reading would be welcomed.

Have a great week!

Tom Siomades, CFA®

Chief Investment Officer

AE Wealth Management

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AE Wealth Management works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AE Wealth Management. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AE Wealth Management.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The personal opinions expressed by Tom Siomades are his alone and may not be those of AE Wealth Management or the firm providing this report to you. The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

02/22 – 2026797-1