AE Wealth Management: Weekly Market Insights | 10/16/22 – 10/22/22

Weekly Market Commentary

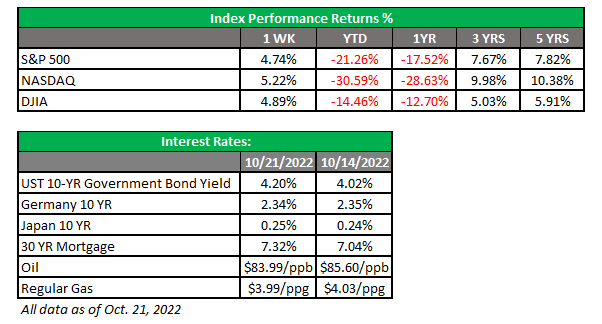

THE WEEK IN REVIEW: Oct. 16 – 22

Earnings keep markets afloat

Some dread existed as third-quarter earnings began in earnest last week. However, earnings have been mostly positive, beating low expectations. Better earnings helped markets last week, but anxiety about the economy’s trajectory and the path of interest rates continues to weigh heavily. We are hovering between a desire for the markets to move upward and concerns that the Federal Reserve will overdo it with interest rate hikes.

Recession seems to be baked into current levels; now, the debate is when a recession could start and how severe it could be. This week we’ll get the initial third-quarter gross domestic product (GDP) reading, which is forecast to come in at +2.4%. A positive GDP number would break the string of two consecutive negative readings, which is the definition of a recession. Even so, the number likely won’t be significantly positive — and when you add all three quarters, we’ll still be negative or flat for the year.

So what’s next? Remember the mantra, “Buy the dip?” That seems to have petered out, but the classic capitulation that typically accompanies market bottoms has also been absent. Does that mean there’s potentially more market pain to come? As far as we can tell, there doesn’t seem to be additional pain lurking right now, unless there is something on the horizon markets haven’t considered.

As I said, recession is already priced in. When all is said and done, the recession could likely be of the “double dip” variety: the current downturn with a break in the cycle for the third quarter and back to negative growth in the fourth quarter and beyond. The markets are trying to gauge how long recession could last, how deep it could go and what may be the catalyst to officially kick it off.

Earnings are softer but keeping us in there. However, there is fear of the Fed overdoing it. Earlier this year, markets had little fear the Fed would stay the course; now they’re concerned the Fed will overshoot and create a deeper economic downturn. It seems like inflation has peaked, and now the question is when we will start seeing a reversal. The concern is that inflation will remain stubborn, and the Fed will keep pushing, which could result in a severe recession rather than a mild one. Right now, the markets are expecting the federal funds rate to increase to 4.5% to 5% by the first quarter of 2023. If the Fed keeps looking for the unemployment number to move higher as a signal to stop rate hikes, it will continue down a more aggressive path and lead us into a deeper recession. But the current employment number seems disconnected from reality. Has it become a flawed measure of economic health in our current environment? For now, we are in a tug of war between interest rates and better-than-anticipated earnings, and the markets are hanging in at these levels.

Top things to keep an eye on the next few weeks

We know these notes have been more negative than positive recently. However, a couple of things in the next few weeks could change the mood. First up: midterm elections. A divided government will remove the possibility of any new spending from Washington in the next two years. Less spending means less contribution to high inflation — and markets would love that. And speaking of inflation, if we resume the negative trajectory in economic growth, people will spend less, and inflation will decline. That may be just the ticket to get the Fed to signal it is backing off from interest rate hikes, and markets would love that as well. The wild card in all this is consumer spending; if spending craters during the crucial holiday season, it could lower inflation faster, drive us into a quicker (and deeper) recession and cause the Fed to pause its hikes. But if spending remains solid, we may be set up for a nice run as we close out the year.

Coming this week

- We’ll see more earnings this week. Among the well-known names reporting this week are Zions Bancorp (Monday); UPS, Coca-Cola, Alphabet (Google), Valero Energy and General Electric (Tuesday); Apple, Meta (Facebook), Ford Motor Co., Kraft Heinz Co. (Wednesday); Twitter, Southwest Airlines, Amazon, Comcast, Intel, Mastercard, McDonald’s and Merck & Co. (Thursday); and Exxon Mobil (Friday).

- Earnings will be the heaviest on Wednesday and Thursday and could make or break markets this week. If big names like Apple, UPS and Google can report at or slightly better than expectations, the markets could rise on those announcements.

- Consumer confidence, mortgage applications, new home sales, and wholesale and retail inventories on Tuesday and Wednesday will show to what extent the real estate market has slowed and if the consumer continues to hang in there. On Friday, we’ll also get a reading on consumer spending and sentiment plus pending home sales.

- The initial reading of third-quarter GDP will be the biggest piece of economic data this week. If GDP comes in stronger than expected, markets may interpret that as a reason for the Fed to keep raising rates. This will be another example of “good news is actually bad news” for markets.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

10/22-2454690-4