AE Wealth Management: Weekly Market Insights | 12/3/23 – 12/9/23

Weekly Market Commentary

THE WEEK IN REVIEW: December 3-9, 2023

Markets resume upward momentum as we near year-end

Markets had a decent week after a slow start. After the ADP employment report, Job Openings and Labor Turnover Survey (JOLTS) and Bureau of Labor Statistics (BLS) employment situation summary — aka “nonfarm payrolls” — all showed slowing job growth, markets picked up some steam as we closed out the week at the high for the year.

The employment readings all but cemented no additional rate increases at the Federal Reserve’s final meeting of 2023 happening this week. Now the debate shifts to how soon the Fed will start talking about cutting rates. The markets aren’t buying the “higher for longer” posture the Fed is taking.

Instead, markets are thinking the Fed won’t have the stomach to go the final mile to crush inflation back to its target 2% from the current ~3% level, because that will tank the economy and spike unemployment. In fact, with the elections next year, there will be immense pressure on the Fed to boost the economy via lower rates because no incumbent wants to face unemployed and angry voters. That’s the market’s take.

The November Consumer Price Index (CPI) and Producer Price Index (PPI) will be released this week and may provide some impetus for the Fed to signal cuts. It’s not likely the CPI or PPI will suddenly increase, especially with gas prices where they are. But would a possible sub-3% reading be enough to push the Fed to act? And when the Fed eventually does start cutting, will it be because bad news has finally become bad news and we are in a recession?

For now, simply talking of rate cuts is enough to drive the markets upward. They’ll likely continue that direction as we race toward the end of the year and visions of rate cuts dance in their heads.

Where are all the jobs?

Jobs are available — but job growth has slowed. Job openings, as measured by the JOLTS report mentioned earlier, dropped to the lowest level since March 2021. Only a few months ago there were two jobs for every one worker; now, there are 1.3 job openings per worker, back to pre-pandemic levels.

Keep in mind that the JOLTS number is fairly dated when it’s released. The data wasn’t reflective of what happened in November; instead, these numbers were for October and gathered in November. The trajectory has been going downward slowly, so it is quite possible the current ratio is actually closer to one opening per worker or even worse. All the major strikes are over, and the job market is still slowing.

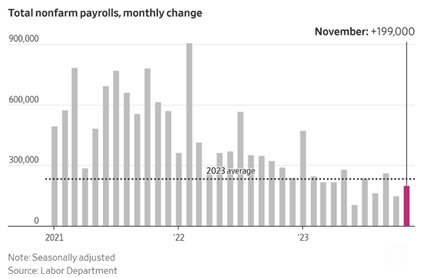

Friday’s BLS employment situation showed an increase of 199,000 jobs against a consensus of 180,000. This was higher than October’s +150,000, but it also included all the auto workers who came back from their strikes. Unemployment dipped from 3.9% to 3.7%, which was mostly due to the worker participation rate increasing. Most of the job gains were in health care (+77,000) and the government (+49,000).

The slowing jobs data keeps the narrative of the soft landing intact. Open jobs are evaporating and hiring is cooling, which means the Fed does not need to raise any more because we are trending downward. The question will be where and when do we level off? Markets are betting the Fed will begin to hit the gas pedal earlier rather than later.

Coming this week

- The final Fed meeting of 2023 will take place on Tuesday and Wednesday, with a decision on the fed funds rate announced on Wednesday afternoon. What will be key is any language from Fed Chair Jerome Powell that even hints of rate cuts. Based on the jobs number last week, he will likely remain tight-lipped and noncommittal, spinning the well-worn “data-dependent” story.

- The latest inflation data will be on display on Tuesday as we get the November reading of the CPI. We were running at a 2% year-over-year rate in October, and with gas prices lower across the board, we will likely see inflation drop again.

- November PPI will be released on Wednesday. Last month’s PPI reading was negative but probably won’t be again this month as that would be a deflationary trend. We’ll also see the MBA mortgage applications on Wednesday.

- The rest of the week will be pretty humdrum from a data standpoint. However, based on what Chairman Powell says and the inflation data, there should be a lot of action in the latter part of the week.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

12/23-3265034-2