AE Wealth Management: Weekly Market Insights | 2/25/24 – 3/2/24

Weekly Market Commentary

THE WEEK IN REVIEW: Feb. 25 – March 2, 2024

New records for the S&P 500 and Nasdaq

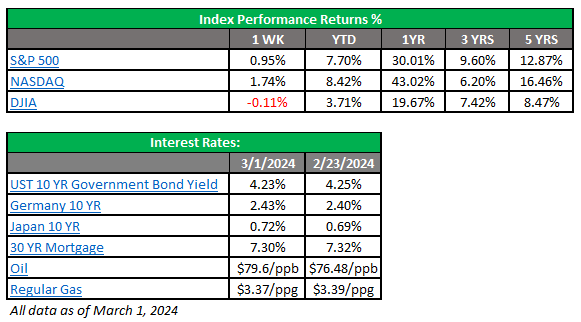

The market keeps on rallyin’. Both the S&P 500 and the Nasdaq pushed to record highs last week, surpassing highs from early 2022. February was a strong month for each major index, and U.S. stocks have had their best start to a year since 2019.

The most significant market mover last week was the core personal consumption expenditures (PCE) report on Thursday. Core PCE measures what consumers spent in the past month, minus food and energy, and is the Federal Reserve’s preferred gauge of inflation. This number rose 2.8% year-over-year in January, aligned with forecasts. Overall PCE fell to 2.4% that same month, down from 2.6% the month prior. Stocks jumped following the report’s release.

Still, the Fed seems unfazed and determined to stay the course. A barrage of Fed officials (12, to be exact) took to their respective podiums last week, delivering similar “stay the course” messages. It seems very likely they won’t be cutting rates at their meeting coming up on March 19-20 and probably not in late April.

One sour note for markets last week was the Institute for Supply Management’s (ISM) manufacturing activity report. The number came in substantially below expectations, falling from its 18-month high of 49.1 in January to 47.8 in February. (Readings above 50.0 indicate economic expansion.) The combination of the core PCE numbers and manufacturing activity report pushed the yield on the benchmark 10-year Treasury note to its lowest intraday level since Feb. 13 by the end of last week.

Barring any surprises from the Fed (not likely) or unexpected events, the month of March is shaping up to be similar to February for markets. One area to watch: the Red Sea, where attacks against cargo ships have caused shipping costs to rise over 150%. While we probably won’t see the same level of supply chain issues that we saw in 2020-21, higher shipping costs mean higher production prices — and ultimately higher prices (once again) for consumers. That will definitely be a factor for the Fed as they decide whether or not to cut rates in the second half of the year.

Coming this week

- Fed officials are still on the speaking circuit this week. Chair Jerome Powell will be testifying to Congress in the middle of the week, while six additional officials are scheduled to talk.

- We’ll see the latest employment data this week, with job openings released on Wednesday and the Bureau of Labor Statistics’ (BLS) nonfarm payrolls and unemployment rate on Friday.

- Other data this week includes factory orders and ISM services (Tuesday), wholesale inventories (Wednesday) and hourly wages (Friday).

Sources:

https://www.morningstar.com

https://www.cnbc.com

https://www.marketwatch.com

https://markets.businessinsider.com

https://ycharts.com

Accessed 03/01/2024

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

3/24-3425868-1