AE Wealth Management: Weekly Market Insights | 6/11/23 – 6/17/23

Weekly Market Commentary

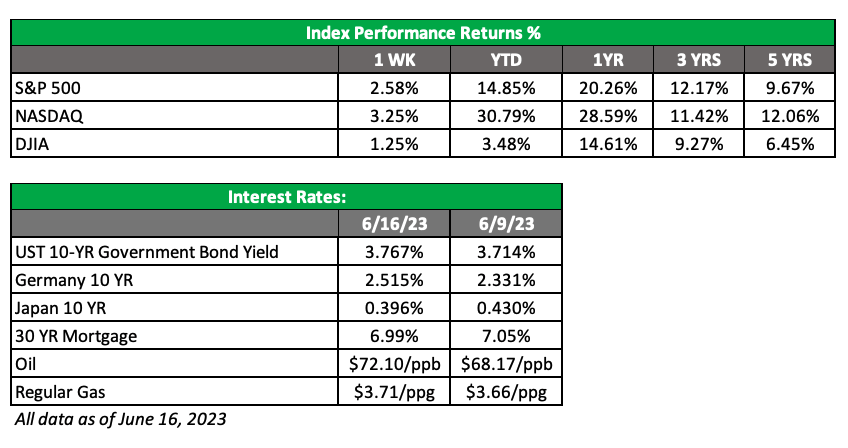

THE WEEK IN REVIEW: June 11-17, 2023

The 11th time is the charm!

Stop, skip — or something else? As expected, the Federal Reserve left interest rates alone last week after raising rates at its prior 10 meetings. Markets have been clamoring for a cessation in rate increases since the beginning of the year, but the Fed didn’t seem moved to pause until the recent bank failures. Breaking the housing market wasn’t enough; it took some very high-profile banks to implode to get the Fed’s attention. The Fed still raised rates as Silicon Valley Bank and Signature Bank collapsed but seemed to have thrown in the towel after First Republic Bank rolled over in May.

Fed Chair Jerome Powell had some cover this time around with the consumer price index (CPI) down well over half from last June’s peak (more below). However, he also hinted in post-meeting comments that there could be more hikes later this year. Sure, it sounds prudent to see what the ramifications of our actions are on the economy. But this pause sounds a lot like when a candidate announces they’re “suspending” their campaign and we all know they’re really done.

It feels that we’re nowhere near where we need to be on inflation and the fundamental factors are still in place to keep inflation “sticky.” The talk of more potential hikes later in the year was meant to dispel any talk of rate cuts in the next few months and cap some of the euphoria in the markets. The Fed is trying to have it both ways — and the market doesn’t seem to be buying it. We moved out of the 4,000-4,200 range on the S&P 500 as soon as a debt ceiling deal was imminent, then ran up to 4,400 in anticipation of the Fed’s pause. We finished the week very strong, and the markets, which have been hamstrung the entire first half of the year, are looking to run.

The Fed may come back in a few months and actually do what it said it will do. However, all signs seem to point to it being done, and that it won’t have the willpower to resume increasing rates. The economy is slowing, credit card balances are rising and mortgage rates are high. Plus, we’re approaching an election year, and incumbent politicians won’t want a lethargic economy with frequent layoffs and sour consumers. Inflation will not go away; we will just have to live with it and hope it goes lower based on what the Fed has done until now.

Inflation cut in half from last year’s peak

We got some good news on inflation ahead of the Fed’s meeting, which validated the decision to pause raising rates and let markets take off. The May CPI reading came in at 4.0%, down nearly 1% from April. That’s more than half the level we were at during last June’s peak of 9.1%.

Good news, right? Things are definitely better this year; in 2022, we were dealing with supply chain hangovers, pandemic stimulus cash, the insane price for a dozen eggs and extraordinarily high gas prices. But the decline in gas prices isn’t because there is more oil being pumped. Instead, it’s because world economies are slowing, and less demand means the price of oil falls.

If you look more closely at the numbers, you’ll see that core consumer prices, which exclude volatile food and energy categories, climbed 5.3% in May from a year earlier. That reading includes housing, which is still elevated. Economists see core prices as a better predictor of future inflation, and the Fed says it is watching the core number, not the CPI.

The good news is producer prices continue to decline. The producer price index (PPI) peaked at 11.7% in March 2022, and it took three months for interest rate hikes to filter their way through producer prices and to consumers. It appears there is more room for CPI to come down, but the core number seems to have stagnated. Getting the core number where the Fed wants it could be painful for the economy and potentially met with resistance in an election year. The Fed is talking tough, but it probably won’t act again, and all the players will cite a lower CPI as a sign of victory to further their self-interests.

Coming this week

- Markets were closed on Monday for Juneteenth, so it’s a short trading week. We should see some follow-through from last week’s post-Fed-meeting rally.

- This week will be pretty quiet from a data standpoint. We’ll see a bill auction on Tuesday and mortgage applications on Wednesday. Thursday will be busier but nothing to get overly excited about: The schedule includes more bond auctions, existing home sales, leading indicators and the Fed balance sheet.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

6/23-2937057-3