AE Wealth Management: Weekly Market Insights | 7/18/22 – 7/24/22

AE Wealth Management: THE WEEK IN REVIEW: July 18 – July 24

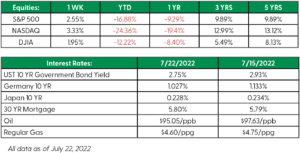

What do we have here? An up week for markets!

Stocks had a strong showing last week. It may sound strange, but traders appeared to welcome signs of a slowing economy and fading inflationary pressures. Weekly jobless claims came in at 251,000, their highest level in nine months, as some companies begin precautionary layoffs as a potential recession looms.

Other data from the housing, manufacturing and service sectors also indicated a sluggish economy. Existing home sales declined 5.4% between May and June, and they’re down 14.2% from one year ago. Mortgage applications dropped 6.3% last week, hitting their lowest point since 2000. The U.S. Treasury yield dropped on the heels of the negative data, hitting a two-month low of 2.73% on Friday.

Earnings season is in full swing, and so far it’s been a mixed bag. Many earnings reports confirmed the economy is slowing, but corporate profits and outlooks were somewhat better than expected. For example, Netflix’s share price rose after reporting it had lost fewer subscribers than expected last quarter following a significant price jump.

U.S. Treasury yields dropped on the heels of the weak data. The yield on the benchmark 10-year Treasury note dropped to 2.73% on Friday morning, its lowest level in nearly two months.

While markets seemed to absorb all of this in stride last week, this week could be interesting as the Federal Reserve holds its regularly scheduled meeting. The majority of economists are anticipating the Fed to raise rates by another 75 basis points (0.75%) during their meeting, taking the fed funds rate to 2.25% – 2.50%. A small number are still saying they expect the Fed to implement a full 1% increase. If the outliers are right, it could increase volatility, as markets seem to be resigned to a 75-point hike.

Another potential point of volatility this week: The first reading of second-quarter gross domestic product (GDP) is scheduled for Thursday. First quarter GDP came in at -1.6%, and two negative quarters in a row would mean we’re “officially” in a recession. Right now, the forecast for second-quarter GDP is coming in at 0.3%, so which way it will go is anyone’s guess.

Coming This Week

- The biggest event this week will be the Fed meeting Tuesday and Wednesday. As mentioned earlier, a federal funds rate increase of more than 75 basis points could create turbulence for markets.

- Second-quarter GDP is scheduled to be released Thursday.

- We’ll see more housing data this week, including new home sales for June. The forecast is calling for sales to drop to 664,000, down from 696,000 in May.

- Friday will be a heavy data day. We’ll get numbers on disposable income, personal consumption expenditures (PCE) price index and the final reading of consumer sentiment and inflation expectations.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

7/22 – 2271280-4