AE Wealth Management: Weekly Market Insights | 8/6/23 – 8/12/23

Weekly Market Commentary

THE WEEK IN REVIEW: August 6-12, 2023

Sticky inflation

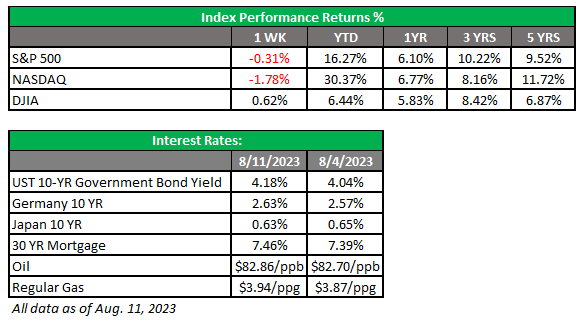

Inflation, as measured by the consumer price index (CPI), came in at 3.2% year over year for July, up 0.2% from June’s reading of 3.0%. The producer price index (PPI) was also elevated from the June reading, yet the year-over-year rate remained at 2.7%. Core inflation ticked down 0.01%, leading to some optimism that it might be enough for the Federal Reserve to stay in pause mode.

As we’ve said before, energy prices — and more specifically, gas prices — need to be monitored because as they go, so does inflation. We’ve seen a decline in most commodities so far this year, with gas prices dropping close to $3 per gallon last December. However, prices have steadily crept upward all year, and the average price of regular gas topped more than $3.90 per gallon late last week.

Food prices are also on the rise, and with food and energy costs moving higher, it’s easy to see why the decline in inflation has come to a stop and is showing signs of reversing. This puts the Fed back in the crosshairs: Do they continue to pause? Is one more rate hike on the table or should we expect more? Has the Fed done too much — or not enough? Is a recession still lurking just over the horizon?

Looking at the Treasury markets, the 10-year note has climbed above 4%, which doesn’t bode well for the stock market nor the broader economy. Summer is winding down, there isn’t much additional data right now and the markets have done well so far this year, so it may be logical to stop and consolidate at the 4,500-ish level on the S&P 500.

One concern is that there won’t be much news, and if the scant news is less than spectacular, it could set a negative tone for the end of the third quarter. September and October aren’t great months for markets from a historical perspective, and a lack of data means idle hands do the devil’s work. Keep focused and stay on track; this isn’t a time to overextend yourself. We may still have a strong ending to the year, but the next two months could challenge our patience. Rely on the plans you have built and trust the discipline.

Not in a party mood

A week after Fitch’s downgrade of U.S. government debt, Moody’s downgraded some large U.S. financial institutions. The downgrades were mostly in response to high-profile regional bank failures, notably Silicon Valley Bank, Signature Bank and First Republic Bank.

Moody’s report highlighted some of the issues that caused the banking crisis earlier this year, noting those issues haven’t disappeared. Banks are still at risk for depositors to withdraw their funds, while higher interest rates are knocking down the value of investments lenders made when rates were super low.

The rating agency added that asset risks are also rising for small- and mid-sized banks, especially those with large corporate real estate holdings. The biggest names on the list were M&T Bank (the 19th largest U.S. bank) and BOK Financial. Moody’s also placed six banks on review for possible downgrades, including Northern Trust, Bank of New York Mellon, U.S. Bancorp, Truist and State Street.

Needless to say, the Moody’s report seemed to send shivers up and down Wall Street. After a promising start to the week, markets sold off on the news. And although inflation data initially fueled a rebound, markets struggled to end the week. The downgrades seemed to set a sour mood and the inflation data kicked up old worries that the Fed isn’t done raising rates and that the economy is in sad shape. Talk about setting a dark mood.

Coming This Week

- The dog days of summer were supposed to be over Aug. 11. But as far as economic data is concerned, the dog days will persist as data remains nonexistent this week.

- What data there is includes retail sales, business inventories and bond auctions (Tuesday); mortgage applications, housing starts, industrial production and the minutes from the last Fed meeting (Wednesday); and unemployment claims, leading indicators, another bond auction and the Fed’s balance sheet (Thursday).

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

8/23-3022085-3