AE Wealth Management: Value of Financial Planning | Blog

THE VALUE OF HAVING A FINANCIAL PLAN

The Wealth Report by AE Wealth Management

Download PDF Version Here

One way to help weather volatile markets, meet financial objectives and manage risk is to have a carefully constructed financial plan.

Overview

One of the most important ways investors can endure the up-and-down nature of investment markets is to have a financial plan in place. Establishing specific financial goals, a timeline for reaching those goals, an asset allocation strategy and an appropriately constructed portfolio that includes liquidity options are all significant components of a sound financial plan.

One of the reasons financial advisors recommend having a financial plan is to help investors avoid panic selling. If you have considered the growth potential and market risks of each of your investments, a plan can help you avoid losses and stay on course to meet your goals.

Without a plan, you may be subject to emotional responses and sell for a significant loss because you can’t take the stress of watching your investment lose money day after day. Perhaps the greatest value of a sound financial plan may be the ease of mind that helps you weather market volatility.

Remote Income

Many people still worked from home in 2021, our second year into the pandemic. However, for some, “home” was wherever they could access Wi-Fi on their laptop. A number of employees took the opportunity to do some traveling while still holding down their daily job. The problem is that when you earn income from outside of your home state, you may, in fact, owe taxes on that income in both states. If you traveled all over the country, you may have to file taxes in states where you worked for the money you earned during the time you were there.

Each state has different rules related to how long you were there and how much you earned. Some have temporary waivers or reciprocal agreements with other states, but only six states tax you strictly on where your employer’s office is located.2 Note, too, that not all tax advisors are licensed to file taxes in every state. You could enlist a tax advisor in each state, but it may be cheaper to hunker down and file all those taxes online yourself.

The situation can be even more complicated if you lived at least half the year in a state other than your home state. In this situation, earned income and investment income may be taxable in both states. Moving forward, it’s important for remote workers to request that their employer make the proper state withholding and perhaps even establish an office at that teleworking location to avoid paying double taxes.

“Historically, what we’ve seen is that every time there’s news of high inflation, the markets get spooked very easily.” — Joao Gomes, Wharton finance professor1

Inflation Concerns

After many years of low inflation, today’s rising prices have the potential to derail investors in two ways. First, they can diminish the value of assets that do not adjust for inflation, such as U.S. Treasury bonds or corporate bonds. Second, if and when the Federal Reserve increases interest rates, this will serve to reduce the value of other assets, such as stocks and real estate. Therefore, even if your investments are diversified, the possibility of rising inflation can impact many aspects of your portfolio.

The following is an overview of how rising inflation can potentially affect certain assets.2

- Higher interest rates can force growth-oriented companies (dominated by tech) to curb spending and expansion, which can slow profits, impede current cash flow and stem share price increases.

- Value stocks, like financials, consumer discretionary and energy, tend to be more shielded from higher inflation because they have lower price-to-earnings ratios than growth stocks. Therefore, value stocks tend to outperform growth stocks during inflationary periods.

- Bond prices move in the opposite direction of interest rates, so as rates increase, their value declines.

- An increase in interest rates compounds over time, so the value of longer-duration bonds is reduced — because their cash flows are further out in the future.

- Shorter-term bonds are less impacted by rising rates because they yield near-term cash flows.

- Commodity prices increase and tend to outperform other asset classes when inflation rises because their consumer prices, such as gas and food, increase as well.

- Property values and rent tend to rise with higher inflation because higher interest rates curb the flow of mortgage and construction loans.

Market Volatility

Market corrections and bear markets are historically common, regular and short term. It is considered healthy for the market to periodically reset to prevent asset “bubbles” and keep valuations in check. Otherwise, investors would always buy at top-of-market prices to expand their positions. However, a market decline can present a good opportunity to purchase equities at lower prices.

The Value of Staying on Course

The garden-variety wisdom is to hunker down and maintain a long-term perspective when the market experiences a correction or prolonged bear market. It is important to remember that investing is a long-term endeavor. The goal should be less about outperforming indexes and more about giving your money time to grow, uninterrupted.

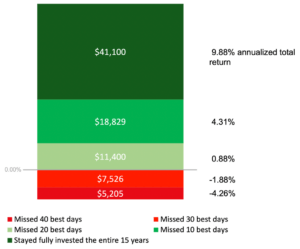

Only time in the market will allow you to benefit from periods of rising prices — or recover from periods of declining prices. Staying in the market during price declines can be an important part of the investment discipline. In fact, even short periods out of the market can have a substantial impact on investment returns, as illustrated in the accompanying chart.

In this scenario, the investor who stayed in the market for the full 15 years would earn $22,271 more than if he or she had periodically pulled out and missed the market’s 10 best days during that time frame.3

$10,000 Invested Over 15 Years in the S&P 500 Index4

Dec. 21, 2005 – Dec. 31, 2020

Tactics

Periodic market setbacks should not be that concerning and often position a portfolio for higher growth in the future. However, if you’re struggling with today’s market volatility, consider the following tactics to help keep your investment portfolio — and your emotions — even keel.

Diversify

When an investor maintains a diversified portfolio, it’s not likely that any one investment will tank his finances or create exorbitant wealth. Spreading out assets and maintaining that allocation over the long haul can help minimize risk and capture growth opportunity from a variety of different asset classes and market sectors.

Strategic Asset Allocation

The key to choosing investments is to first determine your goals. Few investors are simply looking to earn lots of money. They actually have objectives for how they intend to use the money they accumulate, such as buying a home, paying for their children’s college education or providing income during retirement. For example, a college savings 529 plan is designed to yield the funding needed by the time children graduate from high school. An employer-sponsored retirement account should be allocated to meet a target balance by retirement age.

Asset allocation is the tactic of determining how much money to allot to different asset classes (e.g., stocks, bonds, cash instruments). Each asset class is generally associated with a risk-and-reward time frame for delivering best performance.

Rebalance Regularly

One way to help manage risk and short-term volatility is by rebalancing periodically to maintain the asset allocation designed to meet your goals. Rebalancing generates the opportunity to sell winning positions and reinvest proceeds to maintain the appropriate balance among asset classes.

Dollar-Cost Averaging

Regular, automatic investing takes advantage of dollar-cost averaging (DCA), which is simply investing the same amount of money on a regular basis regardless of market performance. Most people do this through salary deferrals to their employer 401(k) plans. That regular contribution buys more shares when prices drop and fewer shares when prices rise. The benefit of DCA is that the cost basis of the total investment generally reduces over time.5 It also takes the guesswork out of when to invest. However, note that dollar-cost averaging does not ensure a profit nor does it protect against losses in declining markets. It involves continuous investing regardless of fluctuating price levels, so you should consider your ability to continue investing through periods of fluctuating market conditions.

Transfer Your Risk

Another way to help add security to your financial plan is to diversify your income sources so that you have multiple streams in case one or more are threatened by market or economic conditions. For example, you could create an alternative income stream by transferring your risk of loss from your investment portfolio to an insurance company. By repositioning a portion of your assets to purchase an annuity, you can count on receiving insurer-guaranteed income throughout retirement.

“If you’re taking more risk than you’d like and your portfolio dropped more than you could bear in January, take this as a signal to rebalance and move forward with confidence.” — Sam Swenson, contributor for The Motley Fool6

Final Thoughts

There can be more than one path to meet your financial goals. If your current asset allocation strategy is giving you cause for concern, you may want to discuss your options with a professional.

In other words, you can stay the course but still make changes to your portfolio. This is particularly true once you’re in retirement, as the changing market environment may weigh relentlessly on your mind. That can get in the way of enjoying a high quality of life during retirement. Remember, you can be flexible and still maintain a long-term perspective.

It’s important to establish a relationship with an advisor who understands your needs. Together, develop a financial plan that offers flexibility to weather changing conditions, as well as reliability, so you don’t have to spend every day worrying about your future.

1 Knowledge@Wharton. Feb. 1, 2022. “What Investors Can Expect from High Inflation and Rate Hikes.” https://knowledge.wharton.upenn.edu/article/investors-can-expect-high-inflation-rate-hikes/. Accessed Feb. 2, 2022.

2 Ibid.

3 Putnam Investments. February 2021. “Time, not timing, is the best way to capitalize on stock market gains.” https://www.putnam.com/literature/pdf/II508-ec7166a52bb89b4621f3d2525199b64b.pdf. Accessed Feb. 2, 2022.

4 Ibid.

5 Adam Hayes. Investopedia. Aug. 19, 2021. “Dollar-Cost Averaging (DCA).” https://www.investopedia.com/terms/d/dollarcostaveraging.asp. Accessed Feb. 8, 2022.

6 Sam Swenson. Nasdaq. Feb. 3, 2022. “4 Critical Lessons From This Stock Market Correction.” https://www.nasdaq.com/articles/4-critical-lessons-from-this-stock-market-correction. Accessed Feb. 3, 2022.

This content is provided for informational purposes. It is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security. Individuals are encouraged to consult with a qualified professional before making any decisions about their personal situation. The information and opinions contained herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management. Neither AEWM nor the firm providing you with this report are affiliated with or endorsed by the U.S. government or any governmental agency. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM. Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

2/22-2022460