AE Wealth Management: Weekly Market Insights | 2/13-3/19/22

VIEW PDF VERSION

A game of chicken (Kyiv)

It’s the worst surprise attack in history that hasn’t happened … yet. It was imminent, inevitable, very high threat, a moment of peril, happening any minute. We told our people to get out, we evacuated and moved our embassy, U.S. Secretary of State Antony Blinken went to the United Nations and Russia said it was pulling troops back, then didn’t.

The market heard what it wanted to hear and rallied last week before its bubble was burst on Thursday after finding out the Russians had done nothing to de-escalate the situation. Consumer spending was surprisingly up in January, and minutes from the last Fed meeting showed they had no desire to raise rates by more than 25 basis points (0.25). However, that was before we got the recent jobs and inflation news.

All this helped push the markets upward in the middle of the week, but as the week wore on, the same old factors — inflation worries, the price of oil, the Fed and the mess on the Russia-Ukraine border — continued to weigh on the markets. Late in the week, the Russians continued their aggressive stance by moving into “firing positions,” and pro-Russian Ukrainian separatists shelled a school in the eastern part of the country. In addition, reports of multiple violations of ceasefires between Russian-supported separatists and Ukrainian government forces were released.

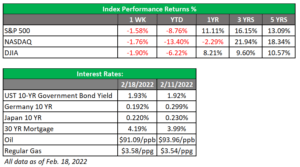

All this activity crushed the markets, with last Thursday closing as the worst day for investors so far this year. There was a flight to safety, and the 10-year U.S. Treasury dropped from 2.05% to 1.93%. The selling continued on Friday as the Russians announced nuclear missile drills. With markets closed on Monday for Presidents Day, no one was in the mood to hold stocks for a long weekend, and the sell-off continued.

Inflation keeps grinding upward

After a really bad reading of the Consumer Price Index (CPI) showed no signs of inflation slowing, last week’s Producer Price Index (or PPI, which shows the cost producers are paying for materials to create products consumers buy) reinforced that inflation is here to stay. President Joe Biden stated in January that it was the Federal Reserve’s responsibility, as one of its two mandates, to control inflation. Yes, it’s true that the Fed has been accommodative in one way or another for well over a decade. However, inflation hasn’t approached current levels during prior periods of accommodation. So, is all this really on the Fed?

We’ve talked in past commentaries about potential policy errors that could derail the economy. In our view, the Fed has already committed two errors — and is on its way to a third that may lead us into a recession. The Fed’s first mistake was buying into the “inflation is transitory” narrative; the Fed should have been stronger in its belief that inflation was not transitory but had its “root causes” in too much money thrown into an economy that may not need it. The Fed had a hand in that, but it wasn’t the only hand that was involved. (More on that in a second.)

The Fed’s second mistake was continuing to throw liquidity into the market. The Fed has yet to remove the quantitative easing it has been providing, which it needs to do to begin the process of curtailing inflation.

The mistake in progress is the Fed heading down the path of not being aggressive enough at the next meeting to address inflation via a strong rate-hike statement (as evidenced by the minutes from the last meeting). What we don’t want to see happen is the Fed remaining flatfooted and being forced into more drastic measures that may tip us into recession.

These mistakes are all on the Fed, but the federal government has created its own policy mishaps that have also contributed to inflation. First, higher energy costs contribute to higher prices; this administration has besieged our energy industry, whether through closing pipelines or making drilling and fracking more expensive, or not granting any new oil and gas leases or allowing them to be renewed. Oil is above $90 per barrel, compared to $60 one year ago and $40 in 2020.

Further proof was with the American Rescue Plan last March, when they flooded another $2 trillion in cash and incentives into the economy, and delayed people returning to work (if they returned at all). The American Rescue Plan and previous “emergency measures” grew the money supply by 40% when many people were already saving at an unprecedented rate during the pandemic. Top that off with vaccine mandates slowing reopenings and further constricting economic activity and production, and it’s safe to say that the federal government did the Fed no favors in righting their wrongs.

One thing is for sure: The Fed can get serious about inflation, stop quantitative easing and raise rates. But the government needs to stop offering lame excuses for inflation, like “a little inflation is good,” “inflation is transitory,” “inflation is caused by price gouging or corporate greed,” etc. The sheer magnitude of excuses tells us one of two things: 1) the government has absolutely no idea what is causing inflation; or 2) the government doesn’t want to admit that it is, at a minimum, partly responsible for the inflation we have. Neither scenario bodes well for the average citizen, and this administration needs to reorient itself and focus on being the people who crushed inflation. How would they do that?

There is too much money chasing too few goods right now, and that’s the classic definition of inflation. Consumers have overspent, and prices have risen. The Fed (with encouragement and public support — not blame — from the government) needs to raise rates. Meanwhile, the government needs to stop spending money and proposing additional spending, and encourage people to work for any benefits they receive. Mandates and restrictions need to stop so the economy can proceed unfettered. It’s time to do something.

Coming This Week

- Markets are closed in observance of Presidents Day on Monday. If something happens with Russia and Ukraine while markets are closed, it may bottle up volatility and potentially lead to a lot of pain when markets finally open on Tuesday.

- We’ll see consumer confidence on Tuesday and mortgage applications on Wednesday. However, data — good or bad — could be overshadowed by events in Ukraine.

- The second reading of fourth-quarter 2021 gross domestic product (GDP) is expected on Thursday. The first reading was +6.9%.

- Finally, on Thursday and Friday, we will have new home sales and pending home sales. Consumer sentiment and spending and durable goods will also be reported on Friday.

Have a great week!

Tom Siomades, CFA®

Chief Investment Officer

AE Wealth Management

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The personal opinions expressed by Tom are his alone and may not be those of AE Wealth Management or the firm providing this report to you. The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

02/22 – 2026797-3