AE Wealth Management: Weekly Market Insights | 5/26/24 – 6/1/24

Weekly Market Commentary

THE WEEK IN REVIEW: May 26 – June 1, 2024

Weaker than expected

Last week was all about economic weakness. We saw it on two fronts: the revised first-quarter gross domestic product (GDP) number and several bond auctions. Although last week was a short one thanks to the Memorial Day holiday, there was enough going on to make up for the day we missed. Frankly, it would have been OK to miss more than one day of trading because the week in the markets was not a good one.

First-quarter GDP was initially reported at 1.6%, but last week it was revised downward to 1.3%. Weak growth revised downward to an even weaker number, coupled with 3.4% inflation (more in the next section), and personal income not keeping up with spending led to a pretty glum mood. When adjusting for inflation, consumption declined, meaning consumers spent more on purchases in April but ended up buying less than they did in March. That just doesn’t add up to a healthy, robust economy and is a large reason why many feel left behind. There are also those experiencing an “emotional recession” — you have a job but aren’t confident in your future, fatigued with high prices and it’s taking more and more money just to keep up.

With that backdrop in mind, we come to the second set of circumstances that we believe caused the market to be crabby and cranky last week. There was a series of bond auctions that were not well received. There wasn’t enough enthusiasm from buyers, which resulted in the government having to offer higher yields to entice buyers. This was the third weak treasury auction in a row.

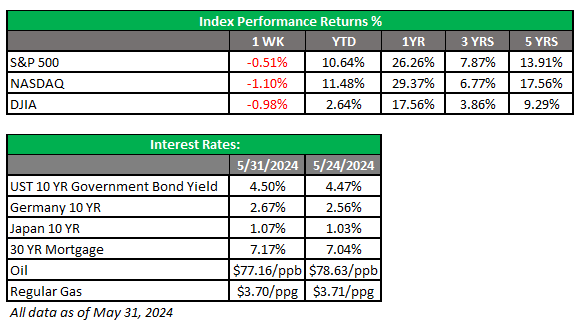

We’ve used the word “weak” a lot in this section: weak economic growth, weak wage growth and now weak demand for bonds. That sounds a lot like things aren’t as rosy as we would like them to be. Higher bond yields make equities less attractive, especially when you can get between 4.5% and 5.2% on U.S. treasuries maturing between two and seven years (the shorter the term, the higher the yield, thanks to the prolonged inversion of the yield curve).

All of this led to a selloff in stocks last week. After hitting 40,000 on May 17, the Dow ended May at 38,706.98. The S&P 500 was off just under 25 points from its all-time high on May 20 (5,308.13) at 5,277.51. Despite last week’s drop, we are still close to all-time highs, and we will see the rally resume if the Federal Reserve signals a willingness to cut. Remember: We want the Fed to cut to keep the economy from stalling and not out of desperation to try and save us from a recession. The next few months will go a long way in deciding which direction we are headed.

Why inflation isn’t dropping

Elevated inflation has been around for over three years now, and the last time we saw a reading below 3% was in April 2021 (2.6%). Sure, 3% may not sound like much — but we were running between a 7% and 9.1% annual rate for a full 12 months (December 2021 through November 2022, with a high of 9.1% in June 2022).

In all, we’ve seen a 17.37% increase in the consumer price index (CPI) since April 2021. Because the memory is so recent, we seem to rebel mentally to accept this. Instead, it can be filed under “I remember when (fill in the blank) cost (fill in the blank)” — because as recently as three years ago, we experienced lower prices from food to gas. As a result, we get mad and aren’t willing to accept the reality because we have seen things get better.

We have become accustomed to a way of life, and as that way of life gets more expensive, we stretch ourselves to maintain it until we finally snap. That is what makes people feel like we’re in an “emotional recession” and why the Fed will not be able to tame inflation because if it continues to keep rates where they are or even raises them to lower inflation to its preferred 2% level, it will virtually guarantee an actual recession. That’s the only difference between a slow death and a sudden one; the results are the same.

The cure for higher prices is higher prices. We will reach a point where we actually say, “No, I will not pay that.” Price increases may then slow, but they will not give up those increases without a painful recession. Right now, we are experiencing a slow death. Real wages are stagnating, the economy is barely growing, interest rates are high and inflation keeps gnawing at our wallets. We can’t seem to get past inflation because we know how it was and so desperately want it to be that way again.

Coming this week

- We are right back on the data train this week. The employment picture is on tap this week; besides inflation or price stability, the Fed’s other focus is the pursuit of full employment. The April unemployment reading was 3.9%, and if we crest 4%, it may spur talk of the Fed lowering rates to bolster the jobs market. However, as we all well know, lower rates most probably reignite inflation, which is already starting to creep upward.

- Monday will be fairly subdued with construction spending, some manufacturing data and auto sales.

- Tuesday will feature factory orders and the JOLTS report. Although this report is useful, it has a full month lag and the jobs openings will be for April. The March reading was 8.5 million, and the market will want to see declines here to signal a softening of the labor market.

- Things will crank up on Wednesday with the usual MBA mortgage applications, plus we’ll have the ADP number for employment in the private sector. The last reading was +192,000, and again, we’re looking for a lower number here. We’ll also get the final revision of first-quarter productivity and the trade deficit.

- Initial jobless claims are on tap Thursday morning. Last week’s claims were 219,000, which was roughly in line with the previous week’s 216,000 but appears to be trending upward.

- On Friday, we’ll get the Bureau of Labor Statistics (BLS) employment situation. We were at 3.9% unemployment last month, and if we hit 4% or more, markets will notice. Last month the BLS reported non-farm payroll growth at 175,000, which is still relatively strong. Consumer credit, wholesale inventories and hourly wages will round out this week’s data dump.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

6/24-3619288-1