AE Wealth Management: Weekly Market Insights | 7/16/23 – 7/22/23

Weekly Market Commentary

THE WEEK IN REVIEW: July 16 – July 22, 2023

Rally continues as the market anticipates the July Fed meeting

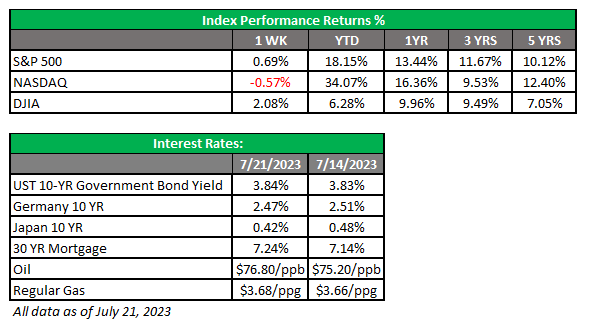

Last week was a strong one for the market, even though corporate earnings were mixed. (More on this in the next section.) Overall, the Dow Jones Industrial Average (DJIA) closed at new yearly highs on Friday at 35,227.69. The S&P 500 followed suit most of the week, up 18% for the year before sliding off to end the week.

Anticipation about the Federal Reserve’s meeting drove markets, although it’s more about what they will say after the meeting. A 25-basis-point increase is almost 100% baked into the markets, but the real news will be what tone Fed Chairman Jerome Powell takes at his press conference immediately after the announcement on Wednesday. It will be interesting because the market views the decline in the Consumer Price Index (CPI) and weaker consumer spending as reasons for the Fed to stop increases and begin teeing up cuts as we head into the end of the year.

The other side of the coin still sees a strong jobs market and an economy that’s still hanging in there. The initial reading of second-quarter gross domestic product (GDP) will be out the day after the Fed concludes its meeting. Right now, advance estimates are calling for GDP to have grown at 2.4%, topping the first quarter. If that holds true, it will indicate the economy is accelerating — not slowing as we’ve been told.

Core inflation, the measure the Fed focuses on when considering its progress in lowering inflation, is at 4.8%, well above the Fed’s 2% target. It appears the market is racing ahead with disproportionate expectations once more. If the Fed believes the economy and jobs are both still robust enough to handle higher rates, it may try to push core inflation to 2%. It doesn’t seem like the market is anticipating that possibility, and if Powell comes off as hawkish, we could be in for a rocky end to the summer.

A mixed bag of earnings

Earnings season is in full swing. Despite some outsized announcements (Delta and Bank of America) and a few disappointments (Goldman Sachs), markets seem to be rallying. Every earnings season has its surprises, both good and bad, but expectations for the second quarter were particularly glum. Inflation, interest rates, slower consumer spending, a decelerating economy, etc., were all reasons cited for potentially lower earnings. But like everything else, if you could predict everything with certainty, why would we need estimates?

The yield curve inversions that have stuck around for over a year now have been predicting a recession that has yet to materialize. Interest rate hikes were supposed to devastate the jobs market and instead created lots of instability and uncertainty for regional banks. Likewise, earnings were supposed to be horrific, and they just aren’t — and we think it’s good that better-than-expected earnings are defying expectations.

Coming This Week

- This week will be a big one, with the Fed meeting on Tuesday and Wednesday. Given the slew of reasons not to continue raising rates further, if Chairman Powell comes off as hawkish, it could lead to turbulence and volatility. The market would again get nervous and start hemming and hawing about the direction of rates, which right now it believes will be trending downward by year-end.

- The other big data coming out this week will be the first reading of second-quarter GDP. The Federal Reserve Bank of Atlanta is projecting growth of 2.4%.

- The earnings beat will continue this week. We’ve had a mixed bag so far, but by and large earnings have been better than expected, so the dreaded collapse in earnings from higher rates has yet to materialize. Many commentators believed this earnings season would be the low point, but so far earnings haven’t been too bad.

- Consumer confidence and the Case-Shiller home price index will be released on Thursday. Consumers are hanging in there and home prices are rebounding, as both seem to have gotten used to higher rates.

- Mortgage applications and new home sales numbers will be out on Wednesday. Finally, personal spending and consumer sentiment will close out a busy week for data.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

7/23-2982871-3