AE Wealth Management: Weekly Market Insights | April 23-29

Weekly Market Commentary

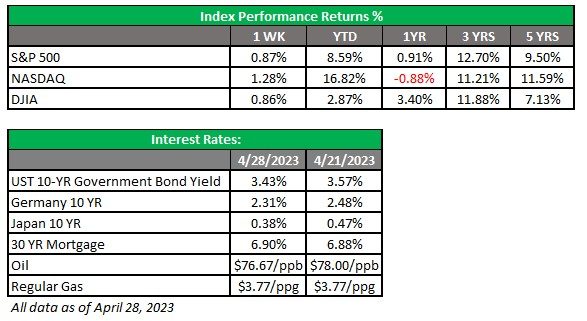

THE WEEK IN REVIEW: April 23-29

GDP reading signals the economy is slowing

The first reading of first-quarter gross domestic product (GDP) was released last week, coming in lower than the forecasted 2.0% at 1.1%. The mild winter in most of the U.S. led to a temporary surge in consumer spending in January, and new auto sales were also robust in the first quarter. There was also a record-high Social Security cost-of-living adjustment and seasonal adjustment issues due to the timing of COVID stimulus payments in 2020-21.

All of this was overwhelmed by slower spending and declining confidence from the consumer, and it appears the Federal Reserve’s rate increases are finally making an impact. Inflation was hammering the consumer, and the Fed aggressively moved to address it by raising rates. Savings levels, which had ballooned during the pandemic, were depleted by inflation and higher prices, and consumers had to resort to credit to keep up with their spending habits. Higher interest rates have made borrowing much more expensive, and all those people who ran up their credit card balances to record highs are paying more to service that debt.

Is it any wonder, then, that it appears consumers are choosing to spend less to try to get those balances under control? Or that their lack of ability to continue to consume is causing their confidence to decline? Their optimism seems to be fading. We’ve said before that once the consumer cracked, the economy would be in trouble — and it appears we are nearing that stage.

The same can be said of the stock market and company earnings. Earnings have been mixed, but higher rates clearly impacted the bottom lines of many companies. (See more on earnings below.) Layoffs are becoming more frequent, and higher interest rates have created havoc in the banking sector. All this could be creating a brew of uncertainty and clearly has an impact on the psyche of the consumer, investor and average citizen who feels the economy is on the wrong track. As a result, it’s not surprising that the stock markets seem nervous and rangebound.

The 1.1% GDP growth would likely have been even lower if the winter had been harsher and a lot of the one-offs mentioned above hadn’t materialized. But even with those one-time bumps, 1.1% growth is pretty anemic, especially compared to +3.2% and +2.6% in the third and fourth quarters of 2022, respectively. We likely won’t see an improvement next quarter, and if we see negative growth for Q2, we are halfway to the official definition of recession.

What is needed to get back on track? I believe the Fed needs to stop raising rates. It’s not a magic solution; if the Fed stops raising rates, things won’t automatically revert back to all good or normal. We need to get government spending in line, and the consumer needs to get healthy again before that can happen. But if the Fed stops raising rates, it will go a long way to not making things worse. Then the economy can start to recover, and we can begin to usher in higher growth, more optimism and better times ahead.

Good earnings overshadowed by bank woes and debt ceiling drama

A few major companies (such as Meta and Microsoft) reported decent earnings early last week, causing the market to rally. But bad news from First Republic Bank created a sour mood, and markets sold off on fears of potentially more bank failures.

The debt ceiling debate is also hanging around like a bad kitchen smell. House Republicans passed an increase of the debt ceiling with proposed cuts, while the White House vowed not to negotiate unless there were no contingencies associated with a rate increase. The stalemate isn’t doing anything to help markets.

Additionally, the upcoming Fed meeting had investors worried about how much the Fed would raise rates this time. In classic “bad news is good news” fashion, the anemic first-quarter GDP report sparked a rally in the market because it locked in a quarter-point fed funds rate hike at the most. Looking forward, it appears we will get one more increase, with most market watchers anticipating cuts in the fed funds rate in early 2024.

What the weak GDP report didn’t do was offset the banking industry woes and debt ceiling drama. However, it stopped markets’ downward slide early in the week, and guess what? We’re right back to the same 4,000-4,200 range on the S&P 500 that we’ve been sitting at since February. Perhaps this week we’ll get some direction from the Fed and the jobs numbers will justify a pause. But the debt ceiling and bank jitters will probably still be lingering for a while.

Coming this week

- It’s Fed meeting week! The meeting starts Tuesday and concludes on Wednesday. Expectations are for an additional quarter-point increase in the fed funds rate, taking it from 4.75%-5% to 5.00%-5.25%. While inflation appears to be in decline, the Fed still needs to see a crack in job growth and a slowing economy to put a pause on rate hikes.

- The Job Openings and Labor Turnover Survey (JOLTS) report will be released on Tuesday, showing the job openings from March. Factory orders will also come out on Tuesday.

- On Wednesday, we’ll get the ADP employment report and mortgage applications.

- We’ll see data on job cuts on Thursday, plus the Bureau of Labor Statistics’ Employment Situation report on Friday.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

5/23-2876775-1