AE Wealth Management: Weekly Market Insights | April 16-22

Weekly Market Commentary

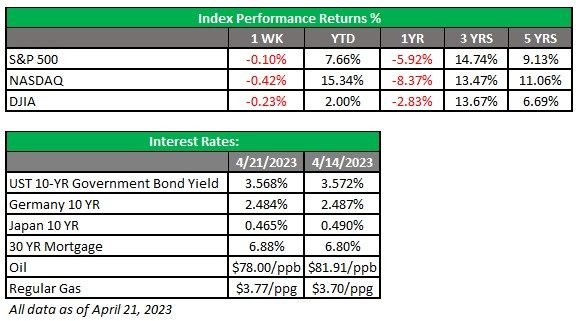

THE WEEK IN REVIEW: April 16-22

Markets are muted as we await the Fed

It almost feels as if it’s the middle of summer for markets. After the major dustup from the Silicon Valley Bank and Signature Bank situations and the government’s subsequent actions, markets seem to have calmed down and are downright mild compared to how they behaved in the first quarter of 2023. Even so, we managed to close out a pretty strong quarter, with the S&P 500 rising 7.5% despite all the drama. The volatility index (VIX) is down into the midteens, and daily moves are muted. Earnings are disappointing but haven’t cratered the markets.

Despite the calmness, two factors seem to be holding the markets back. Let’s start with recessionary fears: It might come as no surprise that most economic forecasters have predicted a recession could start soon. But the question now is, how do you define “soon?” Last year, people were saying to expect a recession in late 2022 or early 2023; now most of the same people say a recession will likely begin in late 2023 or early 2024.

No matter whom you follow or believe, the conventional expectation is for a mild recession six to nine months from now. When data comes out to support that narrative, the market seems to have a decent day; when the data is gloomier, the markets sink. However, we remain in the 4,000-4,200 range on the S&P 500 (the highs for the year so far) without seeing major movements out of the range.

That brings us to the other factor holding markets back. It previously appeared the Federal Reserve would stop raising rates after its last meeting, especially after the banking sector experienced panic. Now it seems a close shave wasn’t enough for the Fed, and analysts are predicting a nearly 90% chance of another 25-basis-points hike at its May meeting. Another rate increase may not put further pressure on the banking sector, but who knows where the next problem will materialize due to higher interest rates.

The sooner the Fed stops, the better. Inflation data appears to be complying and provides a compelling reason for a pause. The same experts who have predicted coming recessions are also predicting the Fed will pause after its next meeting and begin cutting rates by this time next year. Markets are also expecting this scenario, and as long as nothing comes along to upset that view, it appears the market is willing to sit and wait for what develops.

Oh, what a feeling … when we’re dancing on the (debt) ceiling

Maybe Lionel Ritchie was on to something. It would seem this story shouldn’t be a story, but given today’s political climate, here we are. On one side, you have a party that wants to see budget cuts and spending reductions before signing off on a higher debt ceiling. The other side says we need to pay for our obligations and lift the debt ceiling — no strings attached.

Putting aside all the political huffing and puffing, both sides have a point. It may be time to raise the debt ceiling, but plenty of federal government programs need to be streamlined or eliminated. Incurring more debt without reviewing what we are borrowing for will just result in an ever-widening circle of waste. We will have to borrow more and more to continue to fund inefficient or wasteful programs, something neither party really wants.

However, the government will most likely continue to spend if they are allowed. It’s believed that the longer we drag the debt ceiling debate out, the greater the potential for unforeseen events to be introduced into an already tense situation. We cannot afford to default, as doing so would increase the chance of flattening the economy. And the public would certainly blame those in charge, so both sides would suffer. We could potentially avoid all that by simply coming together and hammering out a deal. So far, that doesn’t seem possible, and it will continue to wear on markets as we come closer and closer to the cliff. As we do, it won’t take a huge mistake to veer off into disaster.

Coming this week

- Earnings will dominate the market this week as we await the Fed meeting on May 3-4.

- This week’s data will include consumer confidence and new home sales (Tuesday), mortgage applications and retail/wholesale inventories (Wednesday), pending home sales (Thursday) and consumer spending and consumer sentiment (Friday).

- The first reading of first-quarter gross domestic product (GDP) is scheduled to be released on Thursday. The expectation is for growth of 1.8%, largely due to a temporary surge in consumer spending in January. Real GDP growth remained positive in the first quarter but likely slowed from the final fourth-quarter reading of 2.6%.

AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM.

Information regarding the RIA offering the investment advisory services can be found on https://brokercheck.finra.org/.

Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values.

The information and opinions contained herein, provided by third parties, have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management.

This information is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security or insurance product.

4/23-2825836-4