AE Wealth Management: Minimum Retirement Payouts | Blog

NEW RMD RULES FOR 2022

The Wealth Report by AE Wealth Management

Download PDF Version Here

New IRS tables are designed to decrease the amount of required minimum distributions (RMDs) going forward.

Overview

Retirement income savings plans, such as an employer 401(k), 403(b) plan and the traditional IRA, permit investors to contribute earned income on a tax-deferred basis. Investment growth via capital gains also are tax-deferred until withdrawals are made, which are then subject to income taxes.

These programs are designed to encourage people to save money for retirement by giving them an incentive to defer taxes on their current income. The more they contribute to these retirement plans, the less income they have to report on their annual tax return.

However, the Internal Revenue Service (IRS) plans on getting those tax revenues eventually, and typically on a larger balance that has been growing unencumbered for many years. The IRS even imposes a required minimum distribution (RMD) each year starting at a certain age, to ensure the deferred income and capital gains begin generating tax revenues once the account owner is in retirement. Beginning in 2020, the age to begin taking RMDs rose from 70 ½ to 72.

Once an account owner turns age 72, she has until April 1 of the following year to take her first RMD. In subsequent years, RMDs must be withdrawn before Dec. 31.1 Also note that the account owner is always free to withdraw more than the minimum required amount.

“In order to reflect a longer life expectancy, the tables provide a larger divisor, which produces a smaller RMD; this allows retirees to retain more retirement savings in their accounts for their later years.”2

New Changes

Not only did Congress raise the age at which RMDs must begin, but the IRS recently made adjustments to the Uniform Life Table. This table is established by actuaries who make an assumption about how long the average person will live based on the age he has attained. These assumptions are updated periodically to reflect gradual increases in overall life expectancies over time — facilitated by advances in medicine and healthier living trends.

Over the past two years, there have been so many deaths attributed to COVID-19 that life expectancy in the U.S. has actually dropped. According to federal mortality data released in December of 2021, the average life expectancy declined by 1.8 years in 2020, from 78.8 years in 2019 to 77 years in 2020. Notably, in 2020 COVID-19 was the third-most common cause of death in the U.S., accounting for one out of every 10 deaths.3

Regardless, changes to government policies take time, meaning that the updates to the Uniform Life Table were established pre-pandemic and the timeline for adopting the new table was already scheduled to take effect in 2022.

Fortunately, the updated table represents good news for retirees who do not need a large portion of their retirement account funds to maintain current living expenses. The lower RMD amounts mean that more of their assets have the opportunity to continue growing, with a lower annual tax bill. Retirees who do need substantial withdrawals from retirement plans are largely unaffected since they would likely be taking larger distributions from these accounts anyway.

How To Calculate Your RMD

Be aware that the amount of your RMD will change every year. The annual RMD calculation isn’t difficult, but you do need the most updated Uniform Life Table to determine the correct amount. One component of the calculation is the retirement plan’s previous year-end account balance, which changes every year based on performance and previous withdrawals.

A second component is your life expectancy, which also changes every year as you age. The RMD for each retirement account is determined by dividing the year-end value by the estimated remaining years of your lifetime — based on your age on Dec. 31.

Account balance ÷ Life expectancy factor = RMD

Because the new life expectancy chart is based on a longer average life expectancy than the previous table, the divisors have increased, which means the amount required to be withdrawn will be lower than it would have been based on the previous table.

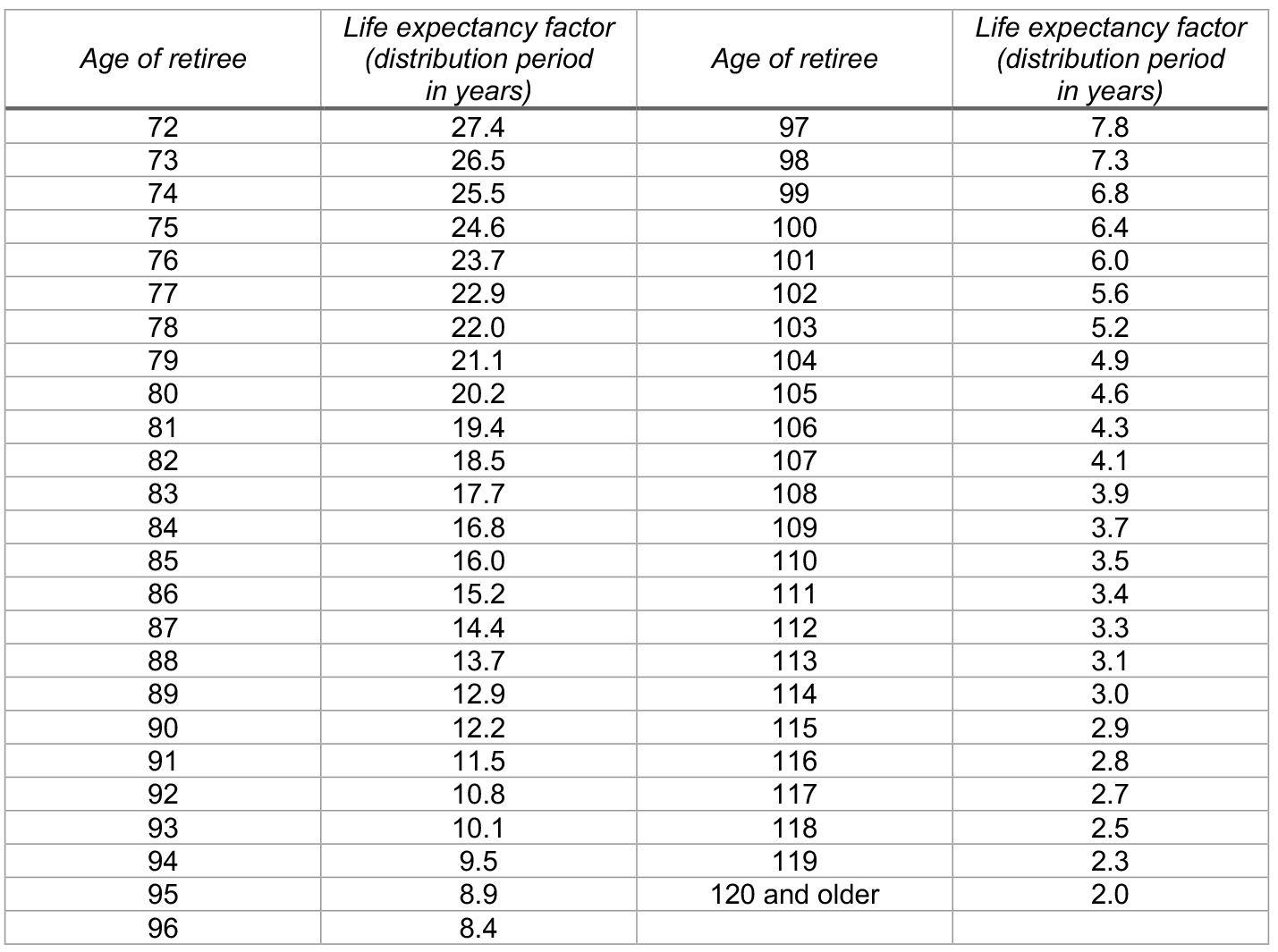

2022 New RMD Table4

Let’s take two examples to illustrate how to calculate the RMD. In the first scenario, Rhonda turns 72 in 2022, so she must take her first RMD by April 1, 2023. If her account balance at year-end 2021 was $1,000,000, her 2022 RMD will be $36,496 ($1,000,000 divided by 27.4).

TIP: In the year you turn age 72, you may not want to wait until April 1 of the following year to take your first RMD. That’s because you’re required to take your second RMD by Dec. 31 of that same year — two RMDs in one year! That could result in a big tax bill.

Now let’s take the example of Roger, age 90. Even though his 2021 RMD was based on the old table, he will need to use the new table to determine his 2022 amount. Let’s say his 2021 year-end account value was also $1,000,000; that will make his RMD this year $81,967 ($1,000,000 divided by 12.2). Even though their account values are the same, Roger and Rhonda’s RMDs are vastly differently because Rhonda is expected to live another 27 years, whereas Roger’s life expectancy is only 11 more years.

The IRS would like to tax that money before the account owner passes away. One thing to bear in mind, however, is that if the account passes to a non-spouse beneficiary upon the owner’s death, the tax bill will likely be even higher. That’s because a younger beneficiary may be in a higher tax bracket or keep the money invested up to 10 more years, so the tax rate would be higher than that of the retired account owner.

Because your life expectancy decreases every year, the percentage of your assets (RMD) that must be withdrawn each year increases accordingly.5

Much Younger Spouse

In this one instance of a much younger spouse, the RMD calculation requires a different table to determine the life expectancy factor. When the only beneficiary of a retirement account(s) is the owner’s spouse, and that person is 10 or more years younger than the account owner, then a different table (the Joint Life and Last Survivor Expectancy Table) must be used.

For example, let’s assume that Rick is age 74 and his wife (the sole beneficiary) is 45. You would cross-reference the ages of both spouses on the Joint Life and Last Survivor Expectancy Table. According to the table, the divisor for these two ages is 41.3. If Rick’s account balance at the end of the year was $1,000,000, his RMD would be $24,213.6

Beneficiary RMDs

RMD rules for beneficiaries differ based on the status of the beneficiary, but the one hard-and-fast rule is this: Before the account is transitioned in any way, if an RMD is scheduled for the year of the original owner’s death, the beneficiary must withdraw the RMD amount (if not already distributed) for that year.

Once that is done, the rules vary. The following is an overview of different scenarios, but beneficiaries should investigate the specifics before making any financial moves.7

Spouse

A sole spousal beneficiary has the most options. If she chooses to cash out the account, she will have to pay income taxes on the proceeds. Alternatively, she can roll the money into her own IRA and make RMDs based on her own life expectancy. Another option is to open an inherited IRA, transfer the balance and remain the beneficiary. Under this scenario, RMDs will be based on her life expectancy but would not have to start until the deceased spouse would have reached age 72, assuming he hadn’t already.

Minor Child

If a child under age 18 (in most states) is the beneficiary, he would have to take RMDs based on his own life expectancy until he turns 18 years old. At that point, he has 10 more years during which time he must withdraw all of the remaining balance.

Disabled Beneficiary

If the beneficiary is chronically ill, disabled or less than 10 years younger than the deceased original owner, she can take distributions based on her own life expectancy and is not subject to the 10-year rule.

All Other Non-Spouse Beneficiaries

All the money must be withdrawn, and taxes paid, within 10 years. They can cash out right away or transfer the assets to an inherited IRA. Taxes are not due until the money is distributed, and they can make withdrawals at any time as long as the account is depleted within 10 years of the original owner’s death. The 10% early withdrawal penalty does not apply even if they are younger than age 59 ½. Bear in mind that while the investment may continue growing throughout the 10 years, so will the ultimate tax bill.

If they do not withdraw the full RMD amount by the deadline, any money not withdrawn is taxed at 50%. This goes for both original account owners and beneficiaries.

RMD Tips

The following are some tips to bear in mind. They may or may not pertain to your situation, but they’re good to know in case you need to investigate your circumstances further.8

- You can take your annual RMD in a lump sum, as needed, or in monthly or quarterly payments. If you delay taking the RMD until year-end, your money will have more time to grow tax-deferred.

- If you work and contribute to a retirement plan sponsored by your employer (and you don’t own more than 5% of the company), you are not required to take RMDs from that particular account until you stop working for that employer.

- However, you must take RMDs from any other 401(k), 403(b) or traditional IRA accounts you own.

- If you have multiple IRAs, including SEP and SIMPLE IRAs, you may take their combined RMD amount from any one of those accounts (or any combination you choose).

- If you have multiple 403(b) accounts, the same applies.9

- However, if you have multiple 401(k) accounts, you must withdraw RMDs from each account subject to the rules.

- Married couples cannot aggregate RMD amounts and withdraw them from one or the other’s account.

- Inherited IRA RMD amounts may not be aggregated either, unless you have multiple IRAs inherited from the same decedent.

- RMDs do not apply to Roth IRAs, as the original contributions were already taxed.

Final Thoughts

RMD rules for retirement accounts can be complex. If you don’t fall under one of the simpler scenarios — especially as a beneficiary — it’s a good idea to get professional advice. You can tap the expertise of a representative who works for the account custodian, but it also can be helpful to consult with a trusted financial advisor and/or a tax professional, depending on your situation.

1 Bob Haegele and Kay Bell. Bankrate. Jan. 18, 2022. “IRA required minimum distributions table 2022.” https://www.bankrate.com/retirement/ira-rmd-table/. Accessed Feb. 15, 2022.

2 David M. Barral. The CPA Journal. December 2021. “Transitioning to the Updated Required Minimum Distribution Tables in 2022.” https://www.cpajournal.com/2021/12/22/transitioning-to-the-updated-required-minimum-distribution-tables-in-2022/. Accessed Feb. 15, 2022.

3 Laura Santhanam. PBS NewsHour. Dec. 22, 2021. “COVID helped cause the biggest drop in U.S. life expectancy since WWII.” https://www.pbs.org/newshour/health/covid-helped-cause-the-biggest-drop-in-u-s-life-expectancy-since-wwii. Accessed Feb. 15, 2022.

4 Bob Haegele and Kay Bell. Bankrate. Jan. 18, 2022. “IRA required minimum distributions table 2022.” https://www.bankrate.com/retirement/ira-rmd-table/. Accessed Feb. 15, 2022.

5 Ibid.

6 Fidelity. 2022. “IRS Joint Life Expectancy Table.” https://www.fidelity.com/bin-public/060_www_fidelity_com/documents/Joint-Life-Expectancy-Table.pdf. Accessed Feb. 22, 2022.

7 Sarah O’Brien. CNBC. Sept. 8, 2021. “Here’s how to avoid costly mistakes if you inherit a 401(k) or IRA.” https://www.cnbc.com/2021/09/08/heres-how-to-avoid-costly-mistakes-if-you-inherit-a-401k-or-ira.html. Accessed Feb. 15, 2022.

8 Sarah O’Brien. CNBC. Dec. 21, 2021. “The best ways to avoid missteps with required withdrawals from retirement accounts.” https://www.cnbc.com/2021/12/21/required-minimum-distributions-from-retirement-accounts-can-be-tricky.html. Accessed Feb. 15, 2022.

9 Denise Appleby. Investopedia. June 29, 2021. “Required Minimum Distributions: Avoid These 4 Mistakes.” https://www.investopedia.com/articles/retirement/04/120604.asp. Accessed Feb. 15, 2022.

This content is provided for informational purposes. It is not intended to be used as the sole basis for financial decisions, nor should it be construed as advice designed to meet the particular needs of an individual’s situation. None of the information contained herein shall constitute an offer to sell or solicit any offer to buy a security. Individuals are encouraged to consult with a qualified professional before making any decisions about their personal situation. The information and opinions contained herein provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by AE Wealth Management. Neither AEWM nor the firm providing you with this report are affiliated with or endorsed by the U.S. government or any governmental agency. Investing involves risk, including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. AE Wealth Management, LLC (“AEWM”) is an SEC Registered Investment Adviser (RIA) located in Topeka, Kansas. Registration does not denote any level of skill or qualification. The advisory firm providing you this report is an independent financial services firm and is not an affiliate company of AE Wealth Management, LLC. AEWM works with a variety of independent advisors. Some of the advisors are Investment Adviser Representatives (IAR) who provide investment advisory services through AEWM. Some of the advisors are Registered Investment Advisers providing investment advisory services that incorporate some of the products available through AEWM. Information regarding the RIA offering the investment advisory services can be found at https://brokercheck.finra.org/.

2/22-2045119